There has been a lot of angst lately over the rise in interest rates and the question of whether the government will be able to continue to fund itself given the massive surge in the fiscal deficit since the beginning of the year.

While “spending like drunken sailors” is not a long-term solution to creating economic stability, unbridled fiscal stimulus does support growth in the short-term. Spending on natural disaster recovery last year (3-major hurricanes and two wildfires) led to a pop in Q2 and Q3 economic growth rates. The two recent hurricanes that slammed into South Carolina and Florida were big enough to sustain a bump in activity into early 2019. However, all that activity is simply “pulling forward” future growth.

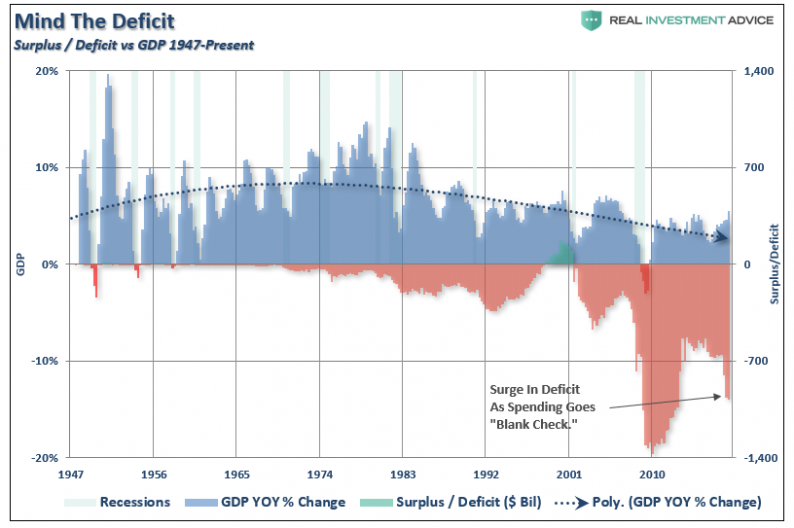

But the most recent cause of concern behind the rise in interest rates is that there will be a “funding shortage” of U.S. debt at a time where governmental obligations are surging higher. I agree with Kevin Muir on this point who recently noted:

“Well, let me you in on a little secret. The US will have NO trouble funding itself. That’s not what’s going on.

If the bond market was truly worried about US government’s deficits, they would be monkey-hammering the long-end of the bond market. Yet the US 2-year note yields 2.88% while the 30-year bond is only 55 basis points higher at 3.43%. That’s not a yield curve worried about US fiscal situation.

And let’s face it, if Japan can maintain control of their bond market with their bat-shit-crazy debt-to-GDP level of 236%, the US will be just fine for quite some time.”

That’s not a good thing by the way.

Let’s Be Like Japan

“Bad debt is the root of the crisis. Fiscal stimulus may help economies for a couple of years but once the ‘painkilling’ effect wears off, U.S. and European economies will plunge back into crisis. The crisis won’t be over until the nonperforming assets are off the balance sheets of US and European banks.” – Keiichiro Kobayashi, 2010

While Kobayashi will ultimately be right, what he never envisioned was the extent to which Central Banks globally would be willing to go. As my partner Michael Lebowitz pointed out previously:

“Global central banks’ post-financial crisis monetary policies have collectively been more aggressive than anything witnessed in modern financial history. Over the last ten years, the six largest central banks have printed unprecedented amounts of money to purchase approximately $14 trillion of financial assets as shown below. Before the financial crisis of 2008, the only central bank printing money of any consequence was the Peoples Bank of China (PBoC).”

Related Posts

USD/CAD Eyes Monthly Opening Range Ahead Of BoC Meeting

USD/CAD Eyes Monthly Opening Range Ahead Of BoC Meeting Dallas, Denver, Seattle Help Tip U.S. Housing Economics Toward Renting Over Buying

Dallas, Denver, Seattle Help Tip U.S. Housing Economics Toward Renting Over Buying The USD ‘Come-Back’; What’s Next? – BofA Merrill

The USD ‘Come-Back’; What’s Next? – BofA Merrill NYSE Short Interest Nears Record, Pre-Lehman Level

NYSE Short Interest Nears Record, Pre-Lehman Level Market Talk – Tuesday, February 6

Market Talk – Tuesday, February 6 SEC accused of ‘gaslighting’ in Coinbase rulemaking dispute

SEC accused of ‘gaslighting’ in Coinbase rulemaking dispute

Leave A Comment