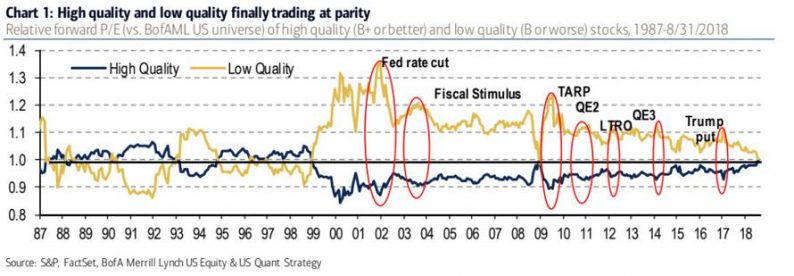

In the rational world of textbook investing, investors should pay up for safety and be compensated for risk, but for the past 20 years, the opposite has been the case in US equity markets.

As BofA’s Savita Subramanian notes, the market has tried to get rational, but, as the chart below shows, each time it was thwarted by some plunge-protection-driven fiscal or monetary stimulus.

But that ‘irrational’ gap has finally closed…

High-quality trades in line with low quality for the first time since ’99.

Now what?

Despite the fact that high-quality stocks have outperformed low-quality stocks in recent years, fund managers are still more overweight low-quality stocks (B or Worse) than high-quality stocks (B+ or Better) although their hedge may be a slight overweight in A+ ranked companies.

So there is plenty of ammo for this to run with a push towards ‘high quality’, and further, as BofA notes…

Assuming upward pressure on the cost of capital as the Fed and other central banks shift from quantitative easing (QE) to quantitative tightening (QT), cash-rich self-funded companies are likely to re-rate and trade at premia to their levered,super-cyclical counterparts.

As we noted above, investors should pay up for safety and be compensated for risk, and as the chart at top shows, in the decades before the Tech Bubble, high-quality stocks traded at fairly consistent premia to the market (and low quality traded at a discount) for the majority of that time.

And in times of volatility, high-quality stocks have outperformed…

And judging by the yield curve – which has historically predicted cyclical volatility – it would appear quality is the best hedge.

Volatility is driven by factors that the yield curve forecasts, like growth and risk. A steepening yield curve typically reflects increasing growth expectations and risk appetite, which have a dampening effect on volatility; a flattening yield curve typically reflects decreasing growth expectations and building risk aversion, which tend to have an amplifying effect on volatility.

Related Posts

Two Interest Rate Hikes, Rather Than One, Could Be In The Cards – Here Are The Ramifications

Two Interest Rate Hikes, Rather Than One, Could Be In The Cards – Here Are The Ramifications GBPJPY: Weakens, Further Corrective Pullback Envisaged

GBPJPY: Weakens, Further Corrective Pullback Envisaged Stocks And Precious Metals Charts – The Primacy Of Conscience

Stocks And Precious Metals Charts – The Primacy Of Conscience E

RXi Pharmaceuticals: Extreme Volatility Attracts Traders, But Long-Term Worries Persist

E

RXi Pharmaceuticals: Extreme Volatility Attracts Traders, But Long-Term Worries Persist- Price analysis 5/5: BTC, ETH, BNB, XRP, ADA, DOGE, MATIC, SOL, DOT, LTC

Gold Fund Inflows Surge To Highest Of The Year

Gold Fund Inflows Surge To Highest Of The Year

Leave A Comment