Should investors use bond yields as a baseline to determine if stocks are over-or-under valued?

If you believe in the “Fed Model,” your answer is “yes”. The model instructs investors to compare the S&P 500’s earnings yield (Earnings/Price, the inverse of the P/E ratio) to the 10-Year Treasury yield:

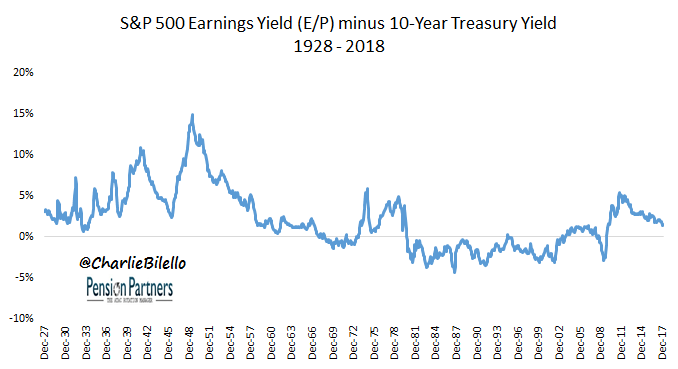

With the Earnings Yield (“EY”) today currently above the 10-Year Treasury Yield (“TY”), many pundits are arguing that stocks are still undervalued (and therefore attractive), despite other metrics indicating otherwise (click here for a recent post on this). Are these pundits correct? Is comparing the Earnings Yield to Treasury Yields an effective way to value stocks and forecast future equity returns? Let’s take a look…

Data Sources for all charts/tables herein: Robert Shiller, Bloomberg, YCharts.

Going back to 1928, we can separate EY minus TY into deciles, from lowest (-4.4% to -2.1%) to highest (7.0% to 14.9%). We can then calculate average and median forward returns over the next 1 to 10 years within each decile…

If you’re struggling to find a strong relationship in the above tables, that’s because there isn’t one. While the highest EY-TY decile is indeed followed by the strongest returns, the lowest EY-TY decile has above-average returns from 4 years through 10 years forward. The weakest returns reside in the middle deciles (4-7), with a slight bias to higher forward returns with higher EY-TY starting levels.

We can observe this bias in the upward slope of the trendline line in the scatter chart below, which compares the starting EY-TY levels to forward 10-Year Total Returns. The R Squared, in this case, is .11, meaning that knowledge of EY-TY accounts for only 11% of the variation in future 10-year returns.

Related Posts

Despite Higher GDP, U.S. Economic Data Continues To Disappoint

Despite Higher GDP, U.S. Economic Data Continues To Disappoint How to make money selling items found in storage units?

How to make money selling items found in storage units?- Oil Prices Struggle As Traders Eye OPEC Meeting

- Most Valuable: The Currency Of Our Debt And Expenses

- FTSE 100 Volatility May Pick Up As Durable Goods Orders Are On Deck

February Pending Home Sales Surge By Most On Record Amid Midwest Miracle

February Pending Home Sales Surge By Most On Record Amid Midwest Miracle

Leave A Comment