After we first reported last week that US credit card, student and auto debt all hit record highs in December of 2017…

… it should not come as a surprise that according to the just-released latest quarterly household debt and credit report by the NY Fed, Americans’ debt rose to a new record high in the fourth quarter on the back of an increase in virtually every form of debt: from mortgage, to auto, student and credit card debt (although HELOCs posted a tiny decline).

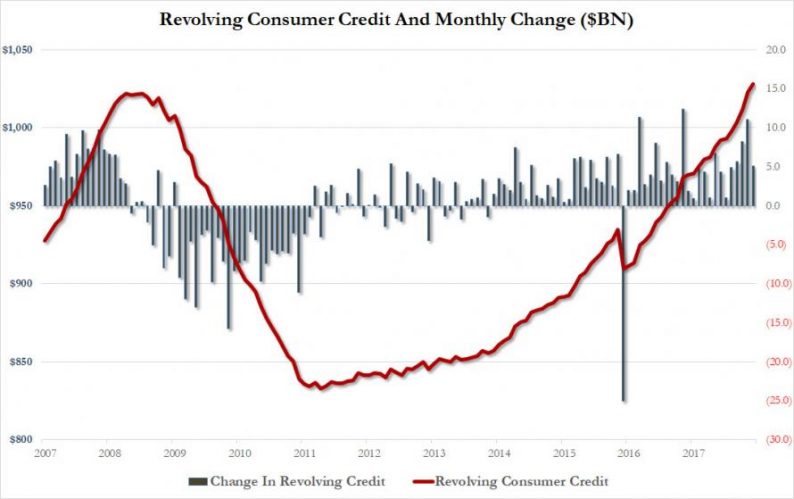

Aggregate household debt increased for the 14th straight quarter, rising by $193 billion (1.5%) to a new all-time high, and as of December 31, 2017, total household indebtedness was $13.15 trillion, an increase of $572 billion from a year ago – the fifth consecutive year of increases – equivalent to 67% of US GDP, versus a high of around 87% in early 2009. After years of deleveraging in the wake of the 2007-09 recession, household debt has risen more than 18% since the trough hit in the spring of 2013.

Some more big picture trends:

There were some red flags of caution: confirming recent negative data from Wells Fargo, and suggesting that the housing recovery is stalling, mortgage originations were at $452 billion, down from $479 billion in the third quarter.

Also troubling: There were $137 billion in auto loan originations in the fourth quarter of 2017, a small decline from 2017Q3 but making 2017 auto loan origination volume the highest year observed in our data.

Leave A Comment