The Nasdaq and the S&P 500 hit new highs again on Thursday morning, with the benchmark crossing above 5,500 for the first time. Sellers then stepped in to send the S&P 500 down 0.3% and the tech-heavy index 0.8% lower on the day.The pullback was welcome and a larger near-term downturn would be healthy as the S&P 500 and the Nasdaq trade well above their 21-week and 21-day moving averages and at overbought RSI levels.The stock market is also in the midst of what could be a boring three-week stretch from now until after the 4th of July in terms of market-moving news. Therefore, now until the start of the busy portion of second quarter earnings season could mark an opportune time for Wall Street to take more profits after the massive first-half rally.  Image Source: Zacks Investment ResearchThankfully, the bullish backdrop remains deeply entrenched because corporate earnings are set to soar and the Fed is likely to cut rates. Investors should remain optimistic and take advantage of any near-term downturn.Today’s episode of Full Court Finance at Zacks explores Micron (MU) and Nike (NKE) ahead of earnings to see if investors should consider buying the soaring AI chip stock and the hard-hit sportswear giant down 45% from its highs with their earnings around the corner.Micron Technology, Inc. (MU) – Q3 2024 Earnings on June 26Micron is a memory chip powerhouse that grew massively over the last decade on the back of smartphones, data centers, connected vehicles, and more. MU has suffered various droughts in the cyclical semiconductor industry. But Micron always bounces back and it’s starting what could be its strongest stretch of growth ever as it benefits from its rise within the booming world of artificial intelligence.Micron has projected that AI will drive record demand for memory chips. CEO Sanjay Mehrotra said last quarter that MU will be “one of the biggest beneficiaries in the semiconductor industry of the multi-year opportunity enabled by AI.”

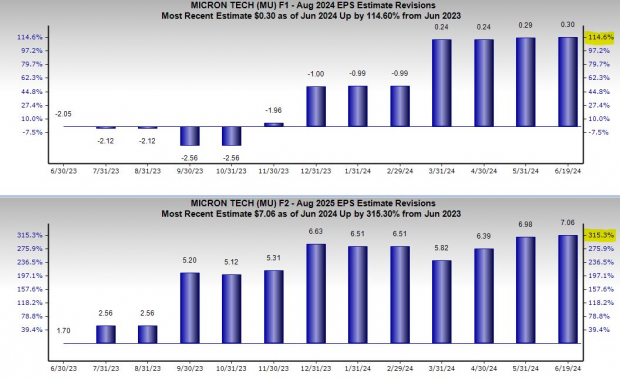

Image Source: Zacks Investment ResearchThankfully, the bullish backdrop remains deeply entrenched because corporate earnings are set to soar and the Fed is likely to cut rates. Investors should remain optimistic and take advantage of any near-term downturn.Today’s episode of Full Court Finance at Zacks explores Micron (MU) and Nike (NKE) ahead of earnings to see if investors should consider buying the soaring AI chip stock and the hard-hit sportswear giant down 45% from its highs with their earnings around the corner.Micron Technology, Inc. (MU) – Q3 2024 Earnings on June 26Micron is a memory chip powerhouse that grew massively over the last decade on the back of smartphones, data centers, connected vehicles, and more. MU has suffered various droughts in the cyclical semiconductor industry. But Micron always bounces back and it’s starting what could be its strongest stretch of growth ever as it benefits from its rise within the booming world of artificial intelligence.Micron has projected that AI will drive record demand for memory chips. CEO Sanjay Mehrotra said last quarter that MU will be “one of the biggest beneficiaries in the semiconductor industry of the multi-year opportunity enabled by AI.”  Image Source: Zacks Investment ResearchThe company in early May said it was the “first to validate and ship 128GB DDR5 32Gb server DRAM to address the rigorous speed and capacity demands of memory-intensive Gen AI applications.” On top of that, Micron is poised to pump upwards of $50 billion in gross capex through 2030 to build cutting-edge memory fabs in the U.S., boosted, in part, by U.S. government incentives.Micron is projected to grow its sales by 59% in FY24 and another 51% next year to reach $37.30 billion in FY25 to crush FY22’s $30.76 billion record. Meanwhile, it is projected to swing from an adjusted loss of -$4.45 per share last year to $0.88 in FY24 and skyrocket nearly 800% next year. MU’s impressive bottom-line revisions help it land a Zacks Rank #2 (Buy).MU also pays a dividend, supported by its great balance sheet, and 24 of the 27 brokerage recommendations Zacks has are “Strong Buys.”

Image Source: Zacks Investment ResearchThe company in early May said it was the “first to validate and ship 128GB DDR5 32Gb server DRAM to address the rigorous speed and capacity demands of memory-intensive Gen AI applications.” On top of that, Micron is poised to pump upwards of $50 billion in gross capex through 2030 to build cutting-edge memory fabs in the U.S., boosted, in part, by U.S. government incentives.Micron is projected to grow its sales by 59% in FY24 and another 51% next year to reach $37.30 billion in FY25 to crush FY22’s $30.76 billion record. Meanwhile, it is projected to swing from an adjusted loss of -$4.45 per share last year to $0.88 in FY24 and skyrocket nearly 800% next year. MU’s impressive bottom-line revisions help it land a Zacks Rank #2 (Buy).MU also pays a dividend, supported by its great balance sheet, and 24 of the 27 brokerage recommendations Zacks has are “Strong Buys.”  Image Source: Zacks Investment ResearchMU has climbed 375% in the past 10 years vs. Tech’s 333%, including a 160% run in the past two years and a 70% YTD climb. Micron fell 6% on Thursday to cool off.MU could face more near-term selling pressure, given that it trades well above its 21-day and at historically overbought RSI levels. Investors might want to buy Micron shares after any larger near-term dip.Nike (NKE) – Q4 2024 Earnings on June 27Nike stock has tumbled 45% from its 2021 highs and it’s down 12% YTD, lagging the beaten-down Consumer Discretionary sector’s 1% dip. Nike got caught in the broader consumer discretionary selloff, sparked by higher rates and rapidly changing consumer shopping patterns following the pandemic boom.Relative newcomers Hoka and On are challenging Nike in the running shoe segment, while Lululemon (LULU) and tons of digital upstarts eat away at its lead in athleisure and sportswear.Wall Street is also concerned about Nike’s pandemic-era pivot to go all-in on digital and direct-to-consumer, which happened under CEO John Donahoe—who took over from long-time boss Mark Parker in early 2020. Nike faces other near-term heads such as slowing expansion in China, a strong U.S. dollar, and more.

Image Source: Zacks Investment ResearchMU has climbed 375% in the past 10 years vs. Tech’s 333%, including a 160% run in the past two years and a 70% YTD climb. Micron fell 6% on Thursday to cool off.MU could face more near-term selling pressure, given that it trades well above its 21-day and at historically overbought RSI levels. Investors might want to buy Micron shares after any larger near-term dip.Nike (NKE) – Q4 2024 Earnings on June 27Nike stock has tumbled 45% from its 2021 highs and it’s down 12% YTD, lagging the beaten-down Consumer Discretionary sector’s 1% dip. Nike got caught in the broader consumer discretionary selloff, sparked by higher rates and rapidly changing consumer shopping patterns following the pandemic boom.Relative newcomers Hoka and On are challenging Nike in the running shoe segment, while Lululemon (LULU) and tons of digital upstarts eat away at its lead in athleisure and sportswear.Wall Street is also concerned about Nike’s pandemic-era pivot to go all-in on digital and direct-to-consumer, which happened under CEO John Donahoe—who took over from long-time boss Mark Parker in early 2020. Nike faces other near-term heads such as slowing expansion in China, a strong U.S. dollar, and more.  Image Source: Zacks Investment ResearchNike is streamlining its business to save up to $2 billion over the next three years. And don’t forget that it posted a massive stretch of revenue expansion between FY21 and FY23 (11% average sales growth). Nike is projected to post 1% revenue growth in FY24 and FY25.The sportswear and footwear powerhouse is expected to boost its adjusted earnings by 16% and 5%, respectively. NKE earns a Zacks Rank #3 (Hold) right now and its earnings estimates have held up recently. Nike has also crushed our bottom-line outlook in the trailing three periods.NKE shares have soared 640% in the last 15 years vs. the S&P 500’s 515%. The stock was crushing the benchmark until the last three years. Nike has dropped 27% as the S&P 500 surged 30%. Lululemon had been soaring, but it got crushed recently on slightly downbeat guidance, which Nike already got dinged for.

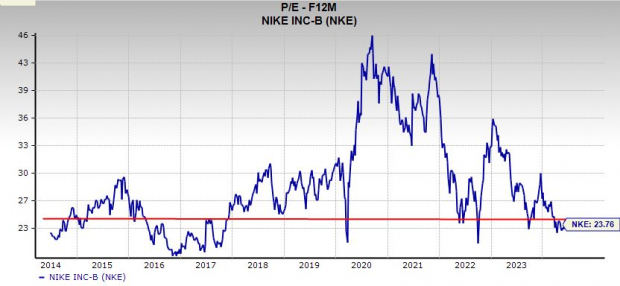

Image Source: Zacks Investment ResearchNike is streamlining its business to save up to $2 billion over the next three years. And don’t forget that it posted a massive stretch of revenue expansion between FY21 and FY23 (11% average sales growth). Nike is projected to post 1% revenue growth in FY24 and FY25.The sportswear and footwear powerhouse is expected to boost its adjusted earnings by 16% and 5%, respectively. NKE earns a Zacks Rank #3 (Hold) right now and its earnings estimates have held up recently. Nike has also crushed our bottom-line outlook in the trailing three periods.NKE shares have soared 640% in the last 15 years vs. the S&P 500’s 515%. The stock was crushing the benchmark until the last three years. Nike has dropped 27% as the S&P 500 surged 30%. Lululemon had been soaring, but it got crushed recently on slightly downbeat guidance, which Nike already got dinged for.  Image Source: Zacks Investment ResearchNike is back above its 21-day and 50-day moving averages, but well below its 200-day. NKE got rejected by its 21-week recently. Nike trades 20% below its average Zacks price target and 45% below its all-time highs at around $95 per share. Nike trades at a 50% discount to its 10-year highs and 12% under its median at 23.8X forward 12-month earnings. Investors might want to take a chance on NKE as Wall Street starts to look for deals. More By This Author:3 Oversold S&P 500 Stocks Down At Least 15% To Buy In June Bear Of The Day: O-I Glass, Inc. Buy This Surging Tech Stock Now and Hold?

Image Source: Zacks Investment ResearchNike is back above its 21-day and 50-day moving averages, but well below its 200-day. NKE got rejected by its 21-week recently. Nike trades 20% below its average Zacks price target and 45% below its all-time highs at around $95 per share. Nike trades at a 50% discount to its 10-year highs and 12% under its median at 23.8X forward 12-month earnings. Investors might want to take a chance on NKE as Wall Street starts to look for deals. More By This Author:3 Oversold S&P 500 Stocks Down At Least 15% To Buy In June Bear Of The Day: O-I Glass, Inc. Buy This Surging Tech Stock Now and Hold?

Related Posts

Buffalo Wild Wings Stock Down On Q1 Earnings & Revenue Miss

Buffalo Wild Wings Stock Down On Q1 Earnings & Revenue Miss- Q2 Earnings Drive Pharma ETFs Higher

Institutions have no appetite for Bitcoin at this price level: JPMorgan

Institutions have no appetite for Bitcoin at this price level: JPMorgan Gold Now At The Tipping Point

Gold Now At The Tipping Point Cesca Therapeutics Announces Registered Direct Offering

Cesca Therapeutics Announces Registered Direct Offering- EC

Ignoring The Mathematics Of Ideology When It Becomes Uncomfortable

Leave A Comment