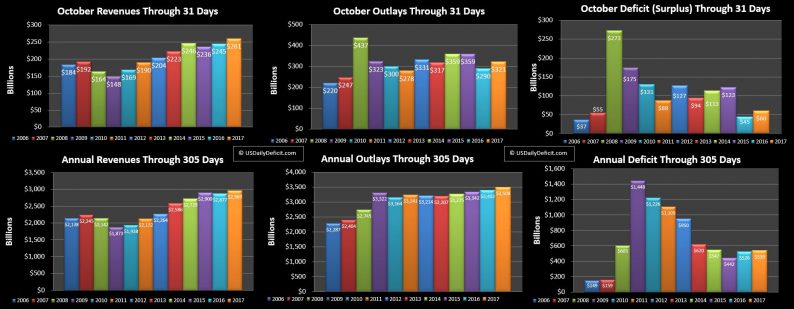

We now have the finals for October which clocked a $60B cash deficit.

Revenues were solid, up $15B, but there was an extra day so it’s not as impressive…but still good

However, outlays were up $30B…some timing, some because of the extra day, and a good chunk of debt issued at a discount….nearly $10B when a normal month may be at $5B. The deal with this is… say Treasury issues a $100 12 month bill for $99….they get $99 of cash, but debt increases $100B. Now in a perfect world I would amortize that $1 over the year, but to avoid a lot of unnecessary complexity that would add little value…I essentially just book the interest expense when it is issued. Over the year….it should more or less pencil out, and it’s not material anyway…but now you know!! Anyway…I’ll keep an eye on it but it’s probably nothing.

Year To Date

Looking at the YTD…Revenue is solid(and boring) at +3.2% so are outlays at +3.1%. The 2017 YTD has now overtaken 2016 after trailing slightly for most of the year. It’s only at +$13B, but with 2 months to go 2017 is on track to top 2016’s $697B deficit by a little….then we go on to 2018…will it be more of the same, or will a tax cut actually sneak through and put us back over $1T?

November Outlook

Looking forward to November, I am expecting about a $150B, in line with last November driven by lower revenues and rising outlays, including about $42B of interest payments.

Related Posts

UK Inflation Misses – GBP/USD Loses Ground

UK Inflation Misses – GBP/USD Loses Ground Silver Prices Are Expected To Drift Higher

Silver Prices Are Expected To Drift Higher How Much Is That Asset In The Window?

How Much Is That Asset In The Window? The Amazing Picture Of America’s Oil Export Growth

The Amazing Picture Of America’s Oil Export Growth Limited Changes Likely Before June 30 Acreage & Quarterly Stocks Reports

Limited Changes Likely Before June 30 Acreage & Quarterly Stocks Reports Week Ahead: Trade Wars And Central Banks To Dominate Markets

Week Ahead: Trade Wars And Central Banks To Dominate Markets

Leave A Comment