Benjamin Graham, Warren Buffett, Seth Klarman, John Templeton, Howard Marks, John Neff, Walter Schloss, Max Heine, Michael Price, Peter Lynch, Wilbur Ross, and many other investment managers created wealth for themselves and their clients based on the belief that the market price for an investment will, at times, vary substantially from the intrinsic value of the investment.

Knowing that superior returns are possible, as these individuals have shown over time, why do many investors today believe markets are so efficient that prices are always correct, and shun any idea that market prices can be wrong? I wish I could give you the answer to this, but I can’t. I can tell you that the individuals I listed, who found a way to capitalize on this discrepancy in the public markets, are considered an anomaly in the world of investment managers. Besides the skill needed to perform the fundamental work of discovering intrinsic value, it also takes a certain personality to take advantage of any price differences. Perhaps it is the personality of those individuals that makes for the anomaly, and not a superior quantitative security selection process. This is what Seth Klarman wrote in his year-end letter to his clients discussing the human qualities of a successful investor:

…a successful investor must possess a number of seemingly contradictory qualities. These include the arrogance to act, and act decisively, and the humility to know that you could be wrong. The acuity, flexibility, and willingness to change your mind when you realize you are wrong, and the stubbornness to refuse to do so when you remain justifiably confident in your thesis. The conviction to concentrate your portfolio in your very best ideas, and the common sense to nevertheless diversify your holdings. A healthy skepticism, but not blind contrarianism. A deep respect for the lessons of history balanced by the knowledge that things regularly happen that have never before occurred. And, finally the integrity to admit mistakes, the fortitude to risk making more of them, and the intellectual honesty not to confuse luck with skill….You don’t become a value investor for the group hugs.

Related Posts

Precious Metals Report – March 4, 2016

Precious Metals Report – March 4, 2016- Shrinking Home Sizes: Downtrend Continues

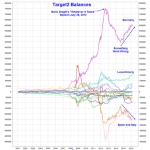

Capital Flight In Eurozone Continues

Capital Flight In Eurozone Continues- Crypto derivatives data signals improving investor sentiment and a possible trend reversal

T2108 Update – And Now The Waiting As The VIX Coils Its Springs

T2108 Update – And Now The Waiting As The VIX Coils Its Springs Looking For Ways To Squeeze More Yield Out Of Your Cash Pile? Me Too

Looking For Ways To Squeeze More Yield Out Of Your Cash Pile? Me Too

Leave A Comment