Politics drove currency market trends in 2017…

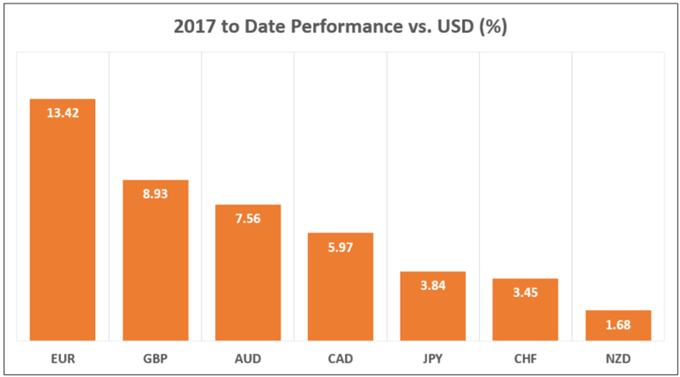

The US Dollar reversed the so-called “Trump trade” narrative prevailing in the months following the 2016 presidential election, falling against all of its major counterparts. The greenback had been buoyed by hopes that the eccentric billionaire’s unlikely triumph would bring inflationary fiscal stimulus and push the Fed into a steeper rate hike cycle. It fell as he struggled to turn campaign promises into legislation.

The Euro led the way higher as a series of worrying elections passed without handing the reins of power to destabilizing eurosceptics. The status quo held out in the Netherlands, France elected an energetic centrist in Emmanuel Macron, Italy managed the abrupt transition from the Renzi to the Gentolini government, and Spain muddled through a separatist flare-up in Catalonia.

The British Pound followed closely behind its Continental counterpart. The markets improbably cheered the outcome of a UK snap electionmeant to cement the authority of Prime Minister Theresa May over warring government factions. That plan went terribly awry, with the Conservatives losing parliamentary majority.Investors seemingly concluded this humbling experience might mean a “softer” Brexit however.

Source: Bloomberg

The greenback’s woes were understandably supportive for the currencies it threatens to unseat at the high end of the G10 FX yield spectrum. The Australian Dollar managed to capitalize but its New Zealand cousin lagged behind after an initially inconclusive general election produced a radically minded government promoting sweeping economic policy changes, including a change of the RBNZ mandate.

…but textbook fundamentals may mark sharp reversals

The year ahead may look decidedly different as monetary policy reasserts its influence. The Euro is perhaps most vulnerable to reversal as the passing of political pitfalls puts the spotlight back on the ECB, where QE asset purchases have been extended at least through September 2018 (albeit at a slower pace of €30 billion per month, down from €60 billion previously). An actual rate hike seems nowhere in sight.

Related Posts

New Record High On Bitcoin! Where To Next?

New Record High On Bitcoin! Where To Next? GBP/USD Possibly Heading Toward 1.52

GBP/USD Possibly Heading Toward 1.52 Momentum And Large-Cap Growth Still Lead Equity Factor Returns

Momentum And Large-Cap Growth Still Lead Equity Factor Returns Price & Time: Gold – Can It Get Out Of Its Own Way?

Price & Time: Gold – Can It Get Out Of Its Own Way? EURUSD: Euro Licking Its Wounds After Yesterday’s Drop

EURUSD: Euro Licking Its Wounds After Yesterday’s Drop This Sector Is Poised To Surprise The Market (But We See It Coming)

This Sector Is Poised To Surprise The Market (But We See It Coming)

Leave A Comment