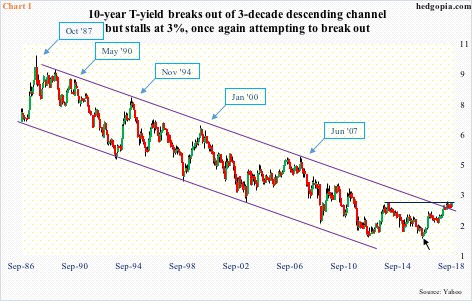

The 10-year Treasury yield is at it again, trying to convincingly break out of just north of three percent. Shorts have done very well in the past year. They will mint money should a breakout occur. A lack thereof also raises the odds of a squeeze in due course.

Once again, the 10-year Treasury rate is hammering on three percent. In fact, it closed Tuesday north of it – to a nearly four-month high 3.05 percent. The last time it reached that level before coming under sustained pressure was December 2013, when it retreated after hitting 3.04 percent. By July 2016, 10-year notes were yielding 1.34 percent (black arrow in Chart 1). This was a major bottom, followed by channel breakout. This is not any one of those plain-vanilla channels – goes back three decades. The breakout took place in April this year. Yields have since stayed above, but building on it has proven difficult. The culprit is resistance at just north of three percent. Hence its significance.

In the past year, the 10-year has rallied 100 basis points. Just in the past month, it has gone up 24 basis points. What could be causing this? Could China – the largest holder – be unloading its holdings? As of July, China held $1.17 trillion in Treasury securities, down $7.7 billion month-over-month. As early as August last year, it held $1.2 trillion. At the same time, holdings were merely $1 trillion in November 2016. So China likely is not a factor. At least not yet.

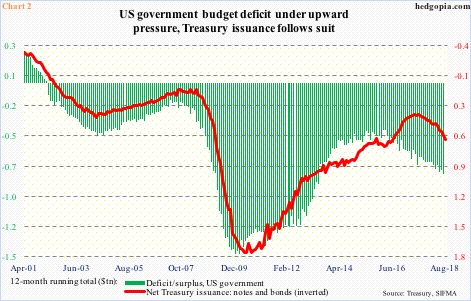

Bond bears can cite other fundamental reasons for their bearishness, one of which is the rising US budget deficit. On a 12-month rolling total basis, the deficit reached $783.8 billion in July. This was the highest since May 2013 (Chart 2). This needs to be funded. Consequently, Treasury issuance is rising. In the 12 months through August, issuance totaled $581 billion – the highest since June 2016.

Concurrently, the Fed is also cutting back on its Treasury holdings. As of last Wednesday, it held $2.16 trillion in Treasury notes and bonds, down from $2.35 trillion in October 2014. Beginning this October, the pace of reduction is set to accelerate. If this selling is not met by demand elsewhere, bonds come under pressure.

Related Posts

Biggest Drop In Small Business Sentiment Since 2015

Biggest Drop In Small Business Sentiment Since 2015 Why For The First Time In Six Years, Hedge Funds Are At The Mercy Of Retail Investors

Why For The First Time In Six Years, Hedge Funds Are At The Mercy Of Retail Investors Price analysis 3/25: BTC, ETH, BNB, XRP, ADA, LUNA, SOL, AVAX, DOT, DOGE

Price analysis 3/25: BTC, ETH, BNB, XRP, ADA, LUNA, SOL, AVAX, DOT, DOGE I Lived Nowhere And With Nothing For The Past Year – This Is What Happened…

I Lived Nowhere And With Nothing For The Past Year – This Is What Happened…- ETFs To Watch On Starbucks Mixed Q1 Results

- USDCAD Daily Analysis – Friday, Oct. 26

Leave A Comment