In JP Morgan’s Quarterly Market Guide a pair of charts on page 31 caught my eye.

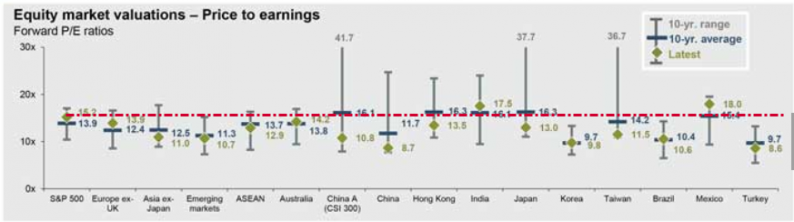

Forward PE Estimates

I don’t have any faith in forward PE estimates. They tend to be overly optimist and subject to numerous “one-time” writeoffs.

Instead, I recommend watching 10-year smoothed PE ratios. See discussion below.

Nonetheless, please note that even on a forward-basis, the S&P 500 ratio is well above most other markets.

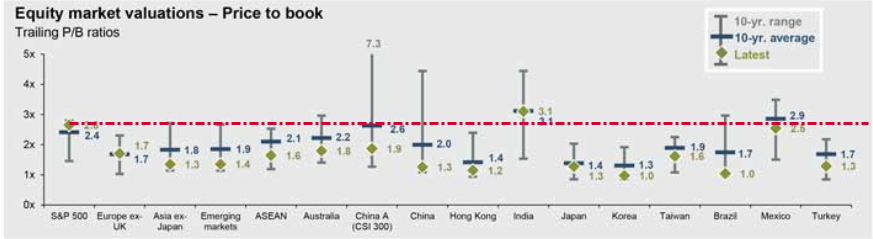

Price to Book Valuations

On a price-to-book basis, US equities are twice as expensive as numerous other markets.

Case-Shiller Smoothed PE

The Case-Shiller PE is a Cyclically Adjusted Price-to-Earnings ratio, commonly known as CAPE, Shiller P/E, or P/E 10 ratio.

To calculate “CAPE”, you divide the current price by the inflation-adjusted average of the last ten years of earnings.

Here is a link to the Current Shiller PE, updated daily. A better-looking chart is shown below.

Bubble Debate Revisited

Doug Short at Advisor Perspectives does periodic updates to the Shiller PE. His latest was on October 1 in Is the Stock Market Cheap?

On a PE/10 basis stocks are in the fifth quintile range signalling extreme overvaluation. Higher smoothed PEs happened in 1929, the dot-com bubble, 1902, and earlier this year.

The historic P/E10 average is 16.6. After dropping to 13.3 in March 2009, the ratio rebounded to an interim high of 23.5 in February of 2011 and then hovered in the 20-to-21 range. It began rising again in late 2013 and hit a new interim high of 27 in February of this year. It has now dropped below that high.

Of course, the historic P/E10 has never flat-lined on the average. On the contrary, over the long haul it swings dramatically between the over- and under-valued ranges. If we look at the major peaks and troughs in the P/E10, we see that the high during the Tech Bubble was the all-time high above 44 in December 1999. The 1929 high of 32.6 comes in at a distant second. The secular bottoms in 1921, 1932, 1942 and 1982 saw P/E10 ratios in the single digits.

Related Posts

E

S&P 500 Trading In A Temporary Correction

E

S&P 500 Trading In A Temporary Correction The Yin And Yang Of The US-China Relationship

The Yin And Yang Of The US-China Relationship E

Celator Pharmaceuticals Soars 300% On Positive Phase 3 Results In High-Risk AML Patients

E

Celator Pharmaceuticals Soars 300% On Positive Phase 3 Results In High-Risk AML Patients S&P Futures, Global Stocks, Euro Dragged Lower By Deutsche, Geopolitics, French Election Worries

S&P Futures, Global Stocks, Euro Dragged Lower By Deutsche, Geopolitics, French Election Worries E

After Just Two Months Of Futures Contracts, It Appears Wall Street Does Have Some Control Over The Bitcoin Price

E

After Just Two Months Of Futures Contracts, It Appears Wall Street Does Have Some Control Over The Bitcoin Price Will Market Erosion Create Incised Meanders?

Will Market Erosion Create Incised Meanders?

Leave A Comment