Starting in the 4Q16, survey data released by Markit saw a pronounced improvement in sentiment. This was accompanied by the UK’s surprising post-Brexit growth, Canada’s continued exit from its shallow recession, stronger 4Q16 Chinese numbers and nuanced but noticeable improvement in numbers from Japan. The IMF acknowledges these improving numbers in their latest global economic forecasts.

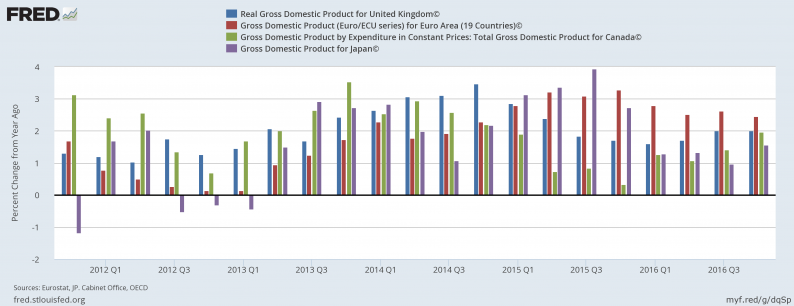

At the highest level, Y/Y GDP for some of the largest economic regions has been moderate but consistent:

Since the 2Q13, Y/Y GDP growth for UK, EU, Canada and Japan has been consistently positive (although perhaps aggravatingly slow). The IMF report made the following observation about growth data:

Economic activity gained some momentum in the second half of 2016, especially in advanced economies. Growth picked up in the United States as firms grew more confident about future demand, and inventories started contributing positively to growth (after five quarters of drag). Growth also remained solid in the United Kingdom, where spending proved resilient in the aftermath of the June 2016 referendum in favor of leaving the European Union (Brexit). Activity surprised on the upside in Japan thanks to strong net exports, as well as in euro area countries, such as Germany and Spain, as a result of strong domestic demand.

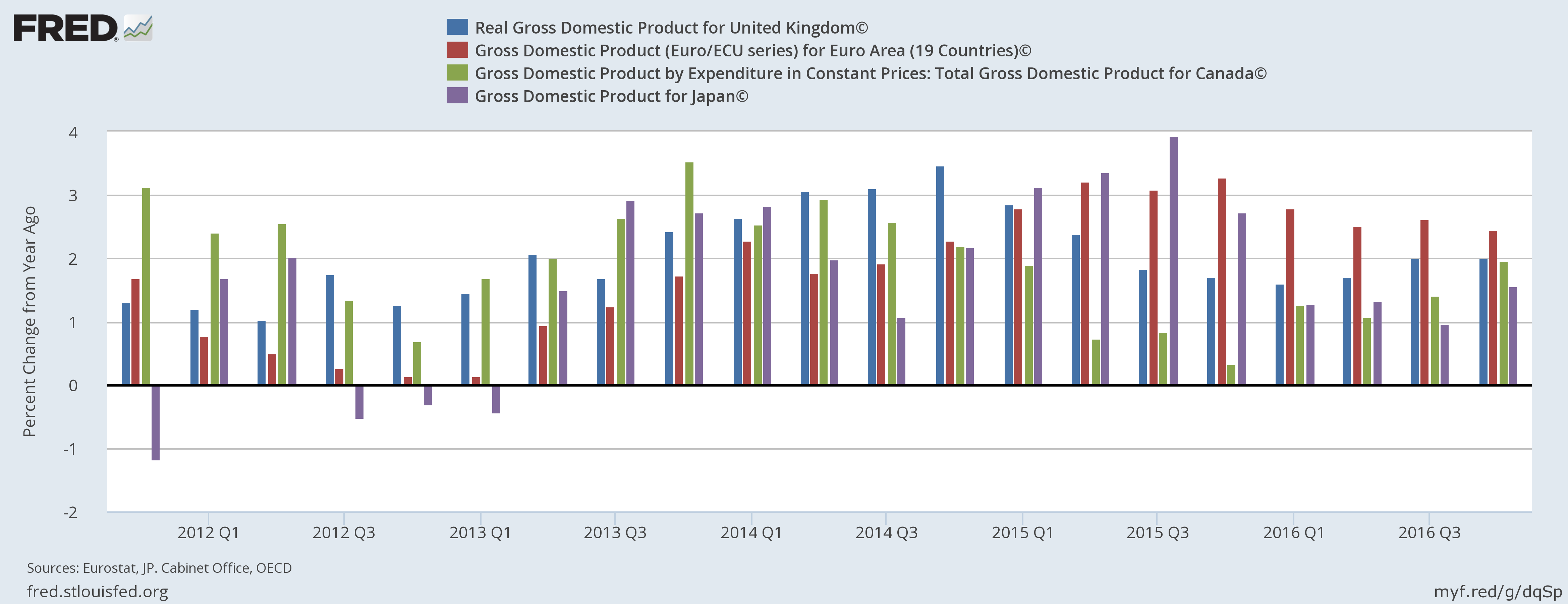

The IMF noted two other important fundamental improvements. First is an increase in consumer durables and capital goods production:

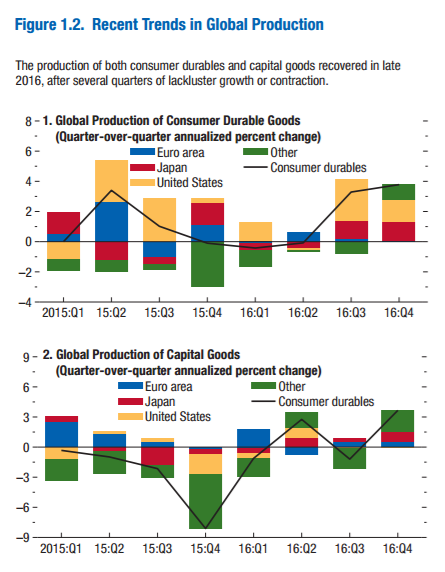

Consumer durables production (top chart) declined in the 4Q15 and 1H16 but has since rebounded and is now growing near 4%. Capital goods production contracted in 1Q15, largely due to the oil price collapse. But in increased in 2 of the last 3 quarters. Second, is a pick-up in trade and investment:

Imports contracted in the 1Q16, but rebounded (top chart). The bottom chart shows the positive correlation between imports and capital investments.

Related Posts

Price analysis 11/8: BTC, ETH, BNB, ADA, SOL, XRP, DOT, SHIB, DOGE, AVAX

Price analysis 11/8: BTC, ETH, BNB, ADA, SOL, XRP, DOT, SHIB, DOGE, AVAX Illinois Tool Works: A Dividend King With Double-Digit Total Return Potential

Illinois Tool Works: A Dividend King With Double-Digit Total Return Potential- Cardinal Health (CAH) Q3 Earnings Beat Estimates, Rise Y/Y

- Stock Charts Today – Friday, May 4

WTI Up Slightly As Divisions In OPEC Emerge

WTI Up Slightly As Divisions In OPEC Emerge GBP/USD Forex Signal: Bullish Ahead Of US Retail Sales Data

GBP/USD Forex Signal: Bullish Ahead Of US Retail Sales Data

Leave A Comment