Fundamental Forecast for the Euro: Bullish

The European taper tantrum has continued into another week, and Euro interest rate forwards are now pricing in two ten-basis point hikes going out to the end of next year; specifically around ECB meetings in July and December of 2018. This is a stark contrast to just a month ago, when there were no hikes expected over this same period. As we discussed last week, this theme of higher rate expectations kicked off around a speech from ECB President Mario Draghi, when the head of the bank said that ‘deflationary forces have been replaced with reflationary forces’, and this came after the comment: ‘The threat of deflation is gone and reflationary forces are at play.’ So, Mr. Draghi’s reiteration around this topic has served to drive rate expectations higher as the continued strength in European inflation is forcing a hawkish turn within the ECB.

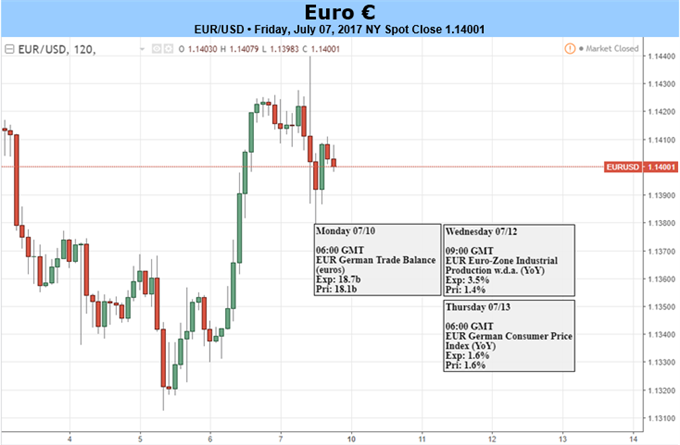

Data for this past week out of Europe was relatively light, with only a handful of medium-importance announcements. On Monday, Euro-Zone Unemployment printed in-line at 9.3%, and then EZ retail sales came-in above expectations on Wednesday, printing at 2.6% versus the expectation of 2.3. A mixed bag of data came out of Germany on Thursday and Friday, as factory orders disappointed while industrial production numbers printed with a strong beat. The fundamental driver that appeared to garner the most attention this week and which led to a strong showing in the Euro on Thursday was the ECB minutes from the June rate decision. This meeting saw the bank hold rates flat while Mr. Draghi attempted to talk down the Euro, after which buyers showed-up to support prices. But in the meeting minutes, it became clear that there is a growing chorus within the bank looking for tighter policy options as inflation continues to remain strong.

Related Posts

The Big Four Economic Indicators: January Real Retail Sales

The Big Four Economic Indicators: January Real Retail Sales Owning REITs With Consistently Growing Dividends Is A Proven Strategy

Owning REITs With Consistently Growing Dividends Is A Proven Strategy How Much Does A Tax Cut Cost?

How Much Does A Tax Cut Cost? In Stunning Crash, Bitcoin Wipes Out December Gains Then Rebounds $2,000 In 7 Minutes

In Stunning Crash, Bitcoin Wipes Out December Gains Then Rebounds $2,000 In 7 Minutes Aussie Jumps After RBA Leaves Interest Rates Unchanged

Aussie Jumps After RBA Leaves Interest Rates Unchanged E

USD/JPY Elliott Wave Forecast: Wave IV Pull Back

E

USD/JPY Elliott Wave Forecast: Wave IV Pull Back

Leave A Comment