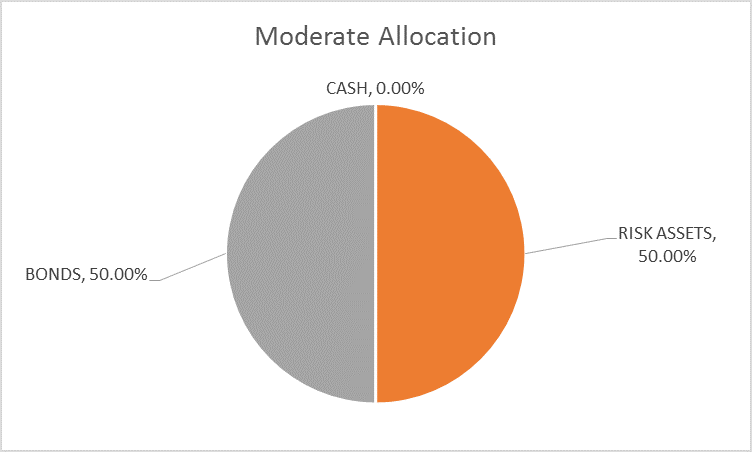

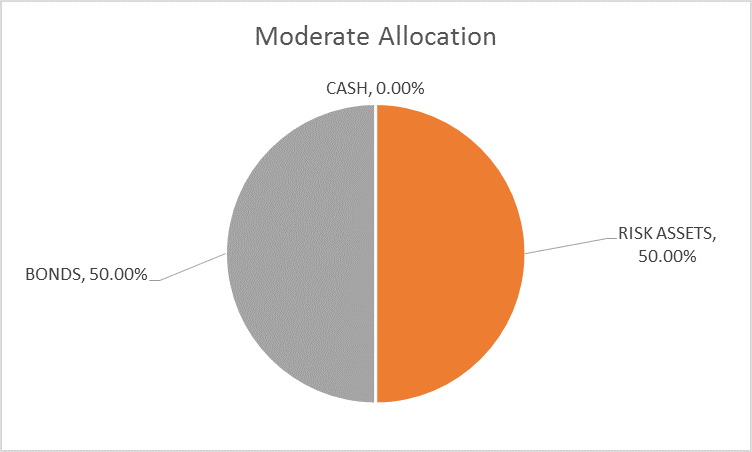

There is no change to the risk budget this month. For the moderate risk investor, the allocation between risk assets and bonds is unchanged at 50/50.

The Fed spent the last month forward guiding the market to the rate hike they implemented today. Interest rates, real and nominal, moved up in anticipation of a more aggressive Fed rate hiking cycle. Post meeting, a lot of the rise came out of the market. Nominal and real 10 year Treasury rates dropped by an identical 11 basis points on the day. Rates fell at the short end too as the yield curve shifted lower but didn’t flatten significantly. The market was looking for a big change in the Fed’s growth and inflation expectations and the dots basically didn’t move. Long term growth expectations are still 1.8-2.0% and inflation expectations were unchanged at 2.0% on the PCE deflator.

Just as or maybe more important was the emphasis in the statement on its “symmetric” inflation target. Rather than say, as they did in the last statement, that inflation was expected to “rise to 2% over the medium term”, the Fed now says “inflation will stabilize around 2%”. I know it seems like a minor change but what it means is that the Fed isn’t going to get too excited if the inflation rate goes above 2% for a period of time. They further emphasized the point by saying:

The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

What all the language changes mean is the Fed isn’t really shifting to a more hawkish stance and that rate hikes will not be coming fast and furious this year. The dot plot indicates the Fed still expects two more hikes this year. The market was starting to price in four (today’s plus two more) and that had to come out of the market after the meeting. This was the most dovish rate hike in the history of rate hikes. Greenspan’s old conundrum was that long term rates weren’t rising as the Fed hiked. The conundrum today is that even short term rates aren’t rising as the Fed hikes. Two year note yields are right back to where they were after the December rate hike.

Related Posts

Plunging Birth Rates Confuse Economists But Are Actually Great News

Plunging Birth Rates Confuse Economists But Are Actually Great News Liechtenstein Bank Offers “Direct” Cryptocurrency Investment And “Cold Storage” Wallet

Liechtenstein Bank Offers “Direct” Cryptocurrency Investment And “Cold Storage” Wallet Why Small-Cap Put Writing Indexes Make Sense

Why Small-Cap Put Writing Indexes Make Sense SP 500 And NDX Futures Daily Charts – And Here’s The Bounce

SP 500 And NDX Futures Daily Charts – And Here’s The Bounce- Nikkei Trades Lower On Core Machinery Orders

- When and why did the word ‘altcoin’ lose its relevance?

Leave A Comment