The overnight exuberance in crude oil futures markets has faded notably as the day has worn on. While news of supply cuts are unquestionably bullish (should one choose to believe it or not, remember the Saudis admission “we tend to cheat”), but the last few days have also seen a plethora of bearish-biased news that for now is being ignored.

The excitement is fading…

As large specs have never been more bullish crude… Investors are betting the rally will continue as we head into 2017. Money managers boosted wagers on higher Brent crude prices to a record before non-OPEC producers agreed Dec. 10 to join OPEC nations in cutting output. Their net-long position in the global benchmark surged by 46 percent in the week ended Dec. 6 to 452,585, the highest in data from ICE Futures Europe going back to 2011. Long positions also surged to a record.

But at the same time, US oil fund USO suffers the biggest 2-week outflows since 2009… U.S. Oil Fund had $197.1m outflow last week following $367.9m outflow the week before, biggest consecutive 2-week outflow since March 2009, according to data compiled by Bloomberg.

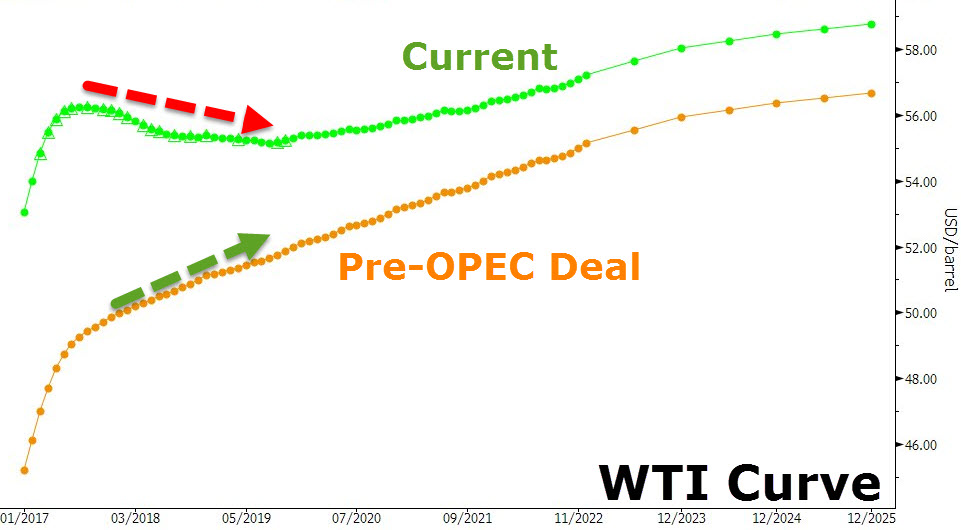

And while the front-end of the crude curve remains steeply contango, the belly has notably inverted into backwardation…

The biggest backwardation since Oct 2014 suggesting producers are hedging aggressively as opposed to believing the higher-for-longer hype.

Part of the steepness of the backwardated curve likely derives from the increasing belief that continued growth of crude supply in North America will have a tendency to drive cash prices in the future towards the marginal cost of production (i.e. lower)… and this is happening as Cushing crude inventories are soaring…

Related Posts

Morning Call For June 2, 2016

Morning Call For June 2, 2016 Pro traders know it’s time to range trade when this classic pattern shows up

Pro traders know it’s time to range trade when this classic pattern shows up Today’s Trading Plan: Forging Ahead

Today’s Trading Plan: Forging Ahead Silver Price Close To Major Breakout

Silver Price Close To Major Breakout RGS Energy Announces Public Offering Of Common Stock And Warrants

RGS Energy Announces Public Offering Of Common Stock And Warrants BofA Beats Despite 14% Slump In FICC Revenue; Interest Income Unexpectedly Declines

BofA Beats Despite 14% Slump In FICC Revenue; Interest Income Unexpectedly Declines

Leave A Comment