Yesterday’s violent reversal which saw the Dow tumble nearly 1000 points intraday from session highs on the Bloomberg report that Trump was preparing to unleash tariffs on all Chinese imports if upcoming talks with China’s president do not yield results, continued in the overnight session with headline scanning algos launching a global buying frenzy on a late Monday headline that Trump expects a “great deal” with China during a Fox News interview, while completely ignoring the rest of what Trump said, namely that China has “drained” the U.S. which has “really helped rebuild China” adding that “we are going to win that one,” referring to China trade battle, but the piece de resistance was that Trump doesn’t think China is “ready” to make a deal. Trump also confirmed the Monday’s Bloomberg report, saying that he is ready to impose $250BN in additional tariffs if deal doesn’t go through and adding that $267BN in tariffs was “waiting to go if we can’t make a deal.”

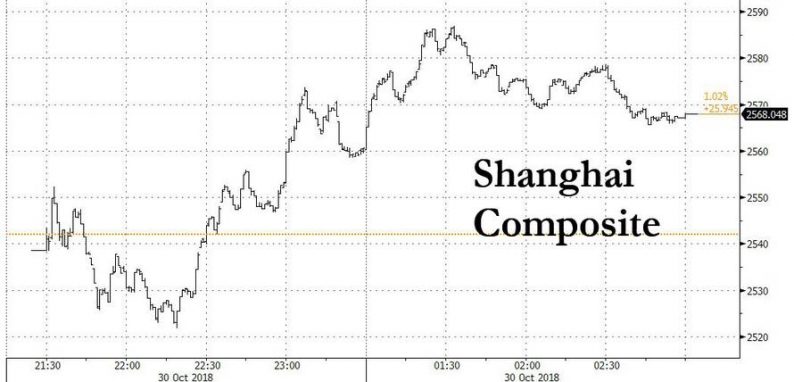

As it turned out, however, the “great deal” quote was enough to push Chinese stocks out of negative territory, and send Chinese stocks higher on the day, closing up 1%…

… while US futures followed suit and rose as much as 20 points from Monday’s close. However, it took some human intervention to temper the algo enthusiasm and read between the lines and trim the entire S&P futures rally…

…. while European stocks dropped as traders turned their focus to a slew of company results while realizing the what Trump said was not at all positive, and instead confirmed the next phase of a trade standoff between America and China.

While Europe’s Stoxx 600 index opened higher after better-than-expected results for major companies including BP and Volkswagen, earnings were mixed overall and promptly European bourses went into reverse after Germany’s DAX slumped to session lows dragging the broader Stoxx 600 into the red. Automakers declines were the culprit, which as Bloomberg noted is a sign that any inkling of good news, like VW’s earnings, beat for example, faces a high bar in convincing investors the worst is over for the sector.

Optimists meanwhile noted that U.S. futures were still up, if well off session highs, while there’s was little spillover into other asset classes. Core euro-area bonds were underperforming the periphery, while risk-sensitive currencies like AUD and NZD in G-10, or TRY and ZAR in the EM are keeping their gains for the moment even as the dollar surged to session highs.

Earlier, the MSCI Asia Pacific Index outside Japan swung in and out of negative territory in morning trade and last traded 0.3 percent higher on the day, halting a five-day losing streak. The yen slid and Aussie rose as Japanese and Australian shares rallied. China’s stocks climbed after authorities made a fresh attempt to stabilize its stock markets by saying they’d encourage long-term funds to invest, although activity was choppy with investors cautious about further escalations in the Sino-U.S. trade war.

The index has lost 12 percent this month and is on track for its biggest October decline since 2008, during the global financial crisis: “At this point, nobody can say the equity market is bottoming out. Global investor sentiment remains shaky,” said Yasuo Sakuma, chief investment officer at Libra Investments in Tokyo.

China’s Shanghai Composite and the blue-chip CSI 300 gained to 1.0% and 1.1%, respectively, winning back earlier losses in a volatile session after China’s securities regulator said it would encourage share buybacks and mergers and acquisitions by listed firms, and would enhance market liquidity, in the latest attempt to put a floor under the country’s skidding equity markets. Japan’s Nikkei average also erased early losses and climbed 1.5%.

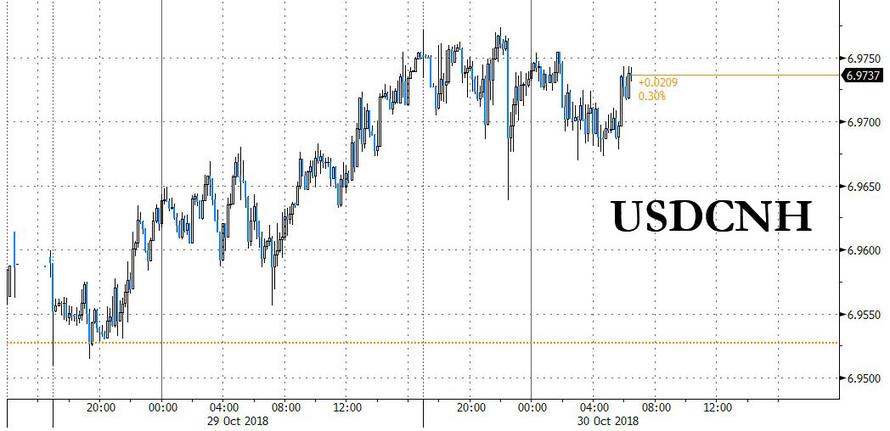

Adding to the jitters, China’s yuan continued to weaken, drawing closer to the closely watched support level of 7.00 vs the dollar. In onshore trade, the yuan slipped 0.15 percent to 6.9774 per dollar, a more than 10-year low, stirring speculation over whether the central bank will tolerate a slide beyond the key level of 7 per dollar.

According to Reuters, major state-owned Chinese banks were seen swapping yuan for dollars in forwards on Tuesday, but there was no immediate evidence of dollar selling in the spot market as the currency neared a key support level, three traders said.

As a result of the rising volatility, sentiment has continued to deteriorate: “The probability of global stocks turning to a bear market is increasing,” said Masanari Takada, cross-assets strategist at Nomura Securities. “While some investors who look at fundamentals buy stocks on dips, there are other players who keep selling automatically in response to heightened volatility. At times like this, buyers can easily be overwhelmed by negative headlines on tariffs, etc.”

In FX, the dollar extended its recent advance as month-end flows that kicked off the London session lent support, sending the euro and sterling to fresh day lows. The common currency subsequently got brief support from regional German inflation data and rebounded while Antipodean currencies led gains in G-10. The dollar gained on a decline in the euro after news German Chancellor Angela Merkel would not seek re-election as head of her CDU party and a big miss in European GDP (Q3 GDP 0.2%, vs Exp. 0.4%). Merkel said she would not seek re-election as party chairwoman, heralding the end of a 13-year era in which she has dominated European politics.

Oil prices were mixed after easing overnight as Russia signaled that output will remain high and as concern over the global economy fueled worries about demand for crude. West Texas Intermediate crude futures dropped below $67/barrel, while Brent crude futures dipped 0.3 percent to $77.13.

Related Posts

Sherwin-Williams: A Dividend Aristocrat With Nearly 40 Consecutive Years Of Higher Payouts

Sherwin-Williams: A Dividend Aristocrat With Nearly 40 Consecutive Years Of Higher Payouts Fed: Mixed Messages

Fed: Mixed Messages The Road To Where Exactly?

The Road To Where Exactly? This Week’s Must-See Restaurant Earnings Charts

This Week’s Must-See Restaurant Earnings Charts- Gold On A Knife Edge Ahead Of FOMC Decision

- Advent/Claymore Enhanced Growth & Income Fund Announces Final Results Of Tender Offer

Leave A Comment