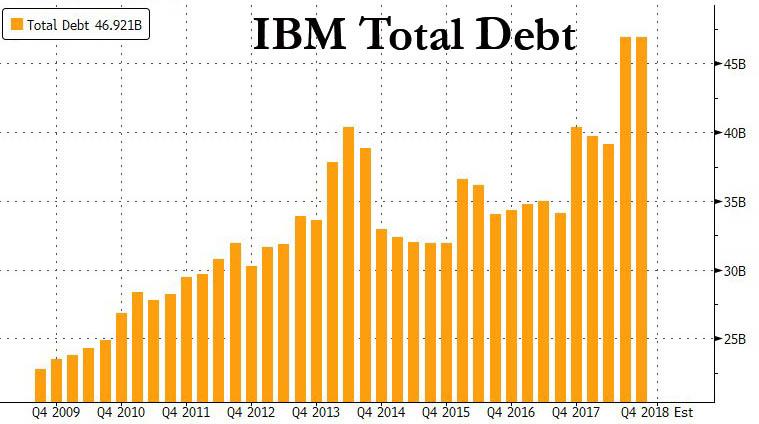

While IBM’s stock is bouncing back modestly from an ugly open, bond market participants remain gravely concerned at what damage the Red Hat acquisition could do to IBM’s balance sheet.

The transaction will take IBM’s debt load close to $80 billion as it takes on the second-largest technology deal of all time, according to Bloomberg Intelligence analysts Robert Schiffman and Mike Campellone.

the Red Hat acquisition and as a result, IBM’s already shaky A+/A1 rating could soon be downgraded to BBB.

For now, the stock seems to be shrugging it off…

But the bond market most definitely is not…

As Bloomberg notes, IBM wants to eschew the route taken by many companies which sacrificed strong credit ratings to pursue large-scale mergers and acquisitions that left them with lower, triple B rankings, according to S&P analyst David Tsui.

“The ratings are very important to them — their competitors in IT services are all rated A or higher”, Tsui said. Debt issuance will be “substantial” but with more than $6 billion in projected free cash flow, the company won’t have to go as close to funding the whole deal with debt, according to Tsui.

Short-dated bond yields have burst above 4%…

And more notably with regard the investment-grade credit rating, IBM bond risk is now dramatically higher than its peers in the IG Technology sector…

A spokesman for IBM pointed to the firm’s strong free cash flow and that the deal is accretive from the first year. He acknowledged the ratings agency moves adding that IBM remains in “solid investment grade territory.”

Bloomberg Intelligence analysts said in a report Monday that IBM may issue at least $20 billion of debt to fund the acquisition:

Related Posts

Some Economics Of Place-Based Policies

Some Economics Of Place-Based Policies UK advertising watchdog flags crypto ads ‘red alert’ priority

UK advertising watchdog flags crypto ads ‘red alert’ priority- Gold Takes Flight After Fed Fuels Rate Cut Hopes At Latest Meeting

Unlocking ASX Trading Success: V300AEQ ETF Units – Wednesday, July 17

Unlocking ASX Trading Success: V300AEQ ETF Units – Wednesday, July 17- Oil Prices Surge 5% As Non OPEC Countries Cut Production, FOMC Ahead

The “Big Bond Short” Illusion

The “Big Bond Short” Illusion

Leave A Comment