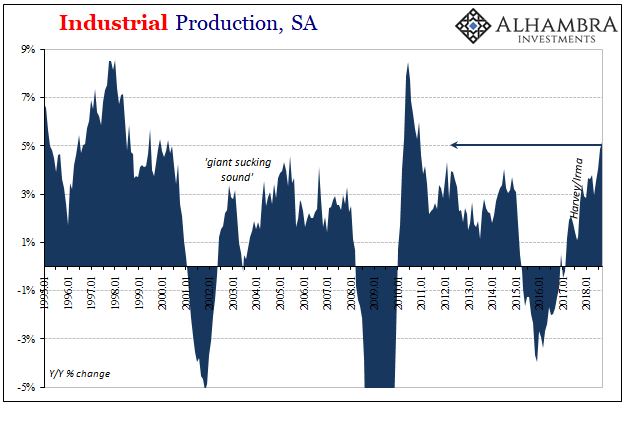

The calendar last month hadn’t yet run out on US Industrial Production as it had for US Retail Sales. The hurricane interruption of 2017 for industry unlike consumer spending extended into last September. Therefore, the base comparison for 2018 is against that artificial low. As such, US IP rose by 5.1% year-over-year last month. That’s the largest gain since 2010.

While that may be, over the last five months American industry has slowed precipitously from its prior pace. It doesn’t show up because the annual rate of change is so heavily frontloaded by the aftermath of Harvey and Irma. Include within that the bringing forward of industrial (largely manufacturing) activity in anticipation of global trade restrictions, it created a period (8 months) where in isolation it looked like economic acceleration – to those who really wanted it to be.

In terms of Industrial Production, from October 2017 to April 2018 (inclusive) the total increase was 4.3%. By itself, that was more than in any month since 2010 at annualized rates. Annualizing those 8 months, it was as if US IP was growing at better than 6.5% which would have been something like the immediate aftermath of the Great “Recession.”

Over the last five months, however, IP has slowed considerably, rising by about three-quarters of a percent. That’s just 1.8% annualized, meaning growth more like the 2012 slowdown than the 2010 recovery(ish) trend.

If this slowing continues throughout October, IP will have gained only 3.7% next month (down sharply from this month on base effects) since it will be compared to October 2017 and that month’s big jump kickstarting the storm cleanup effort.

All these annuals include acceleration in the mining sector, specifically crude oil. Crude production has slowed in the last two months, too, but that’s from an already blistering pace. If the reduction in growth this summer is indicative of anything more than temporary factors, US industry will lose the only segment that is consistent with rhetoric about this “strong” economy.

Related Posts

E

Twitter Delaying Its Death

E

Twitter Delaying Its Death- Toyota, Suzuki To Explore Possibility Of Business Partnership

Expensive Dollars And The Return Of Negative Hedged Yields

Expensive Dollars And The Return Of Negative Hedged Yields Stocks And Precious Metals Charts – Midterm Elections Tomorrow – FOMC Jawboning On Wednesday

Stocks And Precious Metals Charts – Midterm Elections Tomorrow – FOMC Jawboning On Wednesday My Leitner-Esque Moment

My Leitner-Esque Moment Here’s What To Watch In Crude Oil Right Now

Here’s What To Watch In Crude Oil Right Now

Leave A Comment