While toymaker Mattel’s (Nasdaq: MAT) stock has been recovering from the fallout of major retailer Toys“R”Us, sentiment about the firm appears to have turned bearish ahead of earnings.

MAT, owner of popular American franchises, including Barbie, Hot Wheels, Fisher-Price, and Thomas & Friends, has seen its sales suffer for a protracted period, amid mega-retailer Toys”R”Us’ bankruptcy.

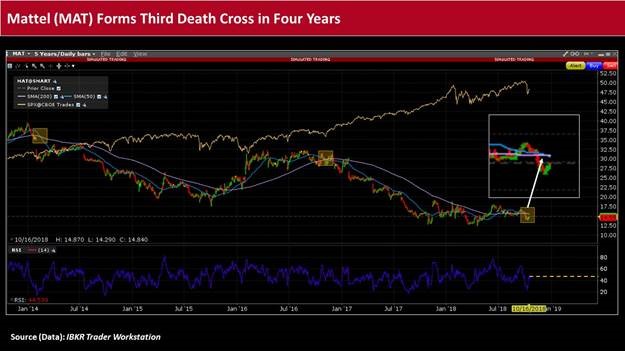

Shares of MAT have recovered roughly 16% of their losses since hitting a 52-week low of US$12.80 on March 21 – soon after the March 15 announcement of Toys”R”Us’ liquidation. However, the company’s sales have continued to decline, and the market appears to be jittery ahead of its third quarter of 2018 earnings figures set for release Thursday, October 25.

At the start of this past week, MAT experienced its third death cross since 2014, with the Relative Strength Index (RSI) – a momentum indicator that weighs the magnitude of recent price gains against the magnitude of losses – languishing below 50.00 (reflecting bearish short-term momentum).

Evolution and FX Headwinds

Part of MAT’s challenges appear to be driven by changing consumer interests and behaviors, amid ever-evolving technological advances.

Fitch Ratings analysts David Silverman and Monica Aggarwal recently noted that MAT has been “unable to effectively evolve its product portfolio commensurate with changes to children’s play patterns.” They observed that children have generally become “increasingly digitally oriented and marginally less interested in traditional toys.”

Fitch noted that Mattel’s traditional toy portfolio, including Barbie, has had “difficulty effectively retaining mindshare as this phenomenon progresses.” Furthermore, Mattel’s revenue base has become increasingly tied to licensed properties, which have created the dual risks of lost licenses, such as the Disney Princess line to Hasbro beginning in 2016, and underperforming properties, such as Cars 3 in 2017.

Leave A Comment