What is the Cash Conversion Cycle?

The main way a company can make more profit is to simply sell more stuff. But how do you sell more stuff?

Cash.

More cash availability equals more products you can make and sell.

Wall Street loves earnings and many people believe earnings drives cash and profitability, but this is incorrect. Cash drives earnings. The faster the cycle of cash, the quicker it can be reinvested to generate earnings.

Regardless of what the media says, cash is and always will be king. No business can start or grow without cash. That’s why growth and start-up companies are constantly looking to raise cash.

By looking at the cash conversion cycle and analyzing the CCC formula, a company that can shorten the cash conversion cycle is going to be ahead of its competitors.

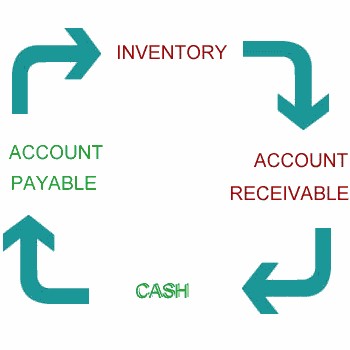

The basic theory of the cash conversion cycle is this:

The Cash Conversion Cycle

The entire cash conversion cycle is a measure of operating efficiency and management effectiveness. The lower the number, the quicker the cycle. The quicker the cash conversions cycle, the better the management is at operating the business.

In this way, you can use the cash conversion cycle formula to compare efficiency and management on apples to apple basis. In other words, do not use the Cash Conversion Cycle to compare companies from different industries or different business models.

How to Calculate the Cash Conversion Cycle Formula

The CCC ratio is made up of 3 components.

The final formula you’ll be using is

Cash Conversion Cycle =

Days Inventory Outstanding

+ Days Sales Outstanding

– Days Payables Outstanding

There is a common misunderstanding that the Cash Conversion Cycle comes from the balance sheet. The CCC equation requires both the income statement and the balance sheet. As the cycle involves the selling of inventory, this is entered into the financials as revenue.

Let’s break down each component and you’ll see how it all works.

Days Inventory Outstanding

Days Inventory Outstanding shows you in days, how long it takes for inventory to be sold. The quicker inventory is sold, the better.

DIO = (Inventory/COGS) x 365

This is an annual calculation. To calculate between two periods, use the below formula.

Related Posts

Half of assessed jurisdictions don’t have ‘adequate laws and regulatory structures’ — FATF

Half of assessed jurisdictions don’t have ‘adequate laws and regulatory structures’ — FATF Key Support Levels For The Markets To Watch After This Bounce

Key Support Levels For The Markets To Watch After This Bounce The Performance Of Impact Investments

The Performance Of Impact Investments The Expected US Economic Growth Rate Is Back Down To The 2% Level

The Expected US Economic Growth Rate Is Back Down To The 2% Level- If You Don’t Learn…

Personal Income, Consumer Spending Rise Less Than Expected; PCE Price Index Negative; 4th Quarter Acceleration Coming Up?

Personal Income, Consumer Spending Rise Less Than Expected; PCE Price Index Negative; 4th Quarter Acceleration Coming Up?

Leave A Comment