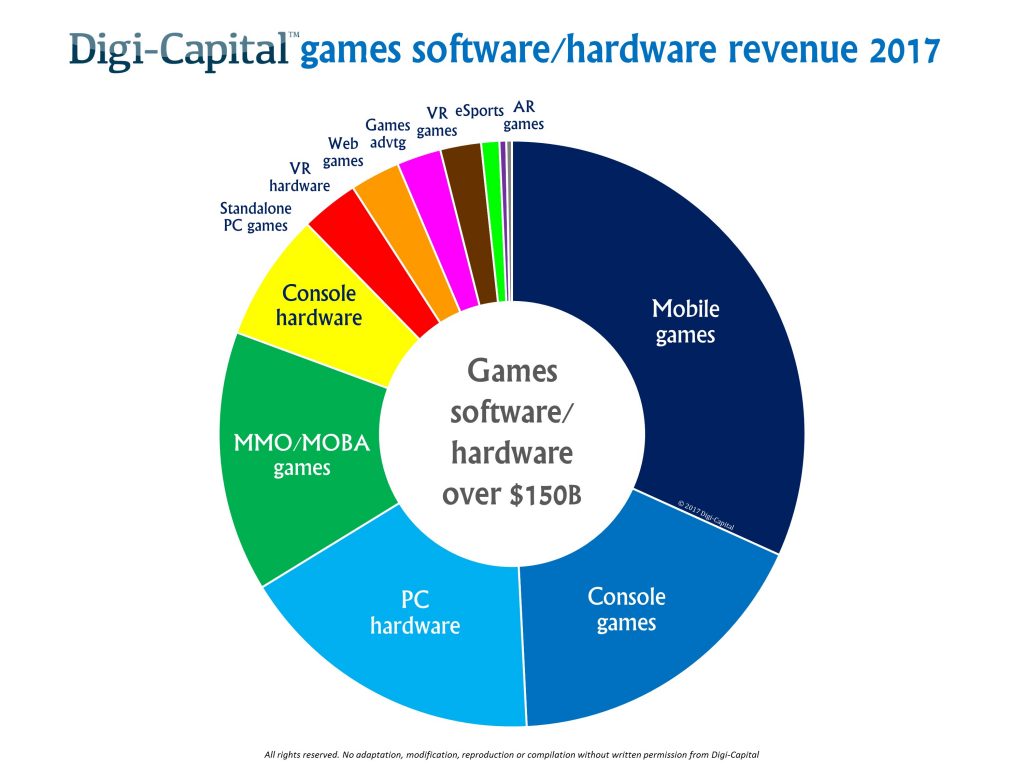

Games software/hardware combined are set to drive more than $150 billion revenue for the first time ever in 2017, with software taking around three-quarters and hardware around one-quarter of the total (Note: this is games software/hardware combined – non-hardware revenues could deliver over $110 billion globally this year). With a compound annual growth rate (CAGR) of 7.9% for the next 5 years, games software/hardware combined could top $200 billion by 2021 (as detailed in Digi-Capital’s new Games Report and Database Q3 2017).

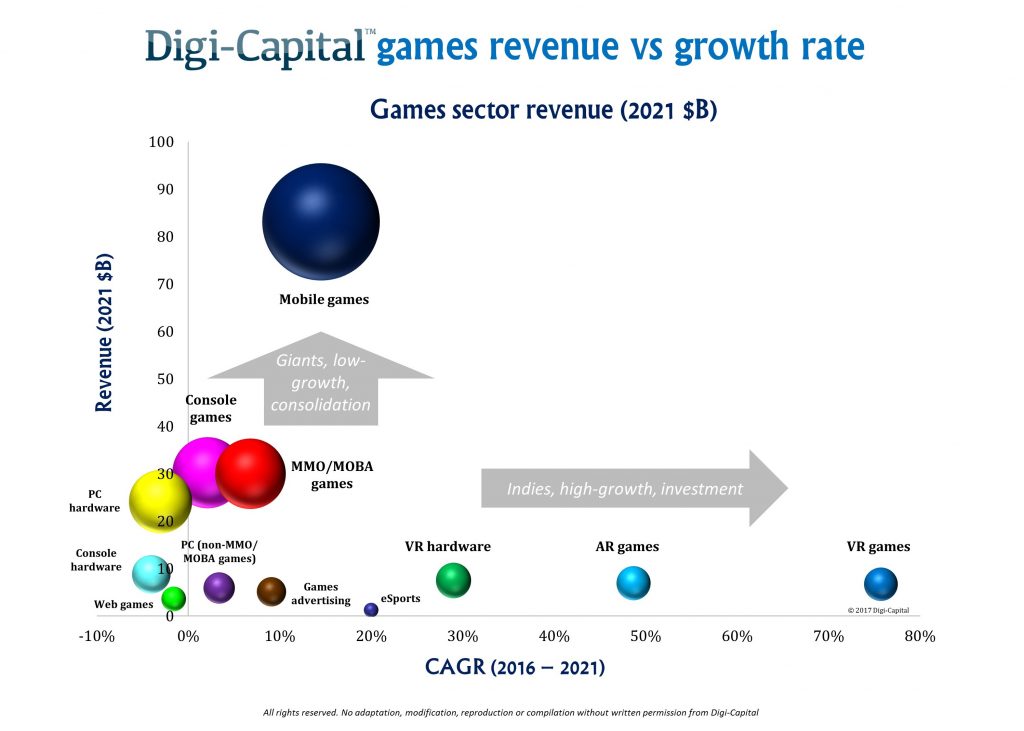

But not everyone’s a winner, as games has turned into a two speed market – giant sectors where giants rule, and small high-growth sectors where nimble indies can still make their mark.

Bigger than big, stronger than strong

Mobile games have grown like a weed since the launch of the iPhone, and could top $50 billion revenue for the first time in 2017. Yet despite this outperformance, mobile games growth could slow to 14.5% CAGR to reach over $80 billion by 2021 (gross apps revenue across iOS, Google Play, and all the Chinese app stores). That’s more revenue than the entire games software market when we first covered it back in 2010 (coincidentally when we first forecast mobile games’ coming dominance, which folks thought outrageous back then).

Console games and MMO/MOBA games should each deliver less revenue individually than mobile this year, and with slowing growth could each individually drive around $30 billion revenue in 5 years’ time. This could make mobile games bigger than console games and MMO/MOBA games combined by then. The remaining big sectors of PC hardware and console hardware are broadly ex-growth (although Nintendo Switch has given console hardware a big bump this year and might help longer term), but could still drive well over $30 billion combined revenue by 2021.

Small but perfectly formed

At the other end of the scale is the land of the indies, where there’s room for them to breath. There isn’t enough money yet for the big boys, a little like early mobile games.

Related Posts

E

Sunshine And Grouses

E

Sunshine And Grouses FTSE 100: Status Quo Maintained As 6054-6195 Range Dominates

FTSE 100: Status Quo Maintained As 6054-6195 Range Dominates- Stock Exchange: Oscar Loves Airlines, But Consider FAST And SLC

Housing Starts, Permits Plunge In February As Rental Units Crash

Housing Starts, Permits Plunge In February As Rental Units Crash Deutsche: “If Trust In Monetary & Political Stability Were Lost, People Would Turn To Cryptocurrencies”

Deutsche: “If Trust In Monetary & Political Stability Were Lost, People Would Turn To Cryptocurrencies” Bitcoin on-chain and options data hint at a decisive move in BTC price

Bitcoin on-chain and options data hint at a decisive move in BTC price

Leave A Comment