For professional investors, August was the cruelest month.

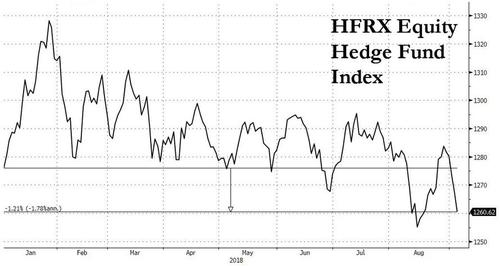

In the month when the S&P 500 cleared a new all time high, rising above 2,900 for the first time ever while setting a new record as for the longest “bull market”, hedge funds were dazed and confused by the market action, suffering another month of sharp underperformance, and sending their YTD return back into negative territory according to the HFRX equity hedge index.

But it wasn’t just hedge funds who suffered the painful short squeezes and sector rotation that prompted Nomura to observe a “multi-month performance disaster for US equity funds”: according to Bank of America, “plain vanilla” large cap mutual funds also struggled to match the rally and posted their weakest hit rate in more than two years, as just 22% of funds managed to beat their benchmark in August, while the average fund underperformed its respective benchmark by more than 70bp.

On a year to date basis, less than half, or 43% of large cap funds, have outperformed their benchmark – down from 50% last month – and well below the 55% at the same time last year. As a reminder, most benchmarks – and certainly the S&P – are indexes which most investors can allocate funds to with virtually no costs and management fees, which means that in 2018, more than half the US asset management industry has destroyed value for their investors.

However, that performance is stellar compared to the (under)performance of large cap core, or blended funds which seek to diversify into both value and growth stocks, which had an abysmal hit rate in August of just 13%: this was the worst showing in the the history of Bank of America’s data which goes back to 2009.

What prompted this abysmal monthly return? While various factors contributed to the poor performance, BofA strategist Savita Subramanian said that avoiding FAANG stocks was the biggest culprit.

Recall that in the first half, just four stocks, Amazon, Microsoft, Apple and Netflix, were responsible for 84% of the S&P upside in 2018. Furthermore, in the first six months of the year, the return of the top 10 S&P 500 stocks of 2018 – which are the who’s who of the tech world – saw their collective return amount to 122% of the S&P total return in the first half of the year. In other words, excluding just the top 10 stocks, the S&P’s return was negative in H1.

Leave A Comment