Oil has stayed resilient during the past few weeks, despite occasional risk-off sentiment. Crude prices rose to their highest in three months in early March, at $42.49/barrel for WTI and $42.54/barrel for Brent. This was triggered by a combination of tightening supply, a proposed production freeze and a weaker US dollar. However, the November-December range of $44.16-$46.46 may act to cap higher development in WTI oil in the near term. Looking ahead, the April 17 Doha meeting to freeze output is a main event for the supply side, whereas demand growth from the main consumers may continue to slow down.

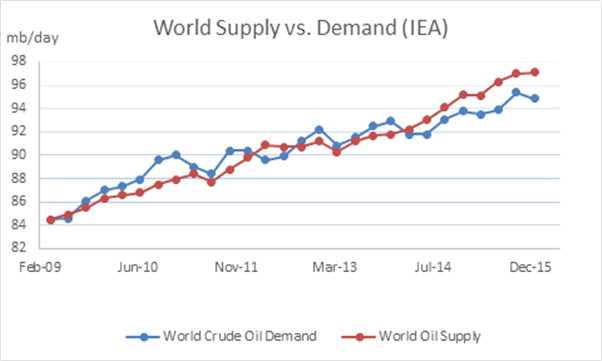

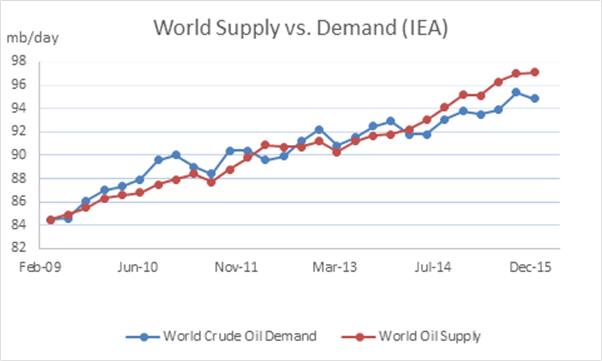

Chart 1. Source: International Energy Agency (IEA) via Bloomberg

Global oil supplies diminished by 180,000 barrels per day in February, according to International Energy Agency’s March report, although the pace of reduction has been painfully slow. Within the OPEC group, decreased output from Iraq, Nigeria and the UAE was offset by a rise in Iran’s production after sanctions were lifted. In the U.S., shale oil producers recently halted their cuts of active rigs, according to Baker Hughes Inc. This pattern will likely continue in the foreseeable future, unless an accord to freeze output is reached at the upcoming producers gathering. Qatar has successfully arranged a meeting among OPEC members and other major oil producers to cap their production at January’s levels, in order to reduce the supply surplus. At the time of writing, Qatar’s Minister of Energy and Industry confirmed attendance by 15 countries within and outside OPEC, with the self-exclusion of Iran and Libya. If this meeting does not come to fruition, similar recommendations would likely be discussed at OPEC’s semi-annual meeting on June 2.

Supplies from major producers have built up over the years, according to statistics by the International Energy Agency (chart 2). However as low oil prices take their toll on upstream investments, plunging supply growth could eventually lead to a price recovery.

Related Posts

Here’s How To Trade The Biggest Political Event Risk In The Developed World

Here’s How To Trade The Biggest Political Event Risk In The Developed World WTI Crude Oil And Natural Gas Forecast – Wednesday, Oct. 18

WTI Crude Oil And Natural Gas Forecast – Wednesday, Oct. 18 Magic Formula Weekly Roundup – October 15, 2015

Magic Formula Weekly Roundup – October 15, 2015 Market Talk – November 27, 2015

Market Talk – November 27, 2015 Litecoin Price Breaking Out Of A Resistance Area

Litecoin Price Breaking Out Of A Resistance Area Elliott Wave Technical Analysis: Iron Ore Commodity – Friday, July 5

Elliott Wave Technical Analysis: Iron Ore Commodity – Friday, July 5

Leave A Comment