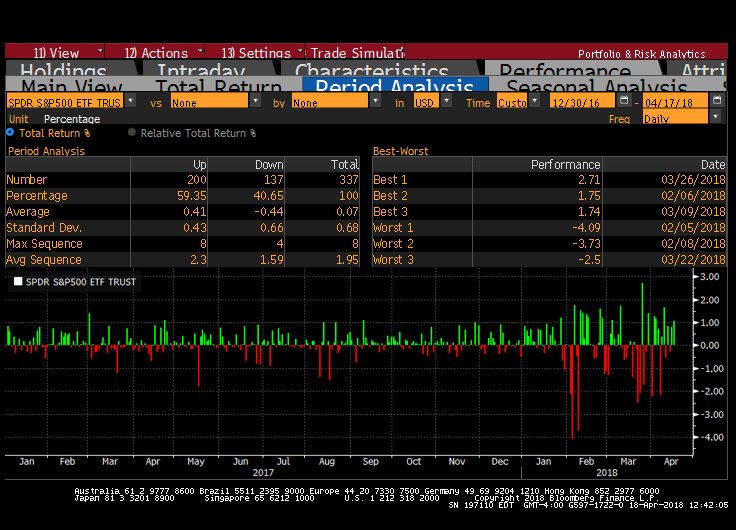

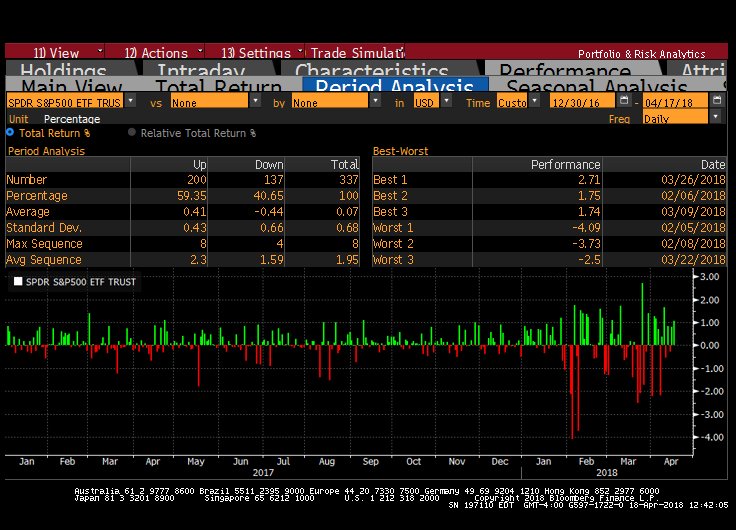

As you are no doubt experiencing, stock market volatility as spiked this year with the S&P 500 dropping or rising 2% or more on eight different days. Jolts of this size didn’t happen at all in 2017.

Source: Bloomberg, LP

The ramp up in volatility serves as a good opportunity to expand on the idea that long-term investors’ response to market volatility should be muted. In short, when prices drop, expected returns often increase. Those that react by trying to get off the ride by trading in and out of the market sadly have little evidence to support their urge. More, volatility spikes can bring benefits to long-term investors. For example, volatility may allow investors to harvest losses (generating higher after-tax returns) and could help keep the equity risk premium high (i.e., if expected volatility were permanently lowered, equity market expected returns would drop).(1)

To build a theoretical and empirical base for this conclusion, I will review a few key concepts associated with modern portfolio theory: Discount Rates, Expected Return Models, and Predictive Models. I will often reference articles by Prof. John Cochrane, current author of the blog “The Grumpy Economist,” a one-time University of Chicago professor and now a Senior Fellow at the Hoover Institute at Stanford. Prof. Cochrane’s articles are more comprehensive and mathematically robust than space (or talent!) allow for in this article, so my goal is to instead share the intuition behind some of these key tenants without the math.

Let’s start with the basics…

Discount Rates

The value of any asset is simply the sum of distributions adjusted for the 1) timing and 2) risk of the payments. With respect to timing, investors typically want their payments sooner rather than later, so future payments are less valuable than current cash (i.e., they sell at a discount). Regarding risk, when the value of the future payment is uncertain, this payment will receive a discount relative to a payment with no risk. What does a discount represent in a market? Well, whoever is buying this asset with a right to the risky cash flow will pay a discount to the face value of the cash flow so they can earn a higher expected return. Discount rates and expected returns are directly tied together (in theory).

Granted, a speculator in Cryptocurrencies may be wagering that someone else will eventually pay more in the future because of its potential role as a store of value. Similarly, a buyer of natural gas might pay-up for the convenience of owning it now versus the promise of owning it in the future. To simplify things, though, I’m going to assume the payments are in cold hard cash. And although I enjoy John Maynard Kayne’s metaphor that the stock market is like a beauty contest, I also appreciate that in practice, he was more of a value investor that used discount rates, and thus, I will also assume that investors can’t predict the fickleness of their fellow investors.

As a simple example, the current price of a bond is simply the summation of all of its future discounted coupons and principal payments. If a bond buyer feels that the rate to determine this discount (aka, the discount rate) is equal to the bond’s promised coupon payments she expects to receive (aka, earn), she will pay the full current face value of the bond. If she changes her mind and determines that the odds of a recession just increased such that she has less comfort that she’ll be paid back, she might increase her discount rate and the price she is willing to trade at will drop. On the flip side, if she feels her bond is free of default risk but a good place to hide, she might be willing to lower the expected return she needs to hold the bond and only be willing to trade it at a premium. Higher levels of change in the underlying discount rate for bonds leads to higher volatility in bond prices.

Related Posts

Bitcoin hits $35K after Biden reveals infrastructure deal, Paraguay proposes BTC bill

Bitcoin hits $35K after Biden reveals infrastructure deal, Paraguay proposes BTC bill After Bitcoin Futures Launched, Goldman Says Price Headed Higher, New Hedge Fund Launches

After Bitcoin Futures Launched, Goldman Says Price Headed Higher, New Hedge Fund Launches BlackBerry Patent Monetization Efforts Set To Step Up As Per Recent News

BlackBerry Patent Monetization Efforts Set To Step Up As Per Recent News- Emerson Electric Co. Dividend Stock Analysis

$475M in Bitcoin options expire this week — Are bulls or bears poised to win?

$475M in Bitcoin options expire this week — Are bulls or bears poised to win? 3 Highlights Of The Berkshire Hathaway Annual Meeting – May 4, 2024

3 Highlights Of The Berkshire Hathaway Annual Meeting – May 4, 2024

Leave A Comment