Gold is challenging the $1300 level for the third time this year. If it breaks upwards out of this consolidation phase convincingly, it could be an important event, signalling a dollar that will continue to weaken.

The factors driving the dollar lower are several and disparate. The US economy is sluggish relative to the rest of the world, the rise of Asia from which America is excluded is unstoppable, geopolitics are shifting away from US global dominance, and the end is in sight for monopolistic payment for oil in US dollars.

These subjects have been covered in some detail in my recent articles, which will be referred to for further clarification where appropriate. This article summarises these trends, and explains why the consequence appear certain to drive gold, priced in dollars, much higher.

The importance of gold and reasons for its suppression

The post-war Bretton Woods Agreement confirmed the US dollar to be fixed to gold at $35 per ounce. All other national currencies were linked to gold through the dollar at the central bank level. Ordinary civilians, businesses and commercial banks were not permitted to exchange their currencies for gold through central banks, so this was simply a high-level arrangement designed to maintain control of gold priced in dollars.

A few years after Bretton Woods, in 1949 and when the newly-fledged IMF began to collate statistics on national gold reserves, the US Treasury was recorded owning 21,828.25 tonnes of gold, 74.5% of all central bank reserves, and 43.6% of estimated above-ground gold stocks. However, over the years the proportions changed, and by 1960, US gold reserves had declined to 15,821.9 tonnes, 47% of central bank reserves, and 24.9% of above ground stocks.

Clearly, American control of gold had weakened considerably in the two decades following Bretton Woods. This weakening continued until the failure of the London gold pool, the arrangement dating from 1961 whereby the major American and European central banks collaborated to defend the $35 peg. The Americans had abused the gold discipline by financing foreign ventures, notably the Korean and Vietnam wars, not out of taxation, but by printing dollars for export, and it began to put pressure on the dollar. The London gold pool effectively spread the cost of maintaining the dollar peg among the Europeans. Unsurprisingly, France withdrew from the gold pool in June 1967, and the pool collapsed. By the end of that year, the US Treasury was down to 10,721.6 tonnes, 30% of total central bank gold reserves, and 15% of above-ground stocks.

Inevitably the decline continued, and by the time of the Nixon shock (August 1971 – the abandonment of the gold exchange commitment) it was clear the US Government had lost control of the market. She had only 9,069.7 tonnes left, representing 28.3% of central bank gold, and 11.9% of above ground stocks. Monetary policy switched from the fixed parity arrangements centred on gold through the medium of the dollar, to a propaganda effort aimed at removing gold from the monetary system altogether, replacing it with an unbacked dollar as the international reserve standard.

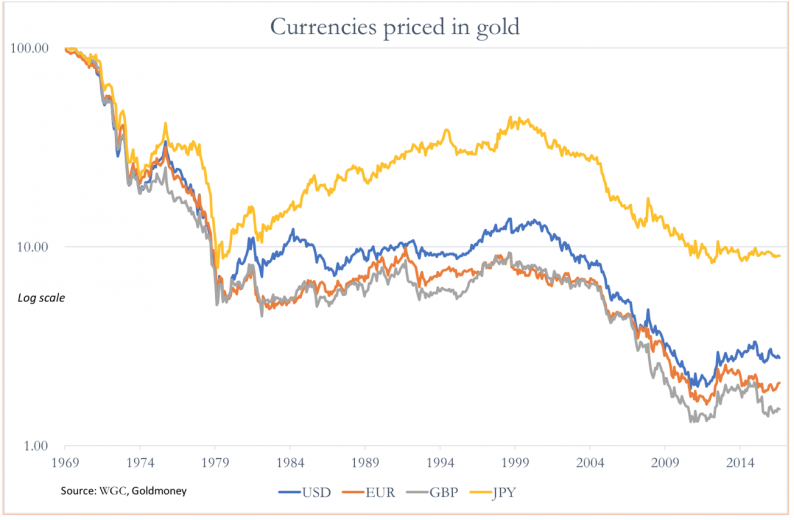

The result was the purchasing power of the dollar and the other major currencies measured in gold has all but collapsed, as shown in the chart below.

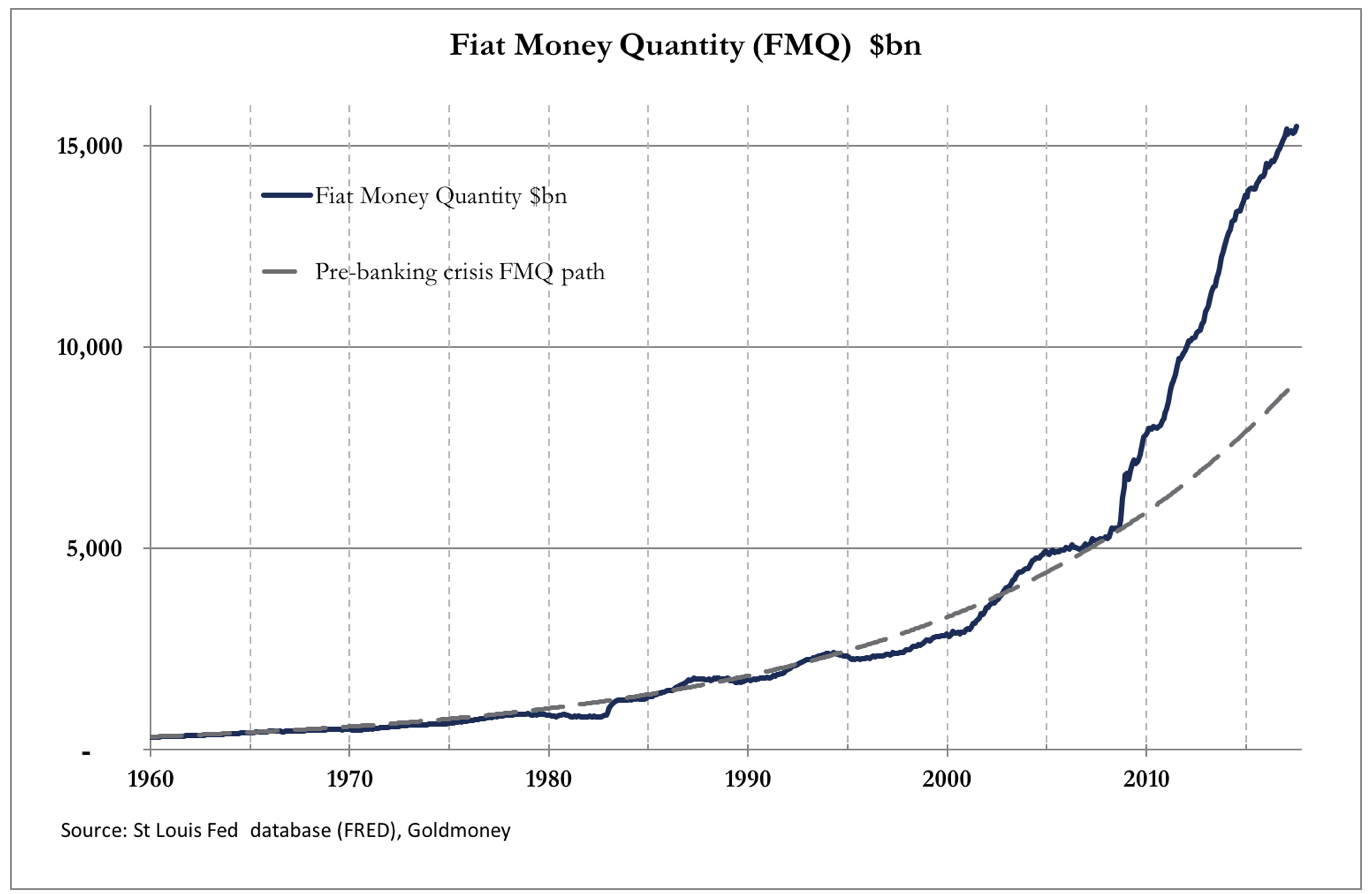

Between 1969 and today, the dollar’s purchasing power relative to gold declined by 97.3% (the blue line). By banning gold from having any monetary role, the US removed price stability from the dollar. More recently, since the great financial crisis the quantity of fiat money in the global currency system has expanded dramatically relative to the long-term average growth rate of money and bank credit. This is illustrated in our second chart, which records the growth in the total amount of fiat dollars in the US banking system.

The fiat money quantity is the sum of true money supply and commercial bank reserves held at the central bank (the Fed). It is the measure of all deposits, including those of the commercial banks. Monetary inflation has expanded dramatically since the great financial crisis, illustrated by its acceleration above the long-term trend. The consequences for the dollar’s purchasing power in time will be to accelerate the dollar’s decline even more.

The monetary expansion of the dollar has been echoed in the other major currencies, with negative consequences for global price inflation in the coming years. Meanwhile, gold’s inflation, at roughly 3,200 tonnes annually, is about 1.9% of above-ground stocks. The different rates of increase between above-ground gold stocks and the fiat money quantities of unbacked state-issued currencies is what ultimately drives the price of gold measured in those unbacked currencies. It is easy to see why a higher gold price, reaffirming gold’s role as sound money at a time of excessive fiat currency inflation, is viewed by the major monetary authorities as a potential threat to their currencies’ credibility.

There can be little doubt that without the propaganda war against gold led by the US monetary authorities, without the expansion of unbacked paper gold constituting artificial gold supply in the futures and forwards markets, and without the secret interventions of the US’s Exchange Stabilisation Fund, the gold price would be considerably higher, expressed in dollars.i

However, gold remains centre-stage as a global hedge against the decline in purchasing power of fiat currencies. Besides rescuing the financial system from collapse nine years ago, the expansion of bank credit is inherently cyclical.ii The credit-cycle for China’s yuan appears to be moving into a new expansionary phase, reflected in a rising trend for nominal GDP. This will be put into context later in this article, but it is noticeable that on the back of China’s GDP growth, Japan, the EU and the UK are also enjoying export-led revivals.

The US does not share these benefits, partly because China and Russia, the founders of the Shanghai Cooperation Organisation (SCO), are deliberately freezing America and her money out, and partly because of America’s own tendency towards trade isolationism.iii It is, therefore, less certain that America is close to moving from the recovery stage of the dollar’s credit cycle into expansion. In the absence of other factors, the difference in interest rate outlooks this implies should be reflected in a declining dollar exchange rate against the other major currencies, a trend that has been under way since last January.

Despite the massive expansion of fiat money over the last nine years, it is possible for governments to stabilise the future purchasing power for their currencies. It will require their fiat currencies to be tied convincingly to the characteristics of gold. It depends on the government concerned accepting that gold is superior money to its own currency, owning sufficient physical gold reserves to convince the markets, and the gold price being at a level where the arrangement sticks. There is no doubt that China, Russia, as well as the other SCO member states and their populations regard gold as a superior money to fiat currencies, partly because their fiat currencies do not have well-established records of objective exchange value.

In the US, Japan, the UK and through much of Europe, the populations have experienced a longer, generally more stable objective exchange value for their currencies. Under pressure from their governments to use only state-issued currency, they have lost the habit of regarding gold as money. The monetary authorities of these countries, with a few exceptions, also do not regard gold as having any monetary role at all, beyond paying lip-service to a vague concept it has value as an asset which is no one else’s liability.

Leave A Comment