Three years after quitting his job at Jeffrey Tannenbaum’s Fir Tree Partners and starting his own hedge fund, 39-year-old Adam Schwartz believes he has found the next big short.

Picking up on a theme that has been thrown around frequently on Wall Street, ever Since Howard Marks asked in March 2015“what would happen if credit ETF holders sold all at once”, and prompting many other Wall Street icons to warn about the dangers of debt ETFs, Schwartz is so convinced that a blow up in fixed income is coming and will hit credit ETFs the hardest, that he has been not only shorting these passive vehicles but layering puts on top.

To Schwartz, it’s only a matter of time before rising rates kill the easy financing for highly leveraged companies, spurring a wave of bond defaults. Furthermore, as Bloomberg notes, running a hedge fund with mostly his own cash has allowed Schwartz the freedom to bet on more extreme scenarios, like betting on the very extinction of the product with credit ETFs “perishing in the bloodbath.”

Why? Because as he told Bloomberg, “the ETF structure isn’t really designed for a large market sell-off. They will break if people don’t trust that they have the liquidity that they think they do today.”

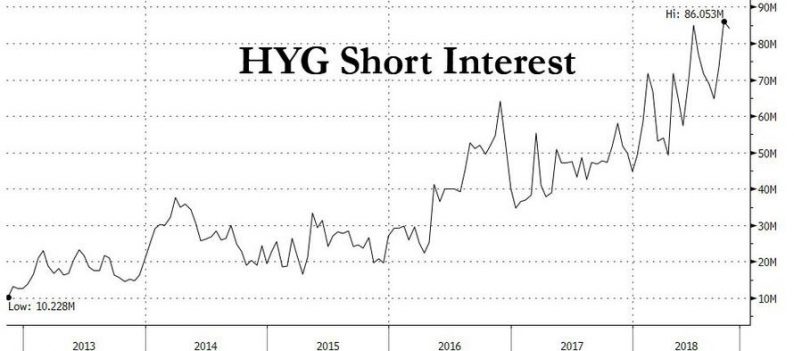

As noted above, Schwartz’ thesis is hardly new, and while ETF providers such as BlackRock – naturally – argue their funds provide a positive force by “adding liquidity” and price transparency in times of stress, others such as Marks say they create a false sense of stability. Meanwhile, other shorts have been piling on and as the chart below shows, the amount of short interest in the HYG junk bond ETF is now the highest on record as many other investors are also convinced the credit ETF day of reckoning is coming.

Yet few investors have backed their conviction in the inevitable extinction of credit ETFs to the same extent as Schwartz: while his Black Bear Value Partners is tiny compared with the $600 billion bond ETF market, his shorts make up about 25% of exposures in the hedge fund Schwartz set up and manages, even though so far these are wagers that have yet to deliver much of a profit.

Leave A Comment