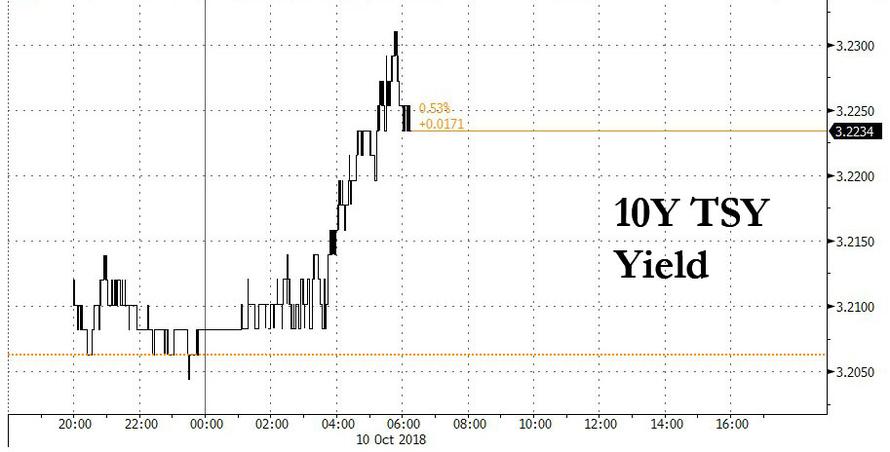

Global markets entered Wednesday in tentative fashion as US Treasury yields resumed their upward march after dropping the day before ahead of a closely watched US CPI report and as the US Treasury prepared to sell more debt to fund the soaring US deficit.

The mood in stocks soured, and European equities turned lower with American futures as Asian peers erased an advance while world stocks inched off eight-week lows; market gains were checked by fears for global economic growth, greater US decoupling, escalating trade war and the possibility of an Italy-EU clash over budget spending. The result was generally a sea of red among global capital markets in early trading.

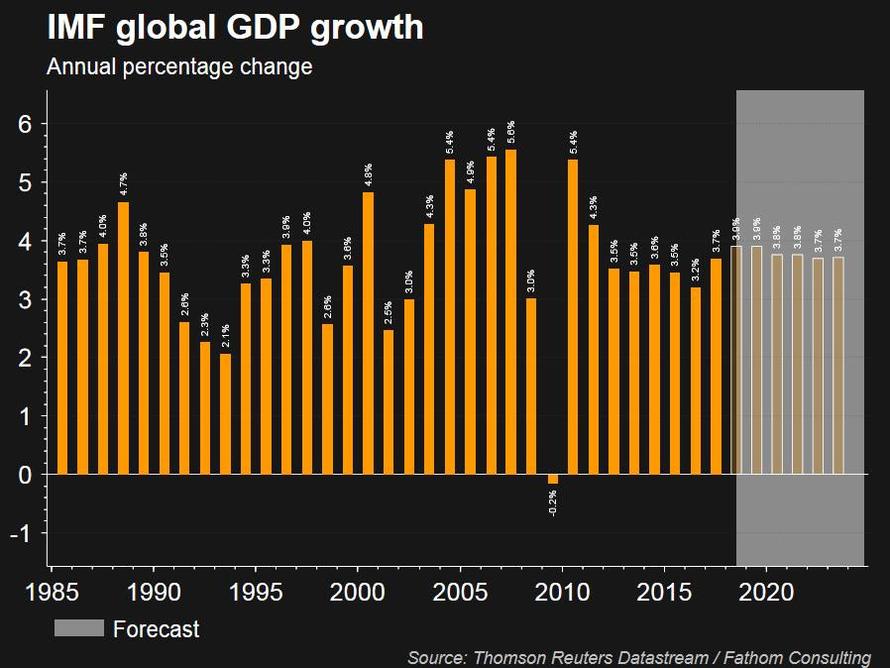

The equity rout that resulted from the global bond selloff that took bond yields to seven-year highs this week were exacerbated by continued growth concerns arising from trade conflicts and $80-per-barrel oil, with the IMF cutting its world GDP forecasts for the first time in two years.

The yield on 10-year Treasurys resumed its ascent to 3.23% from 3.20%, after falling for the first time in a week on Tuesday, putting a lid on early trader optimism.

“We are at some sort of critical moment, a crossroads, for bond and equity markets,” Marie Owens Thomsen, global head of economic research at Indosuez Wealth Management, said noting that while U.S. 10-year yields at 2% unequivocally favored equity investment, this was not so above 3%. “This January we took out the 2 percent (yield) handle and now we are wondering if we are permanently taking out the 3 percent handle as well. That makes the climate for equities much more challenging.”

The MSCI world equity index rose 0.14% after four days in the red. However, while Japan’s Nikkei and MSCI’s Asia-Pacific index outside Japan rose 0.2-0.3 percent, European shares slipped 0.2 percent, undermined by more bellicose rhetoric from Italian politicians.

The Stoxx Europe 600 Index dropped as most sectors turned lower. The European basic resources index (SXPP) – which was one of the best-performing sectors since the end of August – fell as much as 2.2%, one of Wednesday’s main sector laggards, as investors rotated toward defensive sub-groups including telecoms and health care. Milan-listed stocks traded between gains and losses, rising off 18-month lows hit earlier in the week.

Europe’s weakness followed a modest recovery of bullish sentiment in Asia, as shares in Japan rose after four days of losses, South Korean equities slumped as trading resumed after a holiday while those in China closed 0.2% higher after fluctuating between gains and losses before edging barely up after early gains slipped with lithium-related stocks tumbling, while Tencent suffered a record ninth day of declines in Hong Kong.

The retreat in emerging markets took a pause on Wednesday after Donald Trump said the Fed is moving too fast on rate hikes and as traders awaited U.S. inflation data before taking a stance on riskier assets. Equities slowed their drop and currencies eked out their first gain this week, led by India’s rupee

The yuan slipped against the dollar for the fifth session out of the past six to approach four-year lows hit in August, unresponsive to Mnuchin’s warning on devaluation. The focus is on next week’s semi-annual U.S. report on currencies amid Treasury officials’ comments that recent yuan depreciation has raised concerns in Washington.

The backdrop to global markets is still dominated by deepening U.S.-China tensions and a surge in volatility for stock and bond markets. While the Treasury rout has eased, a glut of new U.S. debt is coming to the market this week. American producer and consumer price data is also due in the next two days and may determine where yields go from here.

“After President Trump once again criticized the Fed for raising rates too fast and he reiterated his preference for low borrowing costs, U.S. bond yields fell from their recent highs,” Rabobank strategist Piotr Matys wrote in a note. “This, in turn, provided the emerging-market currencies with respite. However, looking from the perspective of technical analysis the price action implies that U.S. 10-year Treasuries have entered a period of consolidation.”

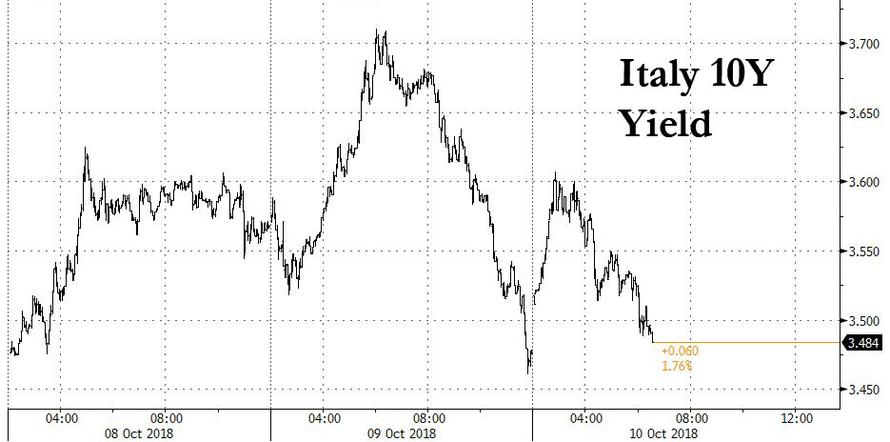

Italian bonds initially dropped and bear flattened beyond the belly after Deputy PMs Salvini and Di Maio said the budget plan won’t change and there’s no going back, suggesting an unwillingness to compromise. Italy’s 10y spread to Germany blew out to 305bps, after Di Maio said that “our objective is not the spread, but the citizen… We expect that the economic growth rate will be higher” with measures included in the next year’s budget plan.

However, the initial weakness reversed in a repeat of Tuesday’s action after Finance Minister Giovanni Tria, speaking before the parliament’s joint budget committee, pledged action to restore calm should market turbulence escalate into financial crisis. Yields slipped further after Tria said he expected “collaboration” with the EU on the budget issue, and added that “the rise in government bond yields recorded in the last few days is certainly a reason for concern, but I want to reiterate that it was an excessive reaction which is not justified by the fundamentals of Italy’s economy and public finances.”

That said, markets’ pressure has not dissuaded the government from a bigger-than-expected budget deficit as ministers’ comments indicated they are prepared to defy European Union critics. The developments have raised risks of a credit ratings downgrade for the country, with a knock-on effect for Italian banks which are big holders of government bonds. However, the banks’ shares received a boost after an EU official told Reuters regulators were “intensely” monitoring Italian banks’ liquidity levels but there was no cause for alarm.

Leave A Comment