Written by John Davi, Astoria Portfolio Advisors

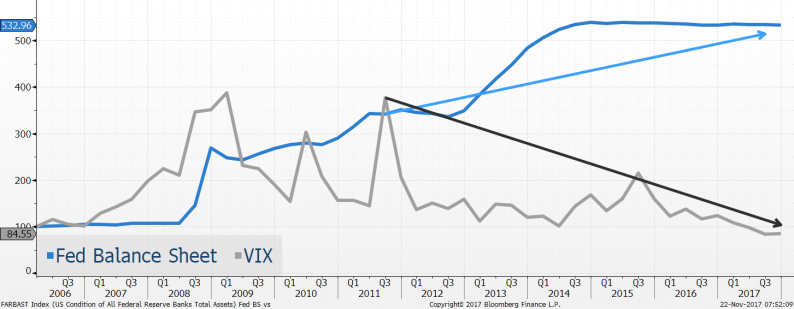

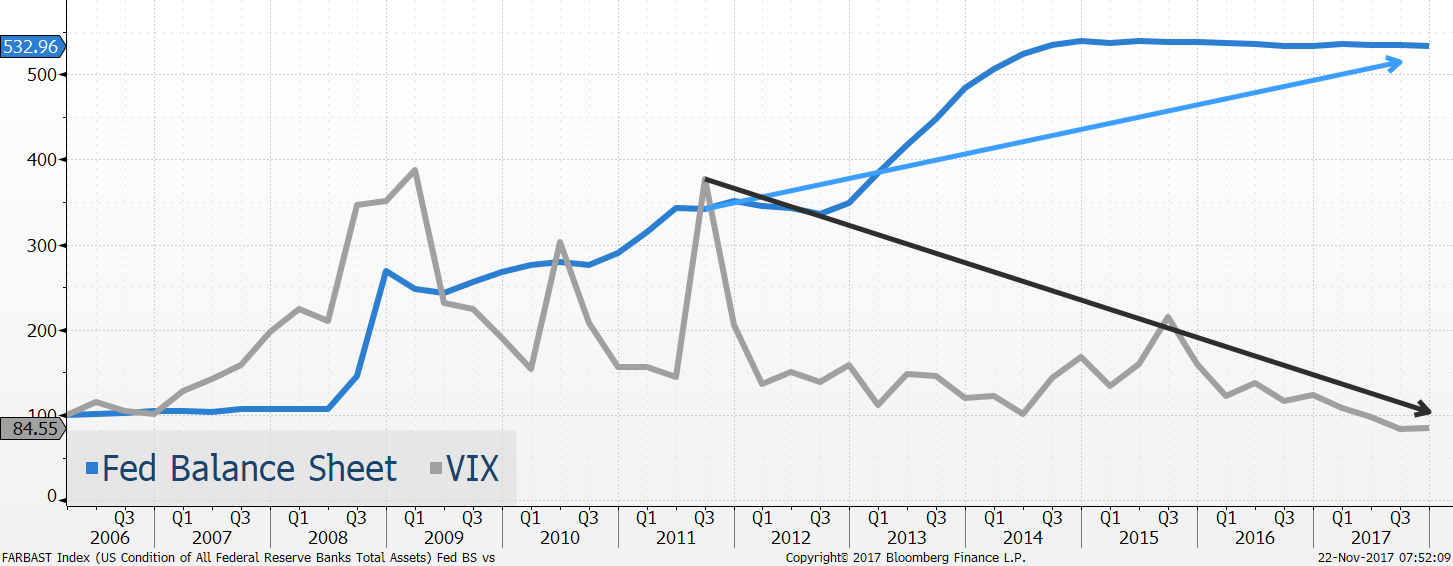

Are you surprised by VIX sub 10? You shouldn’t be. There is a direct linkage between liquidity and volatility as shown in the chart below.

Source: Bloomberg, Astoria Portfolio Advisors LLC.

This year, we have seen $2.2 trillion USD in central bank balance sheet expansion globally (approx. 15% of the aggregate balance sheet across the ECB, BOJ, and Fed). Right now, capital markets are swimming in an ocean of liquidity thanks to central banks flooding the system.

With low levels of economic uncertainty, low levels of earnings dispersion, and ample liquidity, it shouldn’t surprise investors that VIX is “low”. Moreover, there is a direct linkage between implied and realized volatility which reinforces another reflexive concept.

Several worlds are colliding. Earnings are improving, significant amounts of assets are moving into passive and systematic strategies (both of which deemphasize the capital markets aspect that active managers historically implemented), and dispersion is rising.This combination is resulting in lower levels of realized volatility. Reflexivity has been extreme.

The markets, however, trade on the margin and 2018 will begin to see liquidity decline in the US. The Fed has started to raise rates, wants to hike more, and quantitative tightening will further reduce liquidity.The repercussions are quite significant – especially on the margin.

It is not surprising that liquidity sensitive asset classes such as US high yield credit, US Small Caps, and Japan corrected in October/November. Historically, liquidity in capital markets starts to decline in Q4 as banks begin to wind down their balance sheet ahead of year-end.Plus, we have the potential for another Fed rate hike in December.The “liquidity based correction” was likely in anticipation of both events.

Leave A Comment