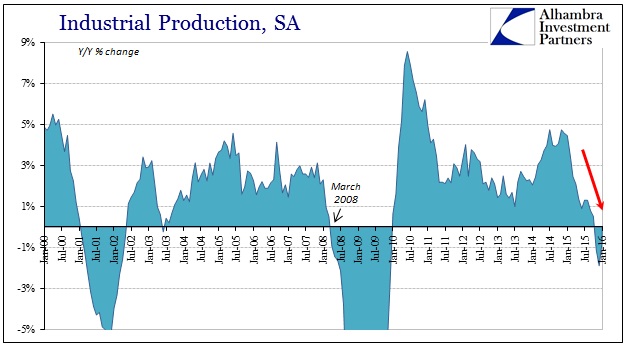

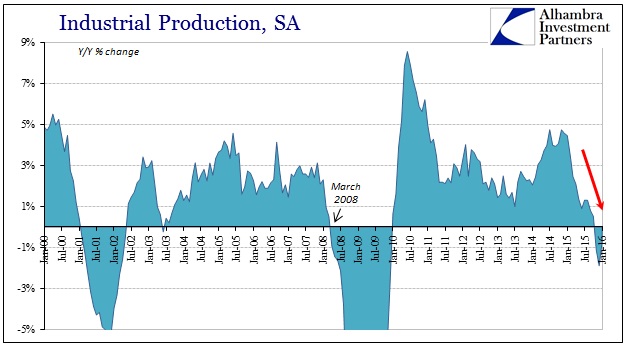

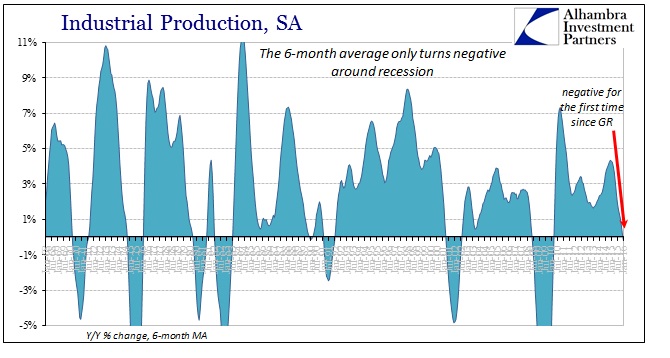

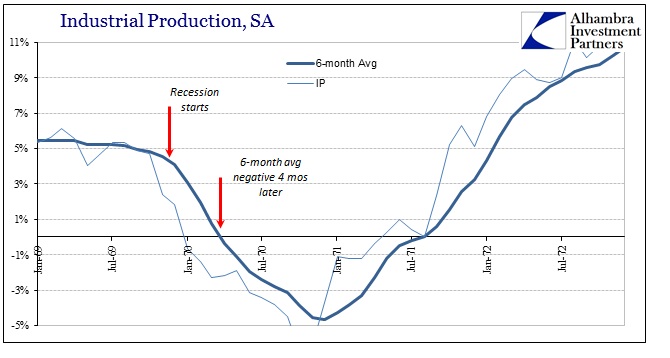

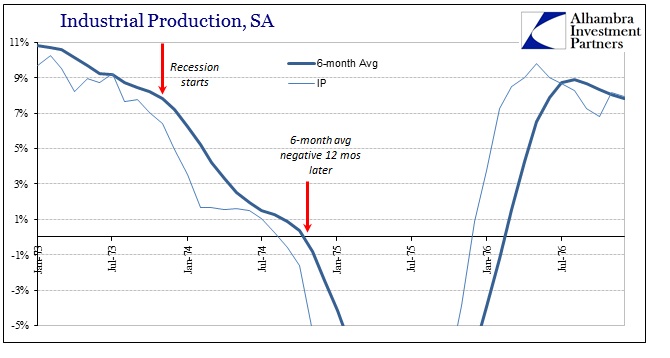

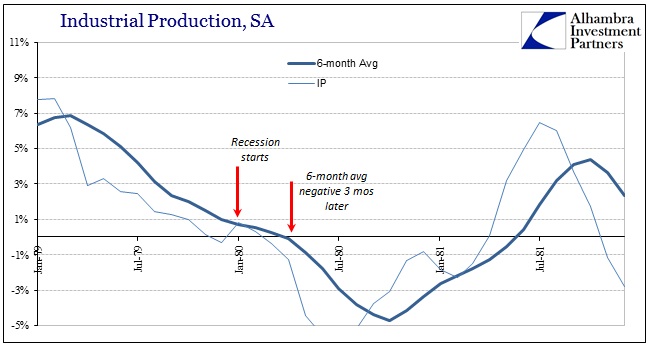

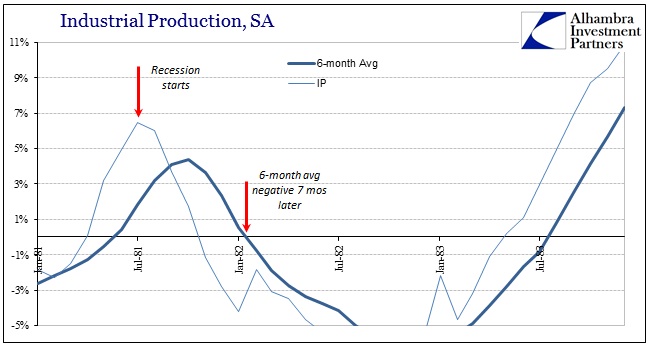

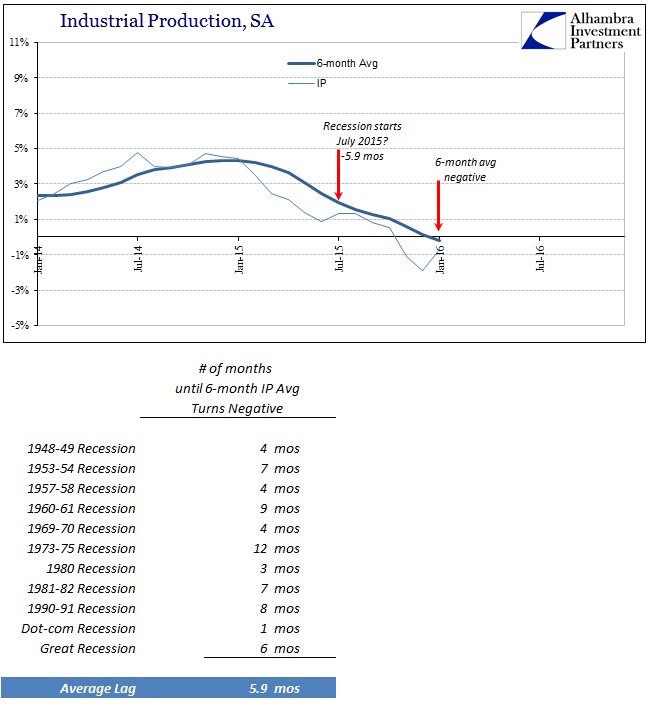

Industrial production fell 0.7% in January 2016 which was slightly better than the (revised) -1.9% estimated for December. It was, however, the third consecutive month showing a decline and, more importantly, the 6-month average turned negative for the first time in the “cycle.” Industrial production, at least as far as the Federal Reserve’s estimated series for it, is actually a lagging indication particularly in the average. In other words, in every other cycle by the time the 6-month average falls below zero the recession is already several months old.

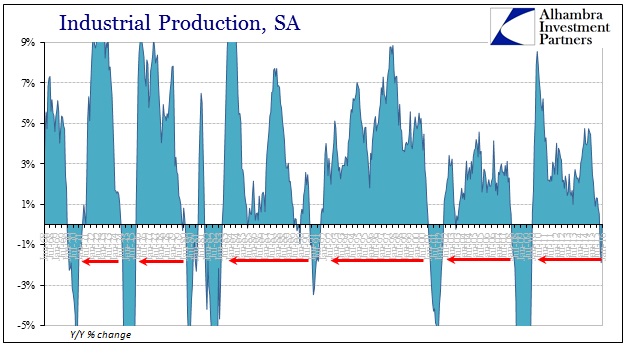

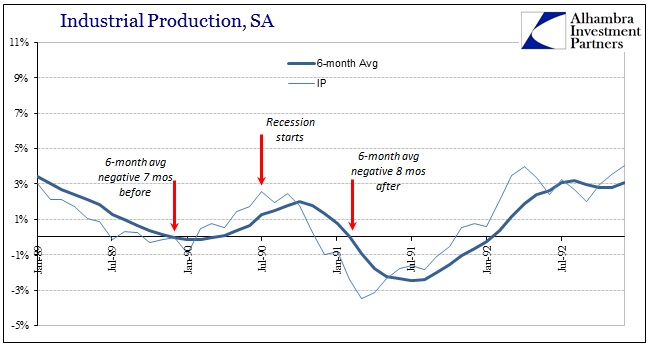

The consistency with which we find that to be the case is very significant. In every recession since World War II, we find contracting IP shortly after each official cycle peak (declared by the NBER). The one exception is the 1990-91 recession where industrial production briefly dropped to slightly negative several months prior to the start of that recession, only to rebound somewhat into its early stages and before again falling further below zero in accordance with this overall long-term pattern.

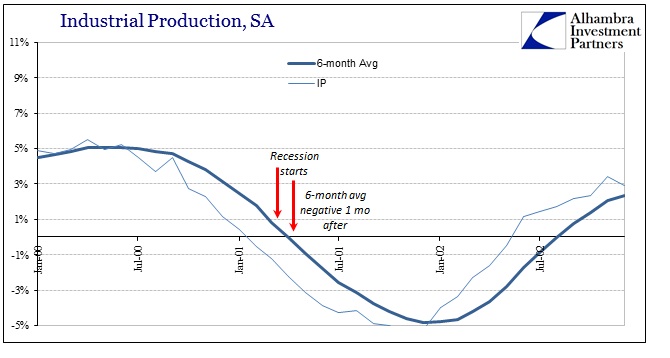

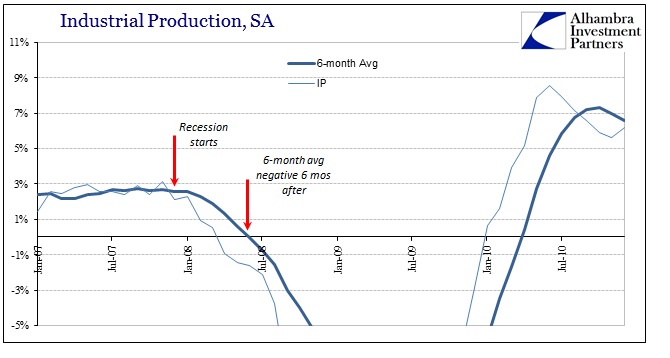

What that repeated pattern suggests is the slowing across industry (second derivative) is the relevant part of the initial recession impulse and not necessarily the actual contraction; that part becomes relevant later toward the trough in determining its severity, or reacting to it in other fashions. Again, this has been remarkably consistent in each post-war recession including the last two officially declared in this century. That would strongly suggest recessionary factors build elsewhere before impacting into contraction in this broad classification for US industry. From that view, we can surmise that when the 6-month average for IP does turn negative it does so as the US economy has already undergone strong recessionary pressure and taken already significant dislocation.

I have shown above only the seven recession events since 1969-70, but I calculated the average lag using all of the post-war contractions. The average time between official recession start and a negative read for the IP 6-month average is just less than 6 months. Again, the uniformity and consistency is what is significant, even taking into account the prior anomaly in 1990. Using this one data point it would suggest that a recession may have begun sometime around July 2015 – which would be perfectly consistent with a whole host of other economic accounts (though, conspicuously not employment estimates), if not certainly market-driven turmoil in across a great many markets (now including stocks).

Related Posts

Equities Search For A Catalyst: Trading What Is In Front Of You

Equities Search For A Catalyst: Trading What Is In Front Of You The Stock Whisper Of The Day: FIT, SPY, SDRL, USO

The Stock Whisper Of The Day: FIT, SPY, SDRL, USO Stellus Capital: 10% Monthly Dividend Is Sustainable… For Now

Stellus Capital: 10% Monthly Dividend Is Sustainable… For Now The Outlook For S&P 500 Dividends Near The End Of 2024

The Outlook For S&P 500 Dividends Near The End Of 2024- BNY Mellon’s Q1 Earnings & Revenues Meet Expectations

- E

Surviving Hillary – Surviving Donald: The Election Portfolio

Leave A Comment