China’s ‘Super Friday’ data dump arrived and despite the 10% devaluation in the Renminbi basket over the past year, and an utterly incredible spike in borrowing (new loans spiked again in June!!), China economic data merely muddles through in its centrally-planned goal-seeked way. Earlier ‘researchers’ proclaimed Chinese GDP at around 6.5% but China GDP grew at 6.7% YoY (beating expectations of 6.6%). While Fixed Asset Investment disappointed (+9.0% vs +9.4% exp), Retail Sales (+10.6%) and Industrial Production (+6.2%) beat expectations.

The devaluation against the USD is starting to accelerate as the broad Renminbi basket has now dropped 10% in the last year (against all of China’s major trading partners)…

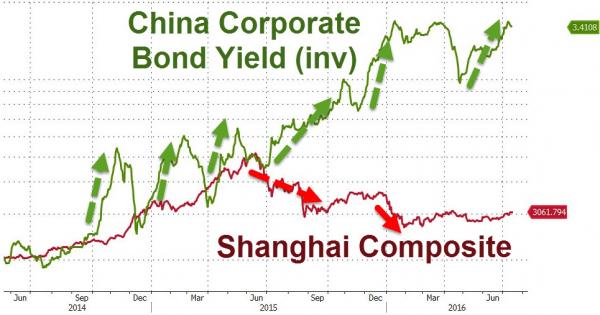

The search for yield has once again led to Chinese Corporates, which have rallied back to almost record bubble low yields (despite the utter carnage in Chinese balance sheets as leverage rises). Bonds have replaced stocks for now as the bubble-du-jour in China…

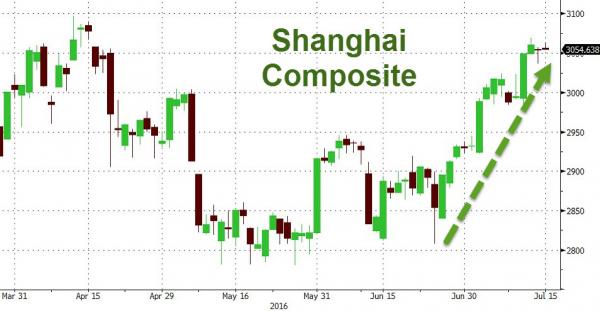

Not easily seen in this chart but SHCOMP has actually rallied bak to April levels in recent weeks amid the world’s flood of central bank largesse.

As Bloomberg notes, whenever China’s GDP beat or met market consensus, the country’s stock market fell. Here’s how the Shanghai Composite did following the last four GDP releases:

But it has not helped the macro-economic data much…

Related Posts

Economic Data And Forecasts For The Weeks Of April 17 And 24

Economic Data And Forecasts For The Weeks Of April 17 And 24- 5 Best Stocks Of The Top ETF Of August

Netflix Stock Buying The Dips At The Blue Box Area

Netflix Stock Buying The Dips At The Blue Box Area E

Microsoft Is Finally A Compelling Value Growth Idea

E

Microsoft Is Finally A Compelling Value Growth Idea Ripples of Bitcoin adoption at Biarritz’s Surfin Bitcoin Conference in France

Ripples of Bitcoin adoption at Biarritz’s Surfin Bitcoin Conference in France Bouncing Toward The Gap And MA

Bouncing Toward The Gap And MA

Leave A Comment