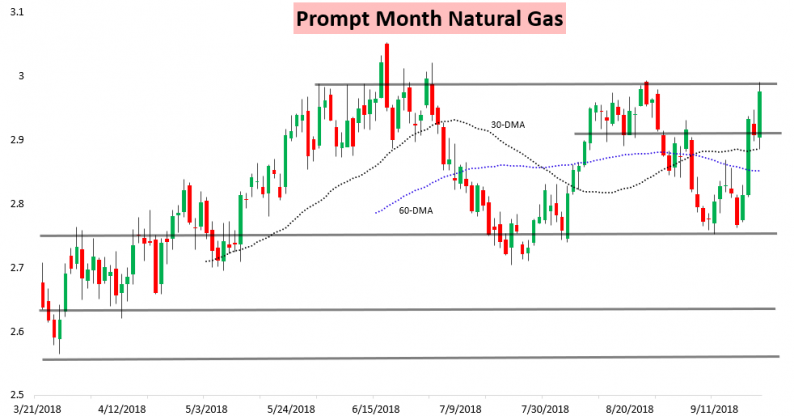

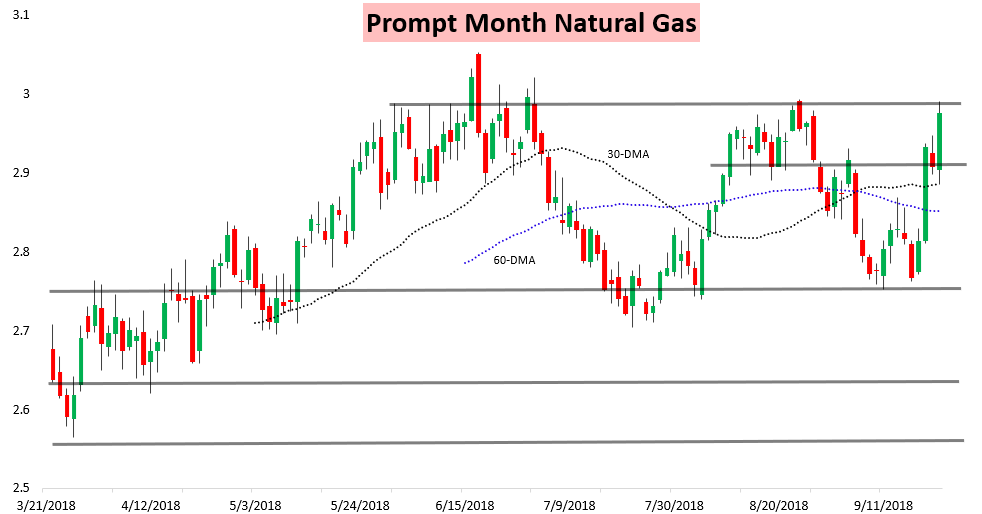

The October natural gas contract rallied a bit over 2% again today, selling off initially on a slightly larger than expected storage injection announced by the EIA but very rapidly reversing high and rallying through the middle portion of the day.

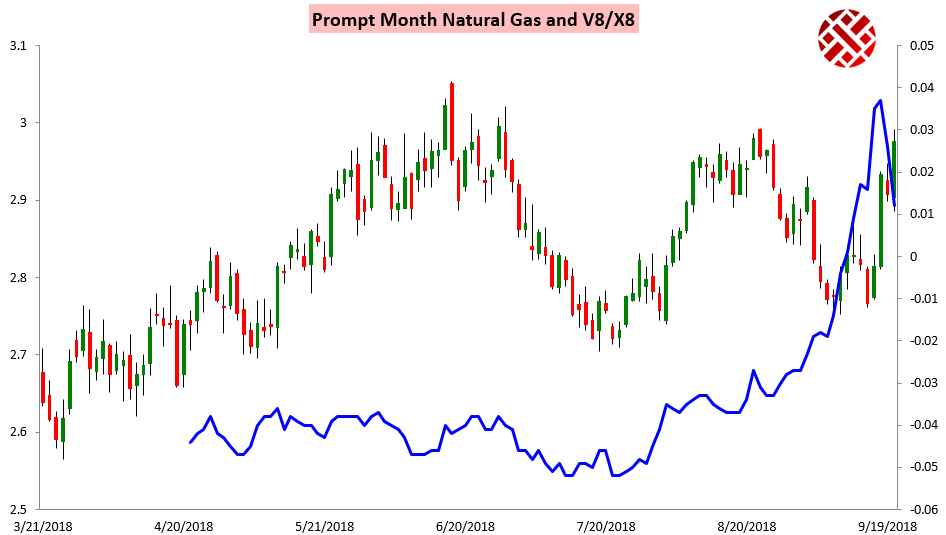

The November contract again helped lead the way higher, leading to another move lower in the X/V October/November contract spread.

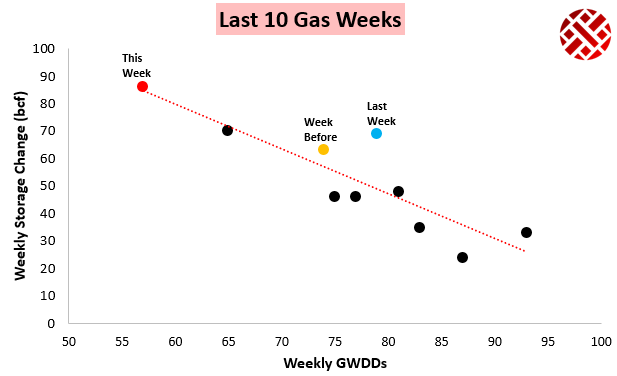

This came even though the EIA announced that 86 bcf of natural gas was injected into storage, beating a market consensus that was right around the 81-83 bcf level. Our estimate of 83 bcf was not far off, but still a touch too low.

This fits in well with the average print of the past 10 weeks after we have seen some loosening recently, as the print was tighter than last week on a weather-adjusted basis. Immediately after its release in our EIA Rapid Release for clients, we emphasized that, “we see room towards $2.95 on this tightening short-term,” which verified within an hour.

Our intraday Note of the Day built on this to highlight the risk for, “…a brief move towards $2.98…” which also verified as prices continued rallying through the day on a supportive strip (and the rally was indeed brief, with selling back into $2.96 from there). The rally was aided by some colder risks in the longer-range on model guidance as well, with Climate Prediction Center forecasts still showing long-range cold risks.

Related Posts

Gold Primed For A Push Higher- Sell The Fed Rip

Gold Primed For A Push Higher- Sell The Fed Rip 3 Things: Fed Error, Houston R/E, No Bounce?

3 Things: Fed Error, Houston R/E, No Bounce? Comcast Slides After Topping Disney In Bid To Buy Sky

Comcast Slides After Topping Disney In Bid To Buy Sky Silver Trading Strategy, XAGUSD Analysis & XAGUSD Forecast – Saturday, November 16

Silver Trading Strategy, XAGUSD Analysis & XAGUSD Forecast – Saturday, November 16 Banks’ crypto exposure must be disclosed — BIS’ Basel Committee

Banks’ crypto exposure must be disclosed — BIS’ Basel Committee The Growth Of The World’s Middle Class May Be The Greatest Story Of Our Age

The Growth Of The World’s Middle Class May Be The Greatest Story Of Our Age

Leave A Comment