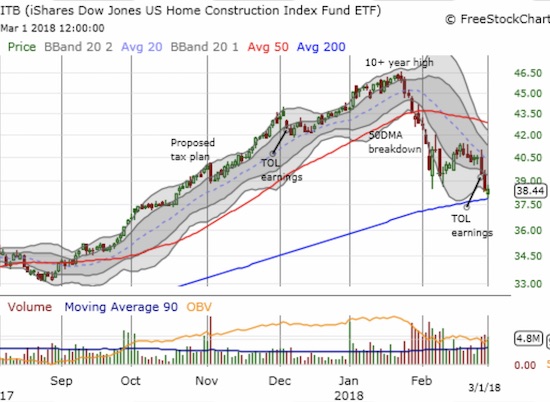

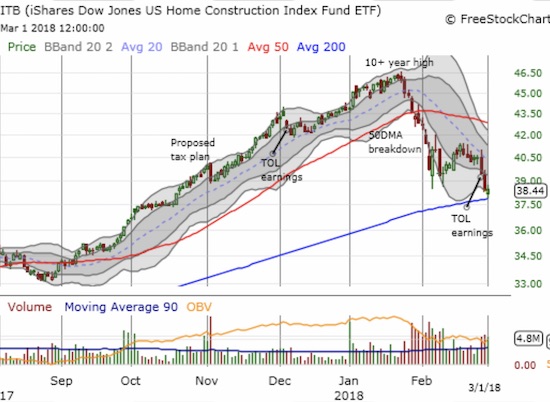

The last Housing Market Review covered data reported in January 2018 for December 2017. At the time, I described the ominous breakdown of the iShares U.S. Home Construction ETF (ITB), but I was not yet ready to connect the dots on the bearish implications. I am now.

ITB has continued its breakdown by first severely underperforming the stock market’s rally from oversold conditions and now closing at a fresh 4-month low.

The iShares US Home Construction ETF (ITB) managed to bounce off support at its 200-day moving average (DMA)…but how long can this support last?

While housing-related stocks were able to power through higher rates and expectations of higher rates, investor sentiment has now turned sour. It seems investors are preparing for a much less favorable rate environment. Risk tolerances seem to be shrinking and turning against home builders. During February, several home builders reported earnings and almost none were received favorably. The most telling churn came from Toll Brothers (TOL) which rallied at first in response to its earnings report but then ended the day down 5.1%. The pattern was a double-whammy as it confirmed resistance at the 50-day moving average (DMA) and created a bearish engulfing pattern. Like ITB, TOL bounced off its 200DMA support, but I have little expectation that the selling ends here.

Toll Brothers (TOL) quickly lost over 10% from its post-earnings intraday high. If support fails at the 200DMA, TOL has little support until last summer’s consolidation between $37 and $41.

The housing data in February failed the cause as well. Homebuilder sentiment held its own. Housing starts gained but are at the bottom of the uptrend. More importantly, sales of existing and new homes faltered notably with existing home sales confirming a deceleration trend. With stocks and data warning, I am warily noting how the current heights of sentiment align with the peak of sentiment before the housing market topped during the last cycle.

This is the point where I should start planning my exit from profitable seasonal trades on home builders. Instead, most of the trades have effectively failed this time around. So I have gone from an excited expectation to a somber realization. I thought the sell-off in home builders presented me with the buying opportunity I did not think would happen this year. Now I am increasingly accepting the possibility that home builders have topped out for the year. Whether this top is THE top for the cycle depends greatly on the macro environment. If economic growth continues to print strong numbers, I think home builders will look a lot less risky. If economic growth falters, homebuilder stocks will surely be considered an immediate and on-going source of funds.

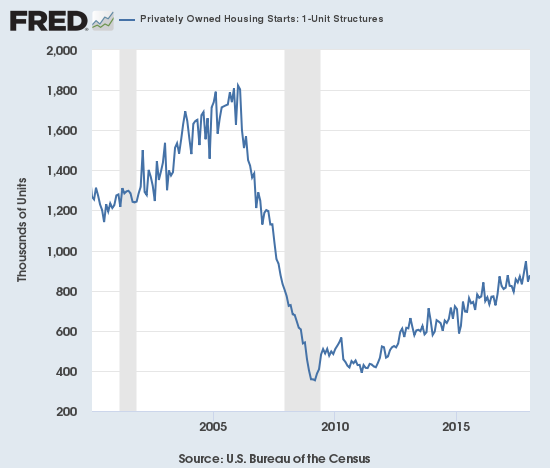

New Residential Construction (Housing Starts) – January 2018

Single-family housing starts for December were revised upward from 836,000 to 846,000. January starts increased month-over-month by 3.7% to 877,000. On an annual basis, single-family housing starts increased a healthy 7.7%, representing a marked improvement from December’s 3.5% year-over-year gain.

January, 2018 housing starts stayed close to the uptrend.

Source: US. Bureau of the Census, Privately Owned Housing Starts: 1-Unit Structures [HOUST1F], retrieved from FRED, Federal Reserve Bank of St. Louis, February 22, 2018.

Over the last five months, regional year-over-year changes in starts have exhibited wide dispersion. The Northeast, Midwest, South, and West each changed 11.9%, -12.4%, 2.0%, and 38.0% year-over-year respectively in January. The West delivered very strong growth yet again as builders are clearly in a rush to serve a thirsting market. I believe this is by far the largest year-over-year gain in housing starts for the West in a very long time.

Existing Home Sales – January, 2018

The existing home sales numbers for January, 2018 had a tough comparison given a year ago sales hit a post-recession high (slightly surpassed in 2017 by March and December sales). Moreover, the month-over-month decline in December closed out the year on a downer and put pressure on the January number to nullify some of the negativity. January failed to deliver relief on the message.

The routine description for existing sales is usually sales decline because of a shortage of inventory and sales increase in spite of inventory shortages. For November, the NAR delivered a twist by distinguishing between the upper-end and the rest of the market to help explain how sales can surge despite the parallel relentless increase in prices. The NAR closed out the year observing that sales could have been better if prices were not so high and inventory more available. To describe the dynamics behind January’s sales decline, the NAR referenced both the lack of inventory and the affordability problem caused by the scarcity.

Related Posts

SP 500 And NDX Futures Daily Charts – Economic Malaise – FOMC And Quad Witch

SP 500 And NDX Futures Daily Charts – Economic Malaise – FOMC And Quad Witch Hot And Cold Sectors In 2014: Looking Back

Hot And Cold Sectors In 2014: Looking Back Japan to reportedly take action to scrutinize crypto globally

Japan to reportedly take action to scrutinize crypto globally- Video: Boeing Bucks The Multinational Trend Ond Overcomes The Strong Dollar

E

The Daily Shot And Data – February 4, 2016

E

The Daily Shot And Data – February 4, 2016 Mandarin Monday – China’s $200Bn Manipulation Not Enough – Now What?

Mandarin Monday – China’s $200Bn Manipulation Not Enough – Now What?

Leave A Comment