Forecast for USD Next Week: Neutral

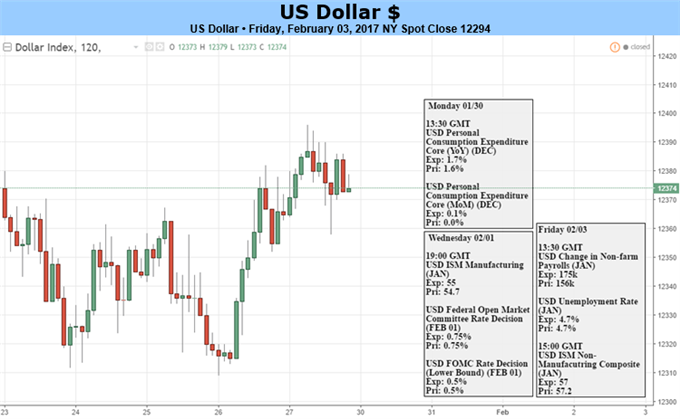

This week saw a heavy inclusion of U.S. drivers come-in to global capital markets, and this was somewhat to be expected for a week that had both the Federal Reserve and Non-Farm Payrolls on the calendar. But, what was perhaps most relevant to USD prices this week was something that few, if anyone, was expecting, and that’s the volatility around the executive order signed by President Trump last weekend around immigration. In what has widely become known as ‘the immigration ban,’ a lot of confusion populated headlines and global markets alike, with the net impact being USD-weakness as questions abound regarding continuation potential of ‘the Trump Trade’.

After gapping-lower to start the week, the Dollar’s bearish price action continued all the way into Wednesday, at which point a brief amount of support showed-up ahead of the Fed. But this meeting did little to re-fire hopes for any near-term rate hikes as the bank made only slight modifications from their previous statement that was issued in December. But what was perhaps most intriguing wasn’t what was in that statement: It’s what wasn’t there; and that’s acknowledgement of the continued improvement in U.S. data that’s shown-up on the back of hope around ‘Trumponomics’. Deductively, this gives the appearance that the Fed isn’t making any huge plans for fiscal stimulus taking over economic growth anytime soon, nor was there any enhanced-need to look at tighter policy options in the near-term. This led into Non-Farm Payrolls which, like Wednesday’s FOMC event, was rather muted. The headline print was a very positive +227k jobs added to American payrolls; but wage growth was lacking with a print of 2.5% (well-below the expectation for wage growth of 2.7%, annualized) while the unemployment rate increased to 4.8% (versus prior and expectation of 4.7%).

Related Posts

Reactors Restart Uranium Mines: Thomas Drolet

Reactors Restart Uranium Mines: Thomas Drolet Stocks For You To Swing-Trade: NVDA, CSCO, ADI

Stocks For You To Swing-Trade: NVDA, CSCO, ADI EC

When Bond Kings Short Emerging Market Equities

EC

When Bond Kings Short Emerging Market Equities The Next Experiment, Part 1: Japan Prepares To Buy Pretty Much Everything

The Next Experiment, Part 1: Japan Prepares To Buy Pretty Much Everything E

SPX, Gold, Oil And G6 Prices For The Week Of September 4th

E

SPX, Gold, Oil And G6 Prices For The Week Of September 4th Trading Support And Resistance – Sunday, September 2

Trading Support And Resistance – Sunday, September 2

Leave A Comment