NW Natural (NWN) has a track record of dividend increases that puts it in very exclusive company. NWN has increased its cash dividend for more than 60 consecutive years, making NWN one of just a handful of companies in the entire market with a dividend increase streak of that length. That puts it among the elite Dividend Kings, a small group of stocks that have increased their payouts for at least 50 consecutive years.

Dividend Kings are the best of the best when it comes to rewarding shareholders with cash and this article will discuss NWN’s dividend and outlook.

Business Overview

NWN is headquartered in Portland, Oregon just a few blocks from where the company was founded in 1859. The business that started with just 49 customers in one square mile of Portland has since grown to serve almost 740,000 customers in 107 communities in Oregon and Southwest Washington. NWN has grown to 1,100 employees since its founding by just two men, a product of the amount of growth it has experienced.

NWN’s stated mission is to deliver natural gas safely and reliably to its customers in the Pacific Northwest. The company achieves this by purchasing natural gas from suppliers in the Western US and Canada and distributing it to residential, commercial and industrial customers throughout its service area. NWN builds, maintains and operates the local natural gas distribution system including pipes and related equipment that transport natural gas to its customers. NWN believes customers in its service area prefer natural gas to electricity for heating needs and continues to capitalize on that growth opportunity.

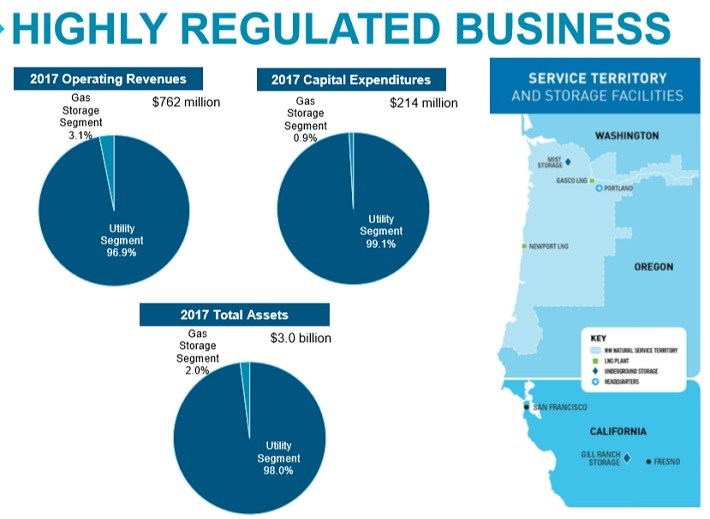

NWN gets almost all of its revenue from selling natural gas to its customers. This chart shows not only how the company’s revenue is broken down, but also the composition of its asset base and capex.

Source: March 2018 investor presentation, page 7

NWN has a gas storage segment it operates via two subsidiaries but as you can see, that segment is but a small fraction of NWN’s total business. This is a pure-play LDC natural gas enterprise in every sense of the term and this company is very good at it.

NWN’s pricing – as a regulated utility – is completely out of its control. Oregon and Washington regulators require NWN to adjust its rates each year based on how much it pays for gas during a 12-month period. The Weighted Average Cost of Gas helps determine how much its customers will pay for each therm (a unit of heat equivalent to 100,000 Btu) of gas. These annual Purchased Gas Adjustment changes take effect on November 1 of each year.

NWN does not profit from the price of gas; the cost of natural gas is a pass-through and is not marked up. This obviously introduces some level of risk to NWN’s revenue growth but of course, this is not unique in the utility industry; it is just something to be aware of.

NWN’s market cap is about $1.6B and it is expected to do almost $800M in total revenue this year. The company’s residential customers make up roughly two-thirds of its business while commercial accounts are about one-fourth, with the balance coming from industrial clients. You’d expect this sort of makeup from a utility so no red flags here, and NWN is committed to growing its residential business in particular because the market opportunity is significant; more on that later.

NWN’s risks to revenue include population growth in its service areas, regulation in terms of pricing as well as potential consumer preference shifts away from natural gas. NWN also faces the risk of some sort of environmental disaster at one of its facilities that could potentially not only disrupt service, but carry with it extraordinary cleanup and legal costs. However, these risks have been present for as long as NWN has been in business and will continue to be and at this point, should not be considered material. NWN operates as a monopoly in its service areas, competing only with other forms of energy, and it plays nice with regulators and the environment.

Related Posts

Lumber Liquidators Sinks After CDC Says Cancer Risk Higher Than Thought

Lumber Liquidators Sinks After CDC Says Cancer Risk Higher Than Thought- E

Greenbrier: Is This The Next Shoe To Drop?

- German Import Prices Rise To 4-Month High In September

Bull Of The Day: SodaStream (SODA)

Bull Of The Day: SodaStream (SODA) WEF 2022, May 25: Latest updates from the Cointelegraph Davos team

WEF 2022, May 25: Latest updates from the Cointelegraph Davos team USD Shows A Wide Range Of Waves Versus EUR, GBP And JPY

USD Shows A Wide Range Of Waves Versus EUR, GBP And JPY

Leave A Comment