Earlier this month, Mario Draghi disappointed markets by failing to deliver an outsized depo rate cut and an expansion of monthly PSPP purchases.

It’s not that the ECB didn’t ease. They did. It’s just that they didn’t ease enough, because when every DM central banker has gone Keynesian crazy (or, “full Krugman” as it were), a 10 bps cut doesn’t “cut” it (so to speak), and a six month extension of QE had been priced in at least since September.

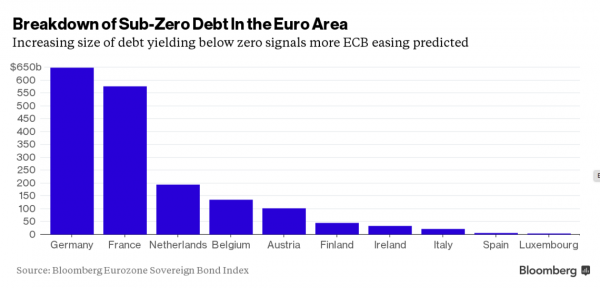

With EU inflation still stuck in Japan mode and with GDP bumping along at the “new normal” pace of what might as well be 0%, the market expects more from Draghi going forward. Need proof? Just look at yields. “As the European Central Bank wound down its asset purchases for the year,the amount of euro-region government bonds that yield less than zero was at about $1.68 trillion, indicating investors see the potential for further easing of monetary policy in 2016,” Bloomberg writes, adding that “a slump in oil prices is supporting economists’ view that the ECB is unlikely to veer from its accommodative policy stance as it struggles to achieve its inflation goal of just under 2 percent.”

“So many sub-zero-yielding securities indicate that there is a belief that there is no real inflationary pressures evident yet, and the ECB will remain ready to do more if required,” Cantor’s Owen Callan says.

Perhaps. But remember that at this point, each incremental purchase of EU govies (especially bunds) brings the ECB closer to the endgame wherein there are simply no more core EGBs to buy at which point it’s either purchase more from the periphery or move into riskier assets and with political turmoil playing out in Spain and Portugal, it’s not entirely clear what’s riskier: sub-sovereigns or PIIG debt. For those who need a reminder of just how scarce purchase-eligible core debt is becoming, here’s a helpful graphic from Citi:

Related Posts

Temporary Speed Bump Expected To Weigh On US Q3 GDP Report

Temporary Speed Bump Expected To Weigh On US Q3 GDP Report April 2016 Conference Board Employment Index Improves But Lower Employment Growth Expected

April 2016 Conference Board Employment Index Improves But Lower Employment Growth Expected Distribution Selling Returns

Distribution Selling Returns Takeda Pharma Promotes A Healthy Future

Takeda Pharma Promotes A Healthy Future What Made Gold Go Up

What Made Gold Go Up- WTI Crude Weekly Gain Slips As Supply Concern And OPEC Doubts Rise

Leave A Comment