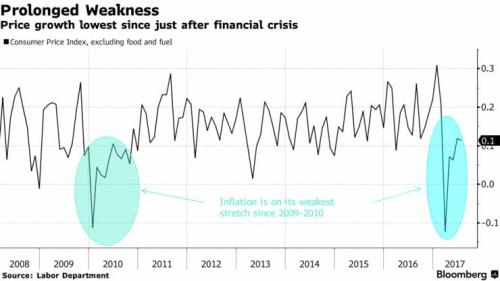

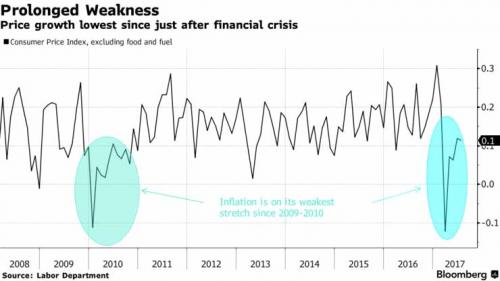

It’s been a bad year for inflation forecasters: every month this year, economist consensus has expected core CPI to rise by 0.2% and every month since March, that figure has proven to be too high, resulting in 5 consecutive inflation misses and the weakest stretch of core inflation growth since 2010.

Tomorrow’s CPI print, however, should finally break the spell: following a stabilization in cell phone plan costs, a rebound in hotel prices, and the ongoing weakness in dollar, should make tomorrow’s 0.2% core CPI forecast easier to achieve. And while year-over-year core growth is expected to slow to just 1.6% , the weakest since January 2015, Fed officials – having telegraphed a December rate hike – have indicated they’re looking more closely at the month-to-month trends for hints on what inflation will do next.

“Inflation matters for the December decision, which is still very much up in the air,’’ Jonathan Wright, an economics professor at Johns Hopkins University and former Fed economist told Bloomberg. If core price gains remain low through the end of the year, “it would be too hard to insist that inflation is still on track.’’

Headline inflation is also expected to come in a tad stronger: 0.3% M/M the highest since January, and 1.8% year-over-year due largely to a jump in gasoline prices following hurricane Harvey. “The core inflation numbers are going to be some of the lesser-affected of the key data between now and December,” said Stephen Stanley of Amherst Pierpont.

And yet, while countless algos will react within nanoseconds of tomorrow’s CPI print, with a laser focus on whether tomorrow’s US core CPI will come out at 0.1%, 0.2% or 0.3%, it is easy to lose sight of the bigger inflation story. Simply put, inflation has been trending down across the major economies for decades. Take the US, each decade has seen inflation average as follows:

Leave A Comment