Reader Arthurian writes in the wake of the 3% growth rate (SAAR) reported for 2017Q3:

Back in January Menzie Chinn said he thought growth in the 3.5-4% range was “unlikely”. I wonder if he is having second thoughts now.

I’m going to show two pictures deploying at most undergraduate statistics to show why I — like most numerically literate people — still think sustained 3.5% growth is unlikely.

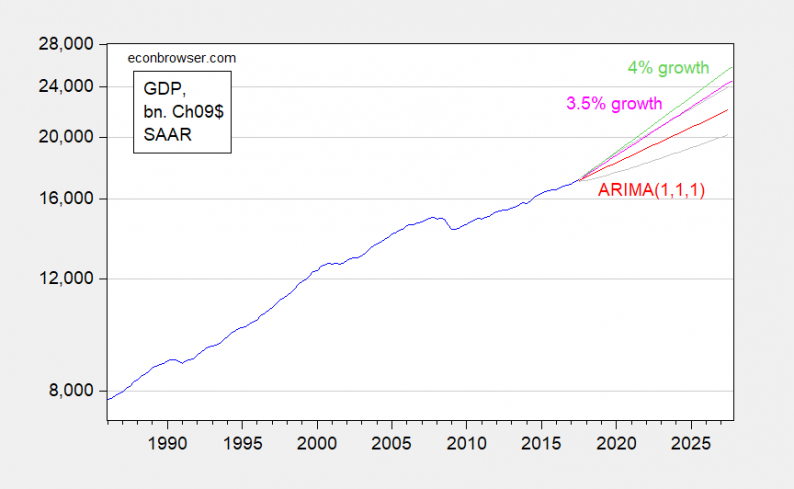

First, consider what a naive statistical model — an ARIMA(1,1,1) estimated over the 1986-2017Q3 period — says, as compared to a 3.5% or 4% growth rate.

Figure 1: Reported GDP (blue), ARIMA(1,1,1) dynamic forecast (red) and 64% prediction interval (gray lines), implied path for 3.5% sustained growth (pink) and for 4% (light green), all billions Ch.2009$ SAAR.

Source: BEA 2017Q3 advance release, author’s calculations.

Note that by estimating the regression starting in 1986 when the trend growth rate was relatively high, I am slanting the results toward projecting faster growth. Even then, the 3.5% growth rate is at the uppermost edge of the 64% prediction interval. 4% growth is even more laughable.

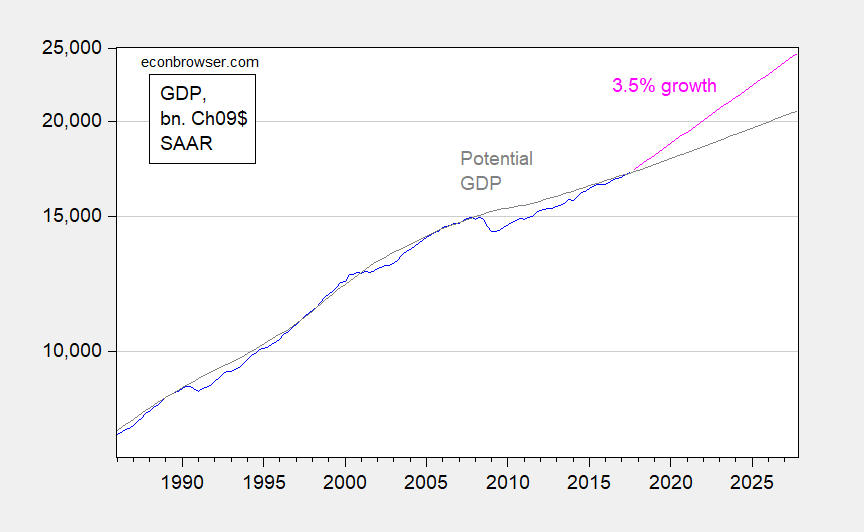

Second, now consider what sustained 3.5% growth implies for the output gap. For that calculation, one needs an estimate of potential GDP; for want of a better measure, I use CBO’s estimate. This is shown in Figure 2.

Figure 2: Reported GDP (blue), implied path for 3.5% sustained growth (pink) and potential GDP, all billions Ch.2009$ SAAR.

Source: BEA 2017Q3 advance release, CBO (June 2017), author’s calculations.

Assuming sustained 3.5% growth, the output gap by end-2019 would be 4.2%, 5.9% by end-2020. Of course, CBO could be terribly misguided about the trajectory of potential GDP. But in order to believe potential GDP can grow at 3.5%, I really do believe that it can only be done by adherence to January. Refer to Figure 3, reproduced from my January post, and look at what the orange bar — labor productivity — has to do in order to hit 3.5% potential growth.

Related Posts

EUR/USD: Broader Bias Remains Higher On Bullishness

EUR/USD: Broader Bias Remains Higher On Bullishness WTI/RBOB Extend Losses After Unexpected Crude Build

WTI/RBOB Extend Losses After Unexpected Crude Build Metaverse ETF ‘PUNK’ closing after betting against Meta’s vision

Metaverse ETF ‘PUNK’ closing after betting against Meta’s vision U.S. Bond And U.S. Stock Soaring Together?

U.S. Bond And U.S. Stock Soaring Together? PE And VC Opportunities In 21st Century India

PE And VC Opportunities In 21st Century India Warmer Long-Range Forecasts Pull Natural Gas Prices Lower

Warmer Long-Range Forecasts Pull Natural Gas Prices Lower

Leave A Comment