It’s time for another update on how corporate America intends to spend the windfall from the GOP tax cuts which the Trump administration variously pitched as a “middle class miracle” despite the fact that trickle down economics literally never works out as planned and despite the fact that independent analysis shows that the benefits of the tax cuts will accrue disproportionately to the wealthy.

As a reminder, here’s what your “middle class miracle” will look like in terms of the distribution of benefits within 10 years:

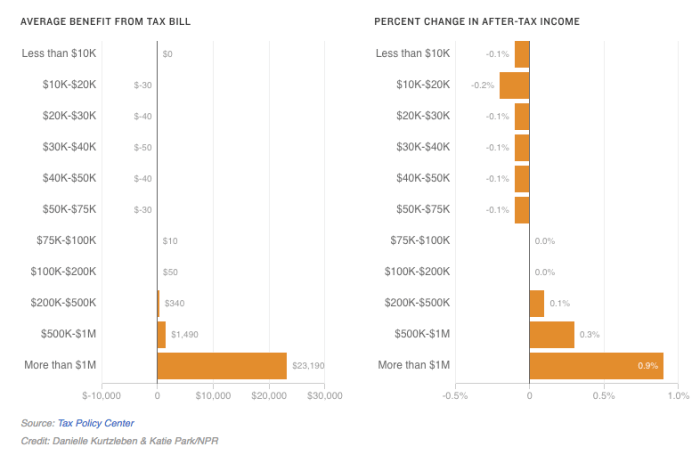

So by 2027, Trump’s tax cuts will actually raise taxes on 53% of households. Here’s the tax policy center’s assessment:

2027

On average, taxes would be little changed for taxpayers in the bottom 95 percent of the income distribution. Taxpayers in the bottom two quintiles of the income distribution would face an average tax increase of 0.1 percent of after-tax income; taxpayers in the middle income quintile would see no material change on average; and taxpayers in the 95th to 99th income percentiles would receive an average tax cut of 0.2 percent of after-tax income. Taxpayers in the top 1 percent of the income distribution would receive an average tax cut of 0.9 percent of after-tax income, accounting for 83 percent of the total benefit for that year.

But hey, that’s fine, right? I mean after all, labor gets a one-time $1,000-ish bonus (or, more to the point, a rounding error on C-Suite paychecks) and also free Ding Dongs for a year. And you can’t really put a price on free Ding Dongs.

As far as investors are concerned, the question is how companies are going to spend their tax savings. The short answer is that a lot of it is going to be returned to shareholders, but there’s some good news on the capex front. Nominally speaking, capital spending will be the largest single use of cash. Here’s Goldman:

MMM, JNJ, and NOC are examples of companies that intend to increase investment spending in 2018 as a result of corporate tax reform. Aside from tax-related optimism, the fundamental drivers of capex also remain firm. Lending standards are easy: the Federal Reserve Board’s Senior Loan Officer Survey indicates lending standards continued to loosen during the past 12 months. S&P 500 return on equity (ROE) excluding Financials and Energy equals 21%, the highest level in more than 40 years. In addition to growing capex investment, we expect companies will increase R&D expenditures by 10% to $325 billion (13% of total cash spending).

Leave A Comment