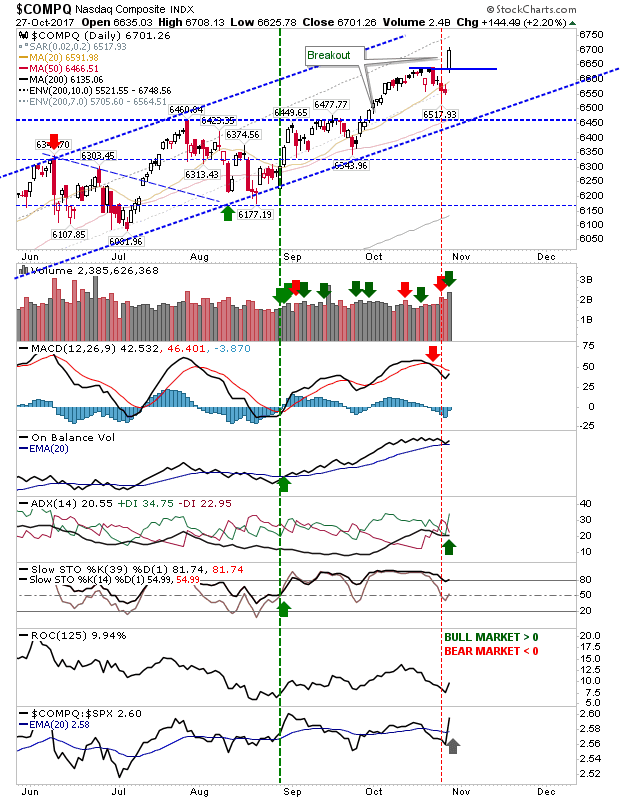

Tech markets, helped by Amazon, Apple and Alphabet, surged into fresh breakouts. The Nasdaq and Nasdaq 100 enjoyed strong volume with renewed ‘buy’ signals for the MACD in the Nasdaq 100 and +DI/-DI in the ADX for the Nasdaq.

Not surprisingly, there were gains for the S&P. Better still, the higher volume accumulation in this index negated the prior week’s ‘bull trap’. The breakout didn’t change the technical picture and the index is still edging a relative advantage over Small Caps.

The Dow was a disappointment. It enjoyed the volume but not the relative gain.

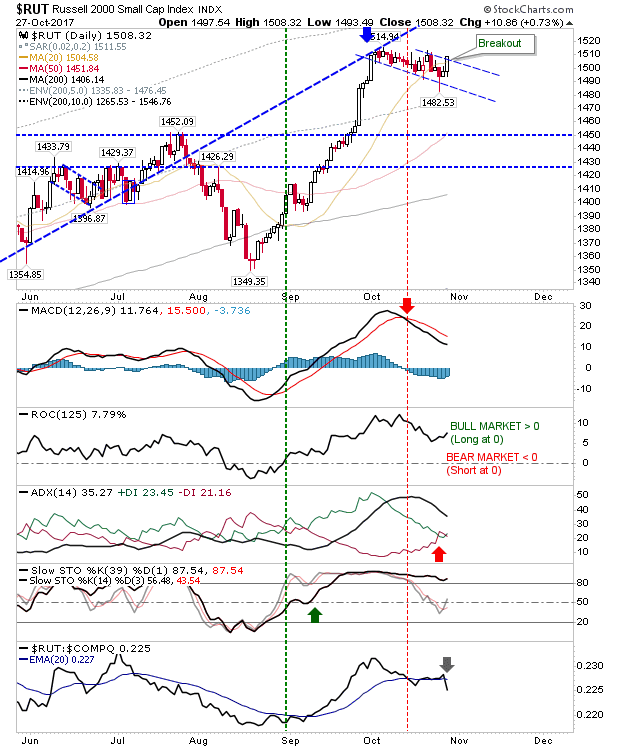

Small Caps continued to map out a broader ‘bull flag’. An argument could be made for a breakout from the ‘flag’ but Monday will tell. If there is a downside, because of bigger gains in other indices it has suffered a relative loss – reflecting a rotation of funding out of Small Caps – a potentially bearish scenario.

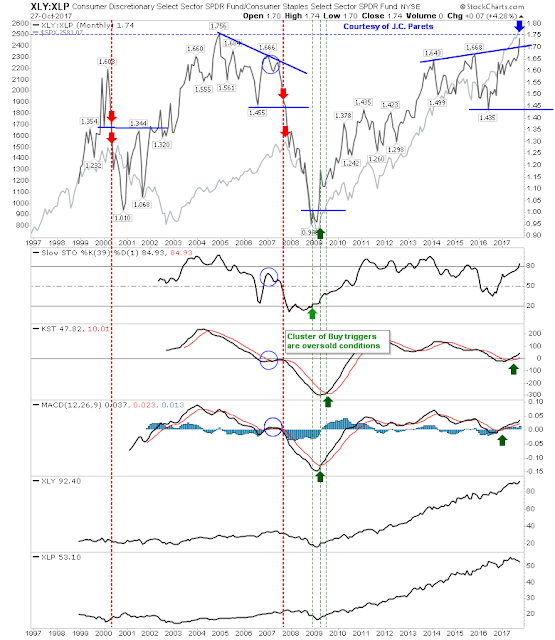

On longer time intervals the relationship between Discretionary and Staples has seen a marked acceleration. This has pushed past resistance and effectively reset the bear count. There is no immediate concern for bulls as a peak high here often leads a market top by a few months to a couple of years.

The more worrying set up for bulls is the relationship between Dow Transports and Dow Industrials. This is fast approaching support and a potential breakdown.

Big gains on opening gaps could kick start a new run much like breakouts in late September were followed by 4-5 days of gains. Better still, Friday’s breakouts were bigger than September breakouts.

Leave A Comment