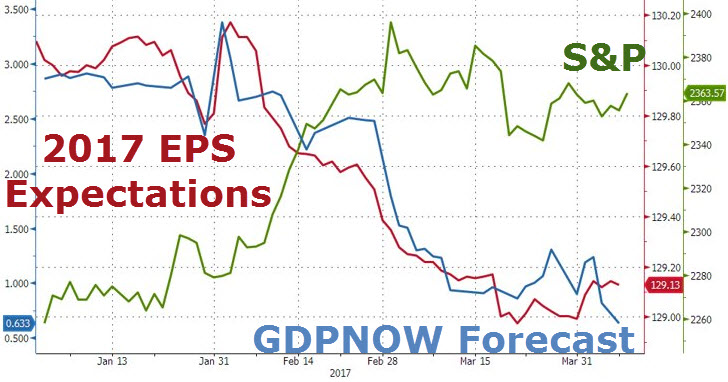

With 2017 EPS expectations at 2017 lows, 2017 GDP expectations at 2017 lows…

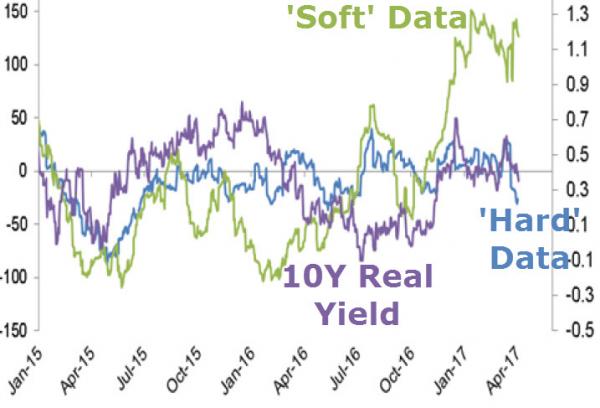

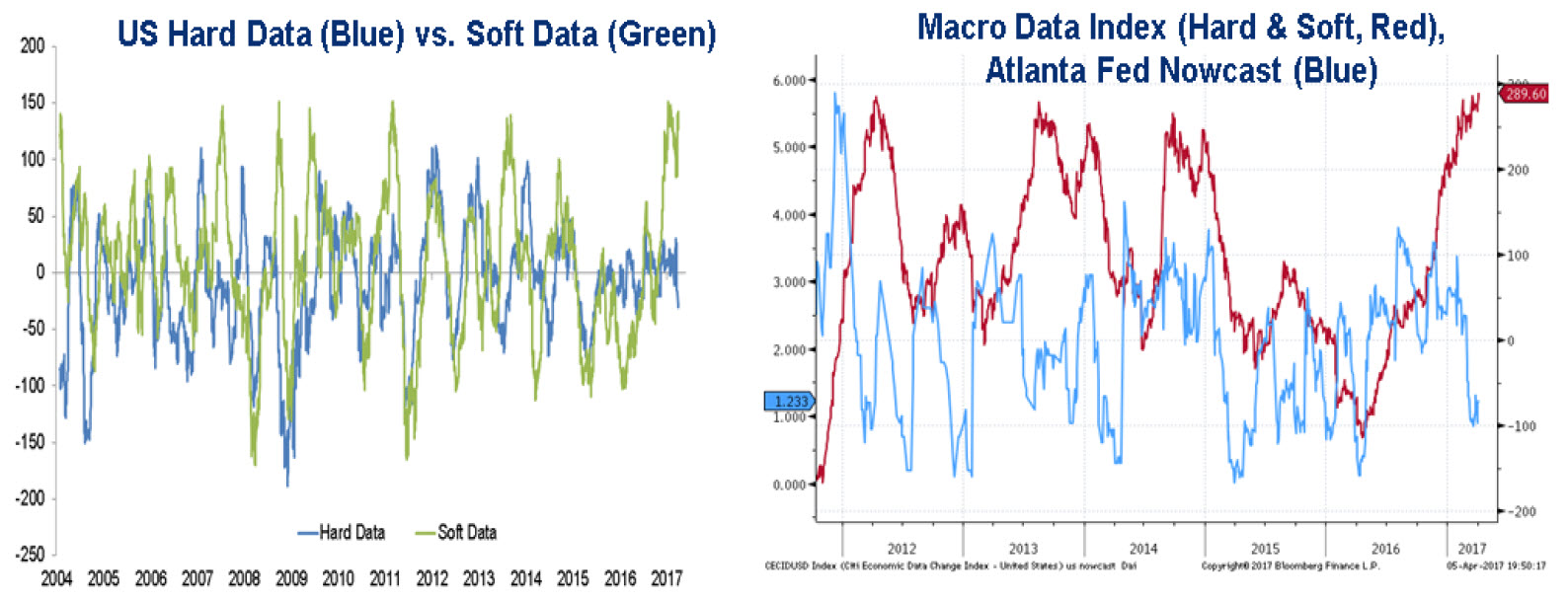

And real bond yields at 2017 lows, it should hardly be surprising that ‘hard’ economic data has collapsed to its lowest level in over a year.

What should be surprising is the equity market’s desperate clinging to ‘soft’ survey data’s high hope levels…

Asa Citi’s Amir Amin notes, much of the repricing across asset markets post-November’s election was as a function of faith-based “animal spirits” as opposed to economic fundamentals. Price action momentum in a number of markets seems to have now stalled, however.

What does potentially concern us is the gap between hard and soft data surprises in the US. For some time now we have been tracking this disparity in data, however, more worryingly the hard-data surprise index has turned into negative territory.

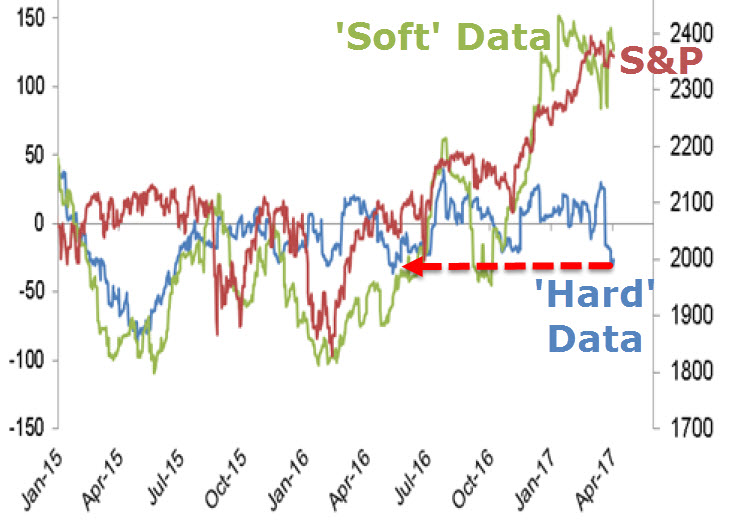

But the hard vs. soft surprise index isn’t the only place we are seeing divergences.

The Atlanta Fed Nowcast languishes at 1.2%, not far from the 2016 lows. Meanwhile, the macro data index is at cyclical highs (right had chart above). We saw divergences like this (macro index making higher highs, Nowcast making lower lows), notably in 2012 but also to some extent in 2013. For equity markets, in 2012 a ~10% correction ensued, whilst in 2013, 2 smaller corrections of ~5% followed. Similarly, 2012 saw 10y UST yields fall ~90bps and ~50bps twice in 2013. Both occasions the Nowcast acted as a leading indicator.

Our fear now, of course, is despite rampant optimism in the US, the data just hasn’t delivered.

Unless we start seeing hard data momentum increase, our view on risk assets may not be as sanguine.

Related Posts

Q&A: The one word that’ll make more big brands jump into crypto

Q&A: The one word that’ll make more big brands jump into crypto Thoughts On Bed Bath And Beyond Here

Thoughts On Bed Bath And Beyond Here Prime Working Age Employment Up, Participation Up (Finally) – Now How About Wages?

Prime Working Age Employment Up, Participation Up (Finally) – Now How About Wages? Comprehensive Bulltargets.com Reviews: A Complete Insight into the Forex Broker

Comprehensive Bulltargets.com Reviews: A Complete Insight into the Forex Broker EUR: Pillars For EUR/USD Bull Case Have A ‘Shaky Foundation’ – Barclays

EUR: Pillars For EUR/USD Bull Case Have A ‘Shaky Foundation’ – Barclays Stock Market Crash 2015: The Dow Has Already Plummeted 2200 Points From The Peak

Stock Market Crash 2015: The Dow Has Already Plummeted 2200 Points From The Peak

Leave A Comment