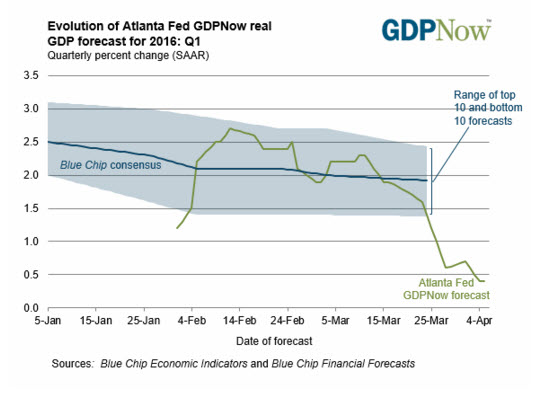

Is the U.S. economy really in great shape? The U.S. Federal Reserve does not seem to think so. They started the year with an intention of raising the overnight lending rate four times – from 0.25% to 1.25%. In March, they announced that it would more likely be a mere two. And today, the Atlanta Fed downgraded its Q1 estimate for gross domestic product (GDP) to a new low for the year (0.4%).

Granted, GDP for the fourth quarter of 2015 came in at a better-than-expected 1.4% after its third revision. However, that is significantly lower than the average economic performance since 2009 of 2.1%.

And then there’s Gross Domestic Income (GDI). This measure looks at the income earned while producing goods and services (as opposed to measuring them on expenditures). GDI finished Q4 2015 at a sub-standard 0.9%, confirming widespread weakness. (Note: Theoretically, GDP and GDI should match one another, but they deviate due to different methods of calculation.)

If one ignores the average rate of U.S. expansion in history, disregards the current 6-month slowdown in GDP/GDI, and overlooks the Federal Reserve’s emergency measures for monetary policy accommodation, one might applaud the economic “progress” made between 2009 and 2016. Conversely, realistic observers know that things are not that rosy.

For example, U.S. government debt has swelled from roughly $11 trillion to $19 trillion. That’s a great deal of stimulus to keep the economy afloat. The Fed’s balance sheet has bloated from $800 billion to nearly $5 trillion. That’s an incredible amount of stimulus designed to bolster borrowing activity. Yet the big bang from the $12 trillion-plus injection is an economy that can barely hold its head above water.

Apologists point to other data points that suggest the U.S. economy is dandy. “Robust job growth,” they say. Of course, they neglect to mention that low-quality positions in leisure, hospitality, retail and customer service account for most of the gains, whereas high-paying positions, particularly in manufacturing, continue to evaporate. That data shows up in average hourly earnings, where stagnation in wages are indicative of a shift toward lower-paying jobs with fewer hours.

Related Posts

AUDUSD Weekly Analysis – Sunday, May 6

AUDUSD Weekly Analysis – Sunday, May 6- UK uses Love Island star to warn finfluencers on crypto and investment schemes

- Pandora Climbs After BMO Upgrades, Says Changes ‘Underappreciated’

- Insurance ETFs Looking Good Post Q2 Earnings

Bank Of America; “This Could Get Ugly, We Think”

Bank Of America; “This Could Get Ugly, We Think”- Hold The Champagne And Truffles: Yellen’s Story Not Yet Written

Leave A Comment