One of the notable market developments over the past month was the spike in HY’s correlation to crude prices when oil took a bath in early March.

To be sure, that wasn’t entirely surprising, but it was nonetheless notable for what it likely said about the extent to which popular HY ETFs are vulnerable to swings in commodity prices.

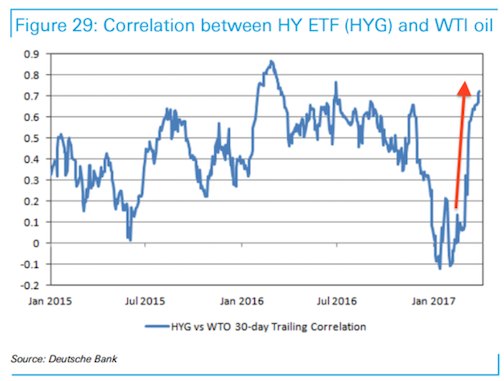

Indeed it was just a few weeks later when Deutsche Bank (DB) decided to look specifically at HYG’s correlation with crude and of course, it jumped materially to (almost) the highest level since 2016’s deflationary doldrums:

(Deutsche Bank)

Well, that obviously raises questions about volatility in the commodities space and about the extent to which that volatility will ultimately spill over into risk assets that you might (or might not) own.

And so, in the spirit of keeping you up to speed on the latest, here’s what Goldman said this afternoon about everything discussed briefly above…

Via Goldman

What’s been happening with oil prices? Commodities have been among the most volatile of assets since the start of March, with copper, oil and gold all moving notably more than other assets (Exhibit 1)…

…and with oil spot having the largest cross-asset return over the past two weeks. The recent volatility of oil is particularly stark given its relatively range-bound prices in the first 2 months of the year. Since we commented on their initial increase one month ago, risky asset correlations with oil have generally remained elevated (Exhibit 25)…

…although MSCI World was actually down this past week. US high yield remains a beneficiary of higher oil prices, with notable inflows in the past 2 weeks alongside the energy recovery.

CFTC data indicates net long positioning has actually come down materially in both WTI oil and copper futures (Exhibit 37). In contrast to this more skeptical signal from investors, our commodities team remains confident that rebalancing of the oil market is making progress alongside strong demand and the 1H17 OPEC cuts. They continue to forecast Brent oil prices at $57/bbl in 2H17, with backwardation coming in 2H17 as well, resulting in positive roll returns for oil.

Leave A Comment