“Davidson” submits:

You can’t forecast what you cannot see…or can you? People are more predictable than things.

Investing is a process which must look through a fog of unknown using past experience. Many use mathematical trend analysis to forecast the future and provide forecasts with date and penny precision. But, how does one forecast inventions such as the iPhone, the Internet, a cure for Hepatitis C or preventative for HIV which force forecasters to revise all their previous assumptions of earlier forecasts. How does one forecast the future of markets if one never anticipated such evolutionary discoveries? The answer lays in not trying to predict the details of the ‘next great discovery’ but resides in understanding how individuals and society thinks and behaves.

One begins by identifying how value is created over time. Once one delves into the process of value creation, it forces one to conclude that value occurs when producers successfully meet the needs of society’s relentless desire to improve its standard of living. Those companies which do this repeatedly over time produce price histories like Danaher (DHR).

There is nothing magical about DHR’s product line which has made roughly 1,000 acquisitions of small industrial product companies over its history. Recently, DHR spun out Fortive (FTV) which represented about 40% of its businesses into a separately traded company. The products these companies produce have serious competition, yet DHR and FTV compete more effectively than any of their peers. This fact forces one to delve more deeply to understand how the people, the management, the CEO, operates these companies so successfully for such an extended period. The answer lies in the corporate culture instilled since 1985 under Steve and Mitch Rales and the development of the Danaher Business System under Art Byrne. Art wrote book about his approach in 2012, “The Lean Turnaround: How Business Leaders Use Lean Principles to Create Value” by Art Byrne and James P. Womack. Charles Koch wrote how he developed his equally strong record of performance at Koch Industries in “Good Profit”, 2015. Great financial performance comes from continuous improvement by engaging employees as partners in the business. This requires a management mind-set which is very different from established concepts of CEOs as leaders. CEOs must become good listeners and a focal point for implementing the best ideas employees bring to their work everyday. The long-term performance of this approach is impossible to ignore. Koch Inds owns Georgia Pacific, the maker of Angel Soft toilet paper and Brawny paper towels on which they make a great profit providing everyday products at low cost to consumers. It is a recipe for improving individual and family standard of living that they follow, Faster! Better! Cheaper! and profitable. While one cannot predict the next great discovery, one can identify CEOs and corporate managements which understand how to focus on meeting their customers needs. Every time a company is able to incorporate this into the corporate culture, the process devolves to every employee, results in considerable employee engagement and strong long-term corporate performance.

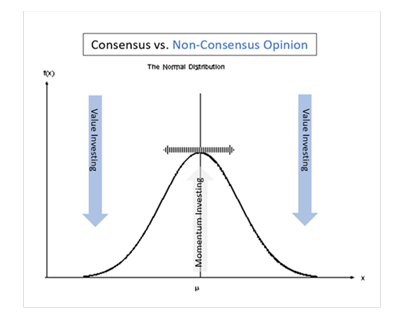

The investing process, once one identifies companies similar to DHR and FTV, becomes one of identifying the economic factors which are likely to produce conditions which lets these managements produce surprise profits. While economic conditions never repeat due to continuous change in society, change in government policies and unanticipated human invention, one can monitor when investors overly favor one area vs. others. Investors(Momentum Investors) have always tended to crowd into the most media-popular area of markets. In today’s market, the over-crowded issues have been identified as the F.A.N.G issues (Facebook, Amazon, Netflix, Google) and Tesla(TSLA). They are media’s daily favorites. For investors who use economic and business return metrics(Value Investors), the better investments lay well outside the focus of market favorites. The typical Gaussian plot helps to explain the concept of Consensus vs. Non-Consensus investing.

Value Investors seek to identify the conditions which will favor a shift of Momentum Investors into the ignored sections of the market. Once conditions appear to offer an opportunity, this involves low prices relative to long-term expectations, Value Investors add capital to companies like DHR and FTV because their managements have become predictable as to the general improvements in profits which are likely to occur with changing economic trends. Value Investors do not predict EPS or market prices with precision. They understand that economics are imprecise and management responses will vary based on unpredictable events. What can be predicted in general is whether Earnings/Shr(EPS) are likely to surprise higher or lower. One can not ever predict the market response other than higher or lower. Investing never allows precision. It only permits fairly good guesses and if one is roughly correct, one can only develop bands of confidence for EPS and the market’s impact on prices.

We just received a favorable response to Fastenal (FAST) and WW Grainger (GWW). Recent reports revealed that both companies had exited the industrial recession caused by a period(2014-2016) of strength in the US$. These companies, like DHR and FTV, do not have a proprietary product base being distributors of fasteners and industrial supplies comprising millions of SKUs. FAST and GWW are ordinary businesses which are simply operated very well. What is predictable for these companies is not the detail of which products will sell. What is predictable is that the history of corporate managements servicing their respective customers very well is likely to be repeated with earnings surprises once conditions permit.

This week just saw a market refocus to GWW which rose more than $20shr to $202shr on the Oct. 17, 2017 earnings release. Value Investors had already witnessed 3-quarters of improving results for both companies and sharp rises in the Chemical Activity Barometer and Job Opening data as the US exited the industrial recession. For Momentum Investors, Oct. 17th was as if a switch was flipped on.

FAST and GWW remain recommendations as they have been since April 2016. It is my guess that as the industrial recovery progresses, investors are likely to re-favor both issues to price levels consistent with previous trends. For FAST this means a price over $100shr and for GWW the level is over $400shr. Market psychology will determine price levels the next 2yrs-3yrs. The best one can do is identify economic trends and the corporate managements with which to participate. The rest is left to changes in market psychology. FAST and GWW remain, at the moment, solidly in the Non-Consensus of market psychology.

The best lesson to learn about investing is that investing is about understanding people, how people create investable performance and how markets price that performance. Value Investors buy when the opportunities are favorable for positive changes and sell when they are unfavorable. We are not investing in things. Value Investors invest in people’s behavior which creates value. Behavior is not a thing and for many remains an elusive criteria for investment.

Behavior once well-defined is more predictable than the ‘next best thing’!

Leave A Comment