EUR/USD seems to have found a temporary calm within the 1.0960 to 1.1070 levels, but this may change soon. What’s next in these disorderly times? The team at Credit Suisse weighs in:

Here is their view, courtesy of eFXnews:

…Many market participants are excited about the 10 March ECB meeting. They hope that a central bank that both understands the need to not appear impotent but also the risk of unintended consequences from misjudged policy will pull the perfect rabbit out of the hat.

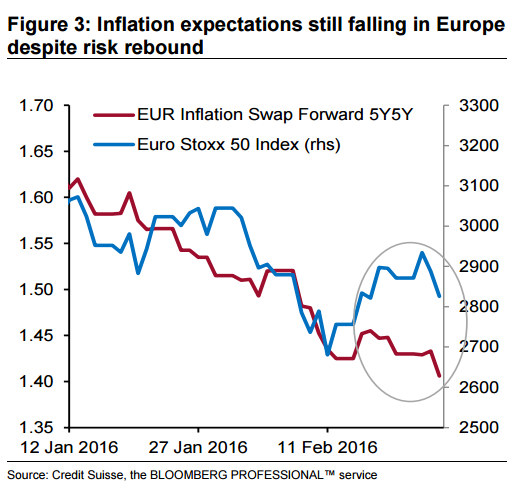

Our economists believe the ECB will cut the depo rate by a further 10bp, extend and expand QE, and potentially look to create and buy credit ETFs to allow for more effective policy transmission. These hopes really started to blossom around 11 February when risk markets bottomed.

The FX impact of this is clear too: since 11 February EUR has weakened materially against both USD and JPY. While some of that is a function of Brexit-fear spillover, most of it we think is ECB-related.

What is curious in our view is how confident the market seems to be that whatever measure the ECB decides on will lead to a lower EUR. After all, this year’s “aggressive” policy shifts in negative rates space from the BoJ and Riksbank led only to momentary FX weakness followed by material strength. The market seems willing to ascribe a much higher policy impact rating to the ECB.

For this reason we have decided to stay stubborn and hold onto our EUR/USD 1.17 3m forecast. We fully acknowledge that this would not be what policymakers want to see and would not help lift ever-falling euro area inflation expectations. But we suspect the proof of the pudding is in the eating when it comes to judging ECB success on 10 March.

Based on the high levels of FX realized volatility, our memory of last year’s 5% daily EUR/USD jumps on positioning squeezes and strong bearish EUR sentiment, anything that misses expectations or is reassessed negatively could easily trigger a large EUR rally. We would, of course, see this as a selling opportunity longer term (current 1y EUR/USD forecast: 1.10, 1y EUR/JPY forecast: 115), especially given the euro area’s profusion of both structural and cyclical weaknesses. But a positioning-related pop cannot be excluded. And certainly that is the pattern set by JPY and SEK this year after central bank easing. Still, a look at the EUR/USD risk reversal skew suggests that the market is at least conscious of this risk.

Related Posts

S&P 500 Dividend Yield: Past, Present, Future

S&P 500 Dividend Yield: Past, Present, Future Ghana’s vice president declares Africa should embrace digital currencies

Ghana’s vice president declares Africa should embrace digital currencies GBP/USD Has Brexit Barriers To Any Trump-Inspired Ascent

GBP/USD Has Brexit Barriers To Any Trump-Inspired Ascent E

The Economy: Mostly Good

E

The Economy: Mostly Good Apple Inc. (APPL) DCF Valuation: Is The Stock Undervalued?

Apple Inc. (APPL) DCF Valuation: Is The Stock Undervalued? WTI Crude Tumbles To $43 Handle After Large Cushing Build

WTI Crude Tumbles To $43 Handle After Large Cushing Build

Leave A Comment