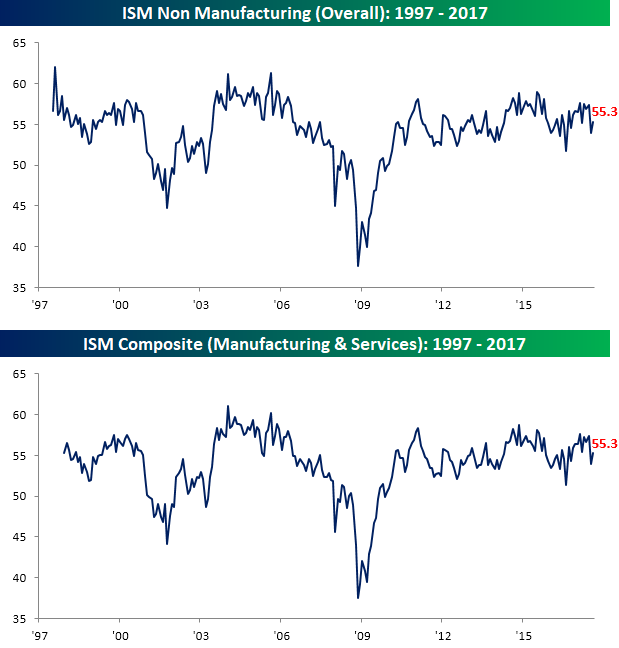

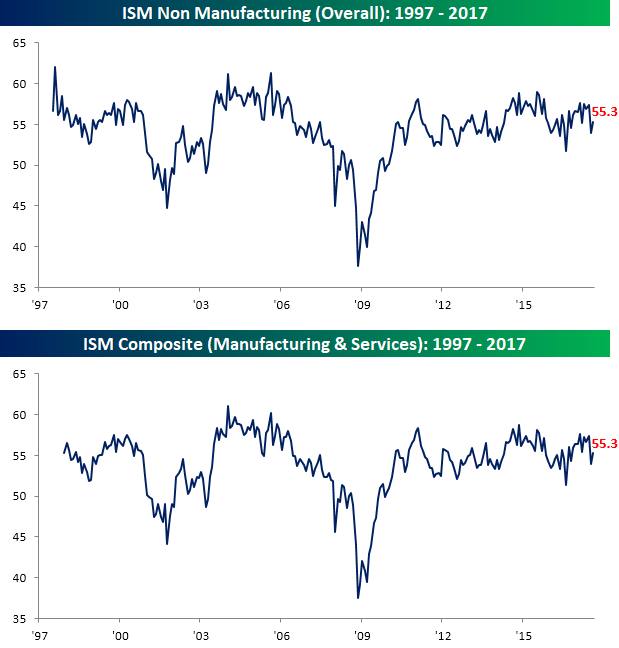

After last week’s ISM Manufacturing report came in at a six-plus year high, the current environment for the larger services sector was not nearly as strong. While Wednesday’s release of the ISM Non-Manufacturing report for the month of August did improve to 55.3 relative to July’s reading of 53.9, the rebound was not as strong as expected (55.6). Even with the disappointment, though, a reading of 55.3 is still solid. On a combined basis and accounting for each sector’s share of the overall economy, the August combined ISM also came in at 55.3 (second chart).

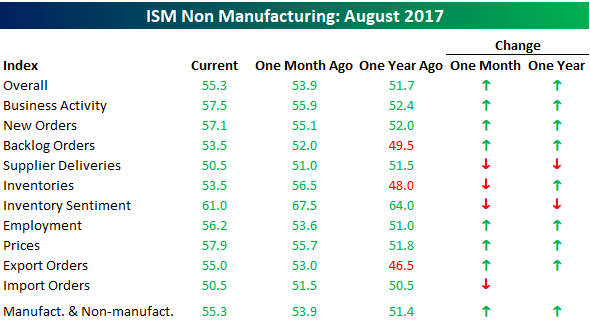

Looking at the internals of this month’s report shows a mixed picture. Of the ten components, six increased on a m/m basis and eight rose relative to their levels from last year. The largest increases this month were in Employment and Prices, while the largest declines were in Inventory Sentiment and Inventories.

Leave A Comment