Talking Points:

– EUR/USD Struggles Ahead of ECB Rhetoric- S&P Calls for Larger & Longer QE Program.

– USD/JPY Range Vulnerable to Slowing China, Waning Market Sentiment.

– USDOLLAR Continues to Coil as ADP Employment Boosts NFP Expectations- Fed on Wires.

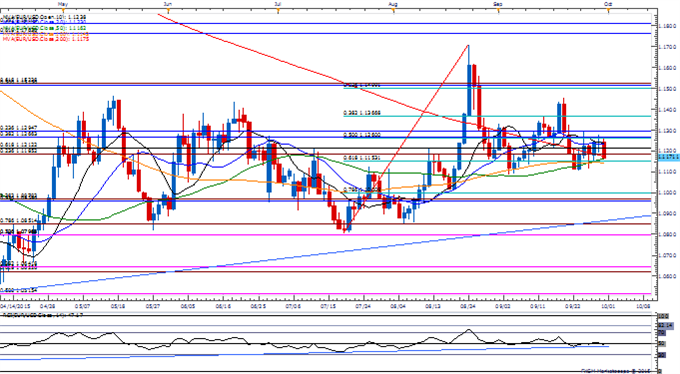

EUR/USD

Chart – Created Using FXCM Marketscope 2.0

EUR/USD struggles to hold its ground ahead of key speeches by the European Central Bank (ECB) officials as Standard & Poor’s (S&P) anticipates the Governing Council to extend its quantitative easing (QE) program until mid-2018, with the non-standard measure increasing the central bank’s balance sheet byEUR 2.4T.

Despite the dovish tone held by the ECB, may see risk trends continue to drive EUR/USD in October as market participants treat the Euro as a ‘funding-currency;’ may need imminent signs for additional ECB support for the long-term trends to come back into play as the central bank largely endorses a wait-and-see approach.

DailyFX Speculative Sentiment Index (SSI)shows retail crowd remains net-short EUR/USD since March 9, but the ratio remains off of recent extremes going into October as it sits at -1.29, with 44% of traders long.

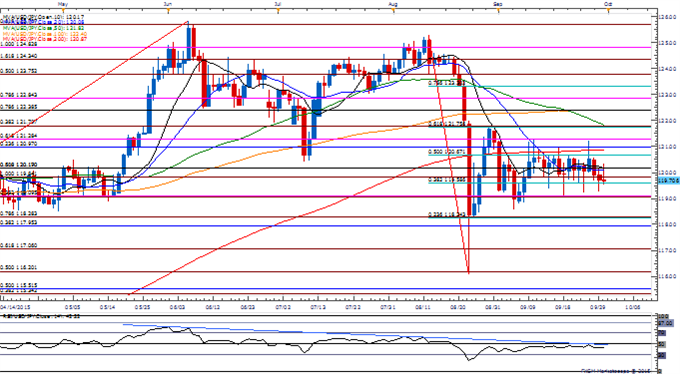

USD/JPY

With USD/JPY finally posting a closing price below near-term support around 11.90-90 (100% expansion), the pair remains at risk for a further decline in the month ahead especially as the Relative Strength Index (RSI) retains the bearish formation carried over from back in May.

Even though the Bank of Japan (BoJ) is scheduled to release the Tankan survey, the key prints coming out of China may play a greater role in driving USD/JPY volatility over the next 24-hours of trade as fears surrounding the global economy drags on risk appetite.

Despite the diverging paths for monetary policy, the BoJ’s wait-and-see approach may open the door for a more meaningful downside correction in the exchange rate amid speculation for additional monetary support at the October 30 interest rate decision.

EU officials sign Markets in Crypto-Assets framework into law

EU officials sign Markets in Crypto-Assets framework into law Stocks For You To Swing-Trade: BABA, TRCO, CVS

Stocks For You To Swing-Trade: BABA, TRCO, CVS This Indicator Shows How Long The Trump Effect On Markets Continues

This Indicator Shows How Long The Trump Effect On Markets Continues There’s Only 1-2 Years Left In This Bull Market. You Should Be Long Stocks

There’s Only 1-2 Years Left In This Bull Market. You Should Be Long Stocks Messi can rest: Argentina’s Copa America strategy

Messi can rest: Argentina’s Copa America strategy What Does Upcoming 100% Likelihood Of A Fed Rate Hike Mean For Investors?

What Does Upcoming 100% Likelihood Of A Fed Rate Hike Mean For Investors?

Leave A Comment