For those that follow Treasury bond fluctuations closely, it’s been hard not to notice the persistent under performance in Treasury Inflation Protected Securities (TIPS) versus nominal coupon bonds over the last several years. It’s no surprise that inflation has been running below expectations for a long time, despite a steadily falling unemployment rate and a generally improving economy. Nevertheless, from a technical and fundamental perspective, the wide divergence that has formed between TIPS and fixed-coupon bonds can’t persist forever.

In fact, this week brought about new data from the Bureau of Labor Statistics on widely followed measures of inflation. Core CPI, which excludes food and energy, rose 2.3% in February in comparison to data released a year ago. For those that may not be familiar with TIPS, their coupon rate is tied to CPI, which in turn increases their payout in an inflationary environment. Also keep in mind that the Federal Reserve wants inflation back above the 2% mark so they can continue to justify rate increases.

We have been closely monitoring inflation ever since we initiated new holdings in inflation-linked bonds for clients in our Strategic Income Portfolio and subscribers to our Flexible Growth and Income Report. We believe that at this juncture, TIPS are grossly undervalued relative to other high flying areas of the Treasury market.

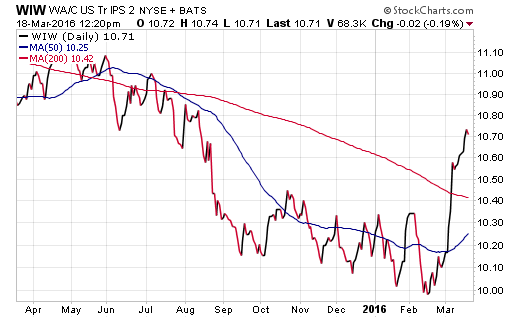

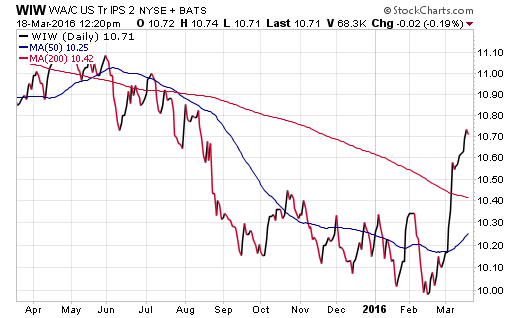

We initiated a purchase of the Western/Claymore Inflation Linked Opportunities Fund (WIW) last week, to capitalize on a reversal of the wide divergence that has formed between TIPS and fixed coupon treasuries. In addition, we see view position as a hedge against any unforeseen market volatility in the intermediate-term that could lead to another dip lower in interest rates.

We opted to go with a CEF in light of a more attractive yield, close tracking margin, and more exotic portfolio management style. We compared this opportunity closely with a traditional ETF such as the iShares TIPS Bond ETF (TIP) as a reasonable benchmark.

Leave A Comment