Think of “market internals” as the blood pressure and insulin levels of the financial world. They operate below the surface, frequently unnoticed, but over time they have a big say in the health of the patient.

And right now they’re pointing to a heart attack.

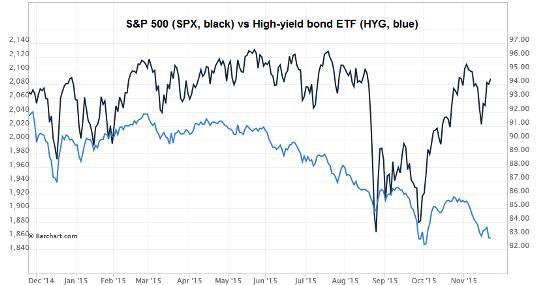

Let’s start with junk bonds. These are loans to financially and/or operationally-weak companies that because of their weakness have to pay up to borrow. Such bonds have a risk/return profile that’s more akin to equities than to, say Treasury bonds, and they trade accordingly, rising and falling on the likelihood of default rather than their relative yield.

Recession means higher default rates for weak borrowers, so when the economy is slowing down or otherwise hitting a rough patch, the junk bond market is often where it registers first. Lately, junk has been tanking relative to stocks (chart created by Hussman Funds):

Another widely-followed internal is the relationship between large-cap (i.e., relatively safe) stocks and riskier small caps. When large caps outperform small caps, it’s frequently a sign that the broader economy is weakening. Since September, that’s been happening too:

In general, when market leadership gets extremely narrow — that is, when only a few things are going up and everything else is either flat or falling — trouble ensues. During the late 1990s tech stock mania, for instance, the global economy ended up being supported by the US, whose economy was supported mostly by the NASDAQ, which was supported by just a handful of high-flying tech stocks. When those stocks finally cracked, they took the whole world down with them.

Now something similar is happening, thanks in large part to this cycle’s dominant tech firms, especially Apple. From CNBC:

The days of Apple’s amazing profits may be over

The S&P 500’s profit margin growth over the past five years has been driven largely by tech, and one name in particular: Apple (AAPL). Unfortunately for the market and for Apple, the days of exceptional expansion may be over.

That’s according to David Kostin of Goldman Sachs, who wrote in a note Monday to clients that he expects margins to remain flat at 9.1 percent for 2016 and 2017.

“Many of the drivers of margin expansion during the past few decades appear to be behind us,” Kostin wrote, listing former catalysts such as lower interest rates, lower taxes, a switch from manufacturing to services and technological innovations.

Since 2009, information technology has been responsible for about 48 percent of overall S&P 500 margin expansion. Apple alone has been responsible for 18 percent. [But that is about to change.] According to BK Asset Management’s Boris Schlossberg, Apple’s “lack of gusto” when it comes to profit margins is a result of unsatisfactory products, aside from the new iPhone.

“At this point, the watch is a bust, TV is a bust, the big iPad is not really flying off the shelves,” Schlossberg said Tuesday on CNBC’s “Trading Nation.” “I don’t see any other place where they’re going to be able to get the kind of margin expansion that they’ve been able to get for the last five years.”

And while Apple is up 7 percent for the year, Schlossberg said investors may be losing enthusiasm for the stock as well, at least compared with other tech outperformers this year.

Leave A Comment