The U.S. energy resurgence has been one of the bright spots of the economic recovery since the Financial Crisis of 2008. Many of the shale plays in Texas financed their growth with cheap debt. Now that oil has fallen from above $100 to sub-$50 many oil drillers are finding it difficult to service that debt. Through mid-December, there were 41 oil and gas bankruptcies with collective debt exceeding $16 billion.

Are Bankers Looking To Save Themselves?

Banks have feasted on fees and interest income from energy loans since the crisis. Now that drillers and oilfield services firms are finding it difficult to service that debt banks want out in order to save themselves. If they can’t sell the paper at cents on the dollar, banks have been willing to fob off their exposure onto shareholders of the underlying credits.

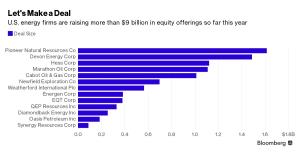

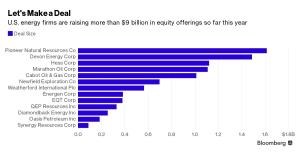

In early March, oil and gas companies had announced plans to raise as much as $9.2 billion in new equity:

U.S. oil and gas companies from Marathon Oil Corp. MRO to Weatherford International WFT have announced plans to raise about $9.2 billion in new equity, the most year-to-date since at least 1999… Until only a few weeks ago, bankers, executives and investors had assumed the capital markets were closed to the energy sector, which is laboring under oil prices that have fallen almost 70 percent from the summer of 2014. Then, in early January, a handful of companies with assets in the prized Permian Basin in Texas successfully tested the waters. Now “the window is clearly open” for almost everybody, Tudor, Pickering, Holt & Co. said.

I had originally thought the equity capital would be used to help the indebted firms stave off the downturn in the oil market. However, in many instances, the additional equity was used to repay debt to bankers who wanted out before the companies collapsed.

Pioneer PXD, Diamondback FANG, Synergy SYRG, Cabot COG, Energen EGN, Weatherford International, Devon Energy DVN and Newfield NFX were expected to use the funds to pare debt, and in some cases, secured revolving debt.

Related Posts

Silver Weakness Persists But A Breakout Could Happen

Silver Weakness Persists But A Breakout Could Happen- Sensex Opens Flat; Healthcare Stocks Lead

- Market At Record Highs; GDP Growth; Tata Steel And Other Top Cues To Sway The Market Today

Gold Stocks: An Inflationary Money Train

Gold Stocks: An Inflationary Money Train- Intel: A Technology Giant Paying Uninterrupted Dividends Since 1992

Surging North American Silver Investment Pushes Domestic Supply Deficit To New Record

Surging North American Silver Investment Pushes Domestic Supply Deficit To New Record

Leave A Comment