“Davidson” submits:

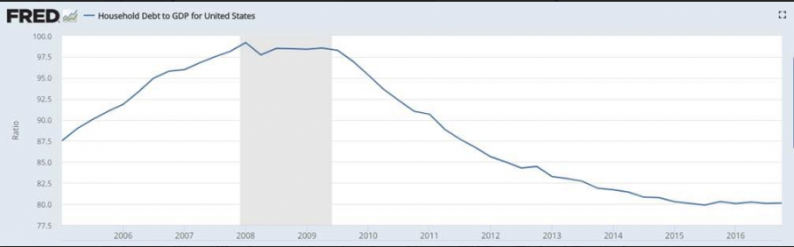

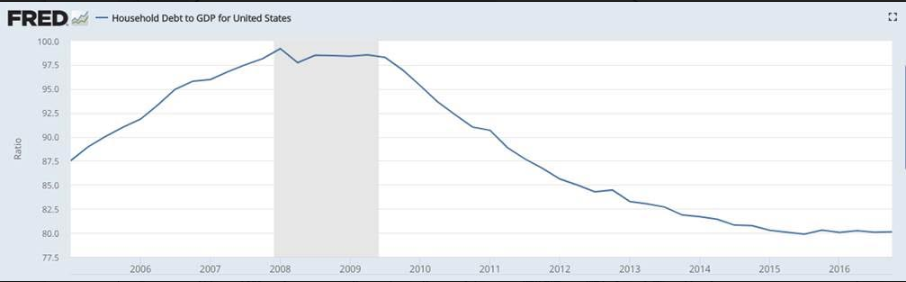

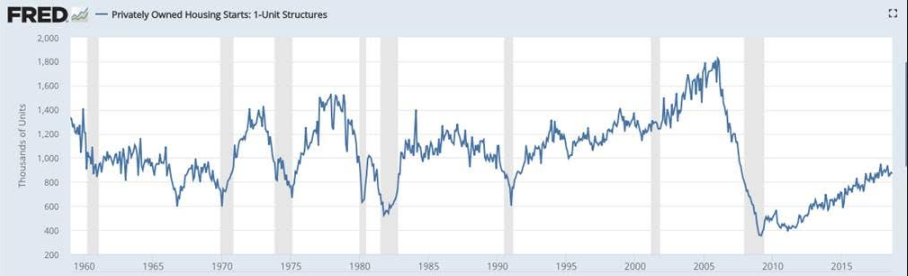

One good measure of indebtedness and risk to financial markets is the Household Debt to GDP Ratio (Percentage). Dodd Frank has not permitted the normal level of mtg lending we have experienced prior to the Sub-Prime surge. So restrictive has it been that starts at this part of the housing cycle remain the lowest since 1960. We should see something north of 1.6mil but we have ~800,000. This shows up in Household Debt to GDP as being the lowest since 2005 and no sign of having risen this cycle.

What kicks every economy into correction has always been bad debt not being able to be papered over which results in their default. This occurs when the T-Bill/10yr Treasury rate spread narrows to 0.2% or less and further lending is choked-off thus revealing the bad debt.

Financially, the US is in very good shape. It is China and other foreign markets which carry high debt. The US, being the consumption driver globally, drives the economic/economic cycle. Even with China’s debt, the US is not much at risk with the goal of lowering global tariffs. China does not control the US economy because the level they import is much less than what we import from them. Chinese investors do impact global markets when they pull capital back to China, but not economic trends.

Related Posts

Yuan Eyes On Chinese PMI, More Weakness Likely

Yuan Eyes On Chinese PMI, More Weakness Likely Deutsche Expects Quick Response From Intel On Register Story

Deutsche Expects Quick Response From Intel On Register Story Klaytn death cross debut coincides with a 57% KLAY price pump

Klaytn death cross debut coincides with a 57% KLAY price pump Cyber-Criminals Abandon Bitcoin; Homeland Admits “It’s A Lot More Legitimate Than People Think”

Cyber-Criminals Abandon Bitcoin; Homeland Admits “It’s A Lot More Legitimate Than People Think” Retail Sales Report- Great July

Retail Sales Report- Great July MoviePass Majority Owner Rises After Canaccord Says Buy

MoviePass Majority Owner Rises After Canaccord Says Buy

Leave A Comment