“…emerging markets experienced a more recent run-up in indebtedness, which started around the time of the crisis, and is still continuing. In other words, their deleveraging has not even begun. This has the potential to create persistent spending disappointments, if monetary policy is unable to stimulate other spending sufficiently.” – “Debt, Demographics and the Distribution of Income: New challenges for monetary policy” – Gertjan Vlieghe, Member of Monetary Policy Committee, Bank of England, January 18, 2016.

This observation from Vlieghe of the Bank of England (BoE) should ring alarm bells for anyone expecting further increases in Chinese demand and consumption in the near future. China is reportedly transitioning from an export-driven to a consumption-driven economy. This economic adjustment is supposed to lead to more sustainable and stable economic growth. Yet, debt levels are exceptionally high in China and still rising. Unless the Chinese government has figured out how to create a perpetual motion machine of debt and consumption, China’s transition to a consumption-driven economy should soon hit a significant roadblock.

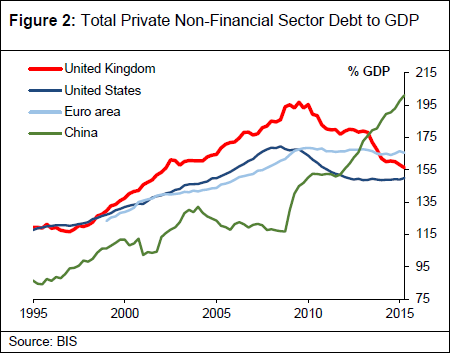

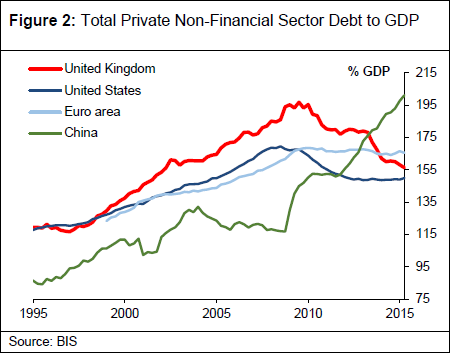

The chart below puts China’s debt run-up in global context. Total private non-financial sector debt has increased rapidly since the financial crisis. As a percentage of GDP, China has surpassed even the pre-crisis peak seen in the United Kingdom.

Total private non-financial sector debt has soared in China relative GDP in the past several years. It has now surpassed the pre-recession peak even in the United Kingdom.

Source: “Debt, Demographics and the Distribution of Income: New challenges for monetary policy” – Gertjan Vlieghe, Member of Monetary Policy Committee, Bank of England, January 18, 2016.

This high-level of debt help explains why the Chinese government has struggled to get much response out of a long series of stimulus measures over the past year or so. The capacity for piling up yet more debt must be reaching some kind of limit. While that specific limit cannot be known in advance, especially since China’s economy is in a much higher growth mode than its Western competitors, I strongly suspect the limit is near. Companies that are continuing to rely upon the China growth story to support their own growth story over the next few years will (continue to) stumble as China approaches and then breaks down from this debt limit.

Related Posts

Omnicom (OMC) Beats On Q3 Earnings Despite Lower Revenues

Omnicom (OMC) Beats On Q3 Earnings Despite Lower Revenues The Agenda podcast chats crypto and sex work with WetSpace CEO Allie Rae

The Agenda podcast chats crypto and sex work with WetSpace CEO Allie Rae Ebay Inc. Shares Dive After Earnings, Paypal Holdings Inc. Stock Rises

Ebay Inc. Shares Dive After Earnings, Paypal Holdings Inc. Stock Rises Is Nikkei Preparing For Huge Breakout?

Is Nikkei Preparing For Huge Breakout? EU Session Bullet Report – USD Trades Steady Ahead Of NFP

EU Session Bullet Report – USD Trades Steady Ahead Of NFP EUR/USD And GBP/USD Forecast – February 29, 2016

EUR/USD And GBP/USD Forecast – February 29, 2016

Leave A Comment